This post is adapted from ARtillery Intelligence’s report, XR 2018 Lessons, 2019 Outlook. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

2018 was a reflective year for XR. After an exuberant 2016, followed by a corrective 2017, XR industries settled into a moderate pace. This includes reset expectations on the size and timing of AR & VR markets, as well as acceptance that aspirations will take longer to materialize.

But we saw deep-pocketed tech giants charge ahead with XR. With strong contention that XR represents the next computing shift, they’re investing in the future of their platforms by gaining early market share and technological edge. And they’re each attacking XR from different angles.

Despite XR market softness, it was these moves from tech giants that provided confidence in 2018 for the eventual market arrival. Indeed, there’s no bigger vote of confidence in a technology and a market than billions of dollars in long-term bets. We believe this will continue into 2019.

#4. Enterprise AR is a Sleeping Giant

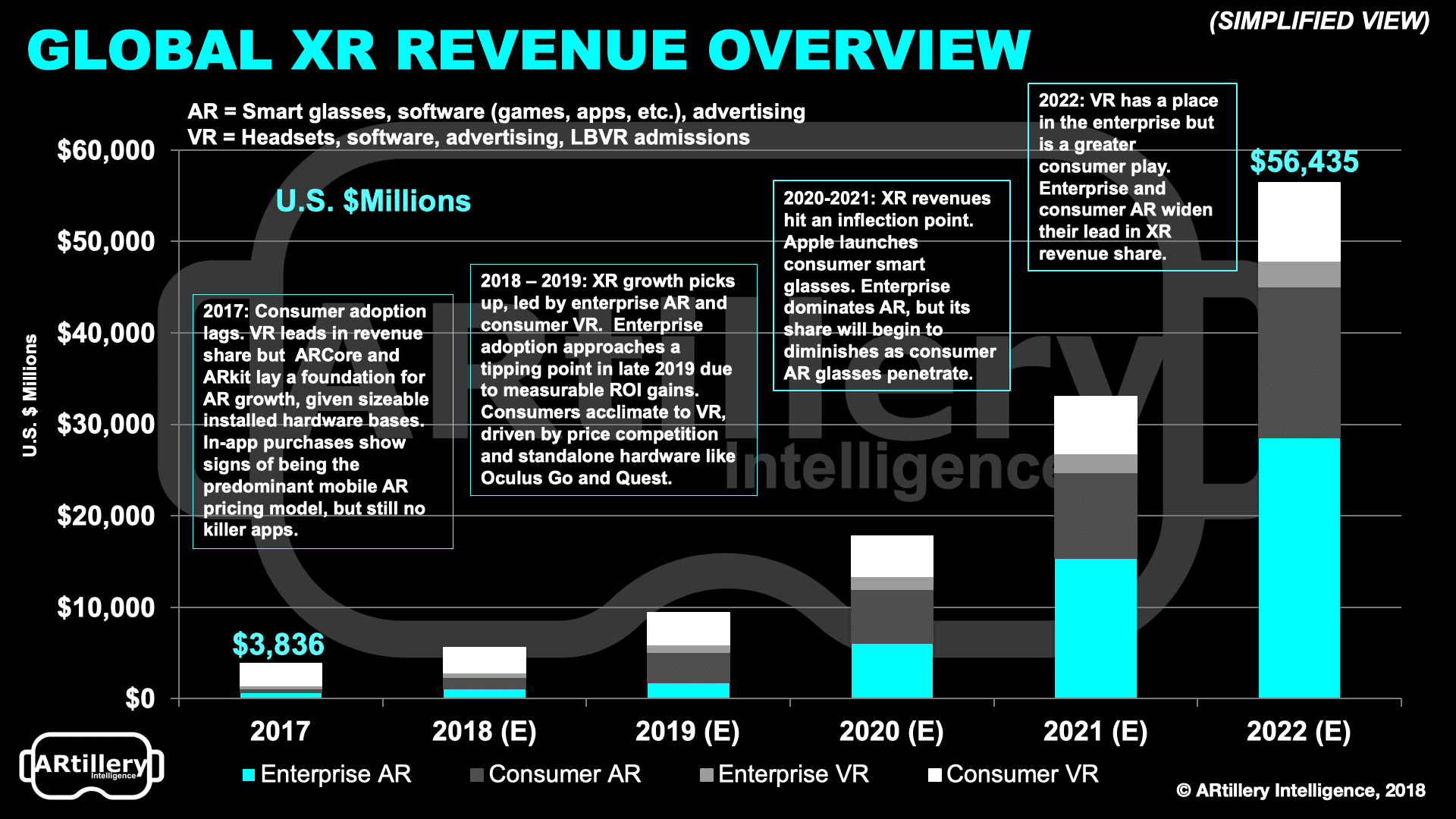

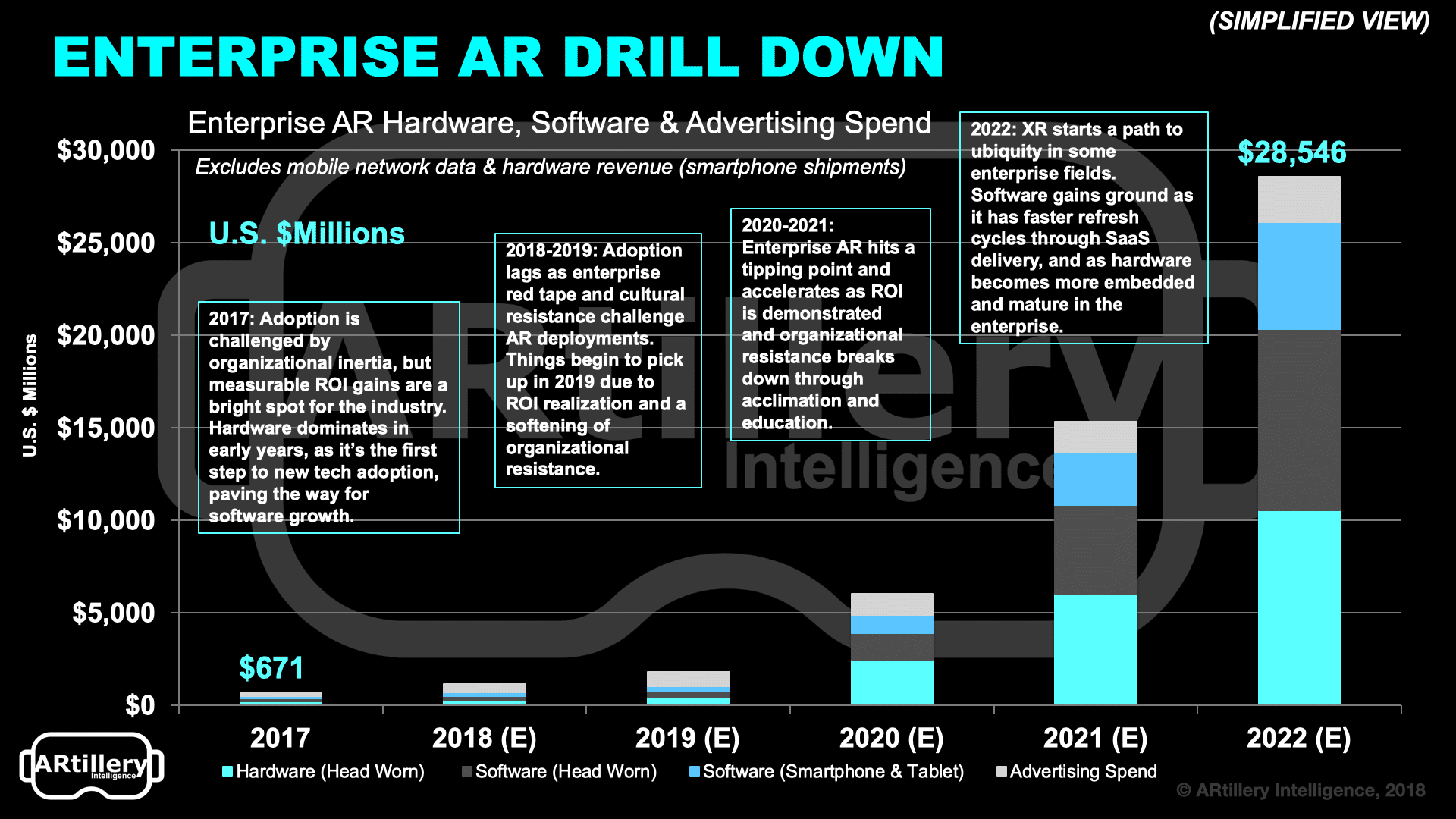

Picking up where we left off last week in drilling down on our specific 2018 lessons and 2019 predictions, Enterprise AR will continue to hold lots of promise, based on the continually-validated ROI for AR-assisted productivity. We project revenues to grow to $28.5 billion in 2022.

But that will start slow ($1.8B in 2019) due to the inertia and risk aversion that faces enterprise AR deployments. Though there’s often adoption among business leaders and innovation centers in a given organization, AR often fails to convert other stakeholders, resulting in “pilot purgatory.”

Points of resistance include mandated risk-aversion in IT departments, given headset cameras and proprietary data exchange (e.g. CAD files). It also notably includes end-user employees who have natural fears of new technology, and how it could impact their job security.

“We’re talking about some pretty impressive ROI numbers,” Scope AR CEO Scott Montgomerie said at AWE Europe. “If I’m a worker, I’m thinking the company can do the same bottom line with 50 percent of the workforce… does that mean I have a 1 in 2 chance of keeping my job?’”

These factors will continue to stunt enterprise AR growth, but will be counteracted eventually by momentum, support and ROI realizations that are currently building. A tipping point will come, after which adoption accelerates in a sort of enterprise herd mentality. But that won’t be in 2019.

We believe the tipping point will be in 2020, followed by ramping adoption across industrial sectors. This will follow a similar pattern, though on a smaller scale, as enterprise smartphone adoption over the past decade. Like we saw then, it will build slow then happen fast.

As for the adoption dynamics, near-term Enterprise AR revenues will be hardware-dominant as it’s usually the first step in enterprise tech adoption. That hardware growth then creates a cumulative installed base for software, which will increasingly dominate enterprise AR in outer years.

AR hardware will also mature as it’s established in the enterprise, with replacement cycles outpaced by software refresh rates. As it played out in the broader enterprise software world, the prevailing AR software model will be SaaS, in terms of how it’s packaged, priced and delivered.

For a deeper dive on 2108 lessons and 2019 predictions, see the full report.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.

Header image credit: Clayco