This post is adapted from ARtillery Intelligence’s report, Spatial Computing: 2019 Lessons, 2020 Outlook. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

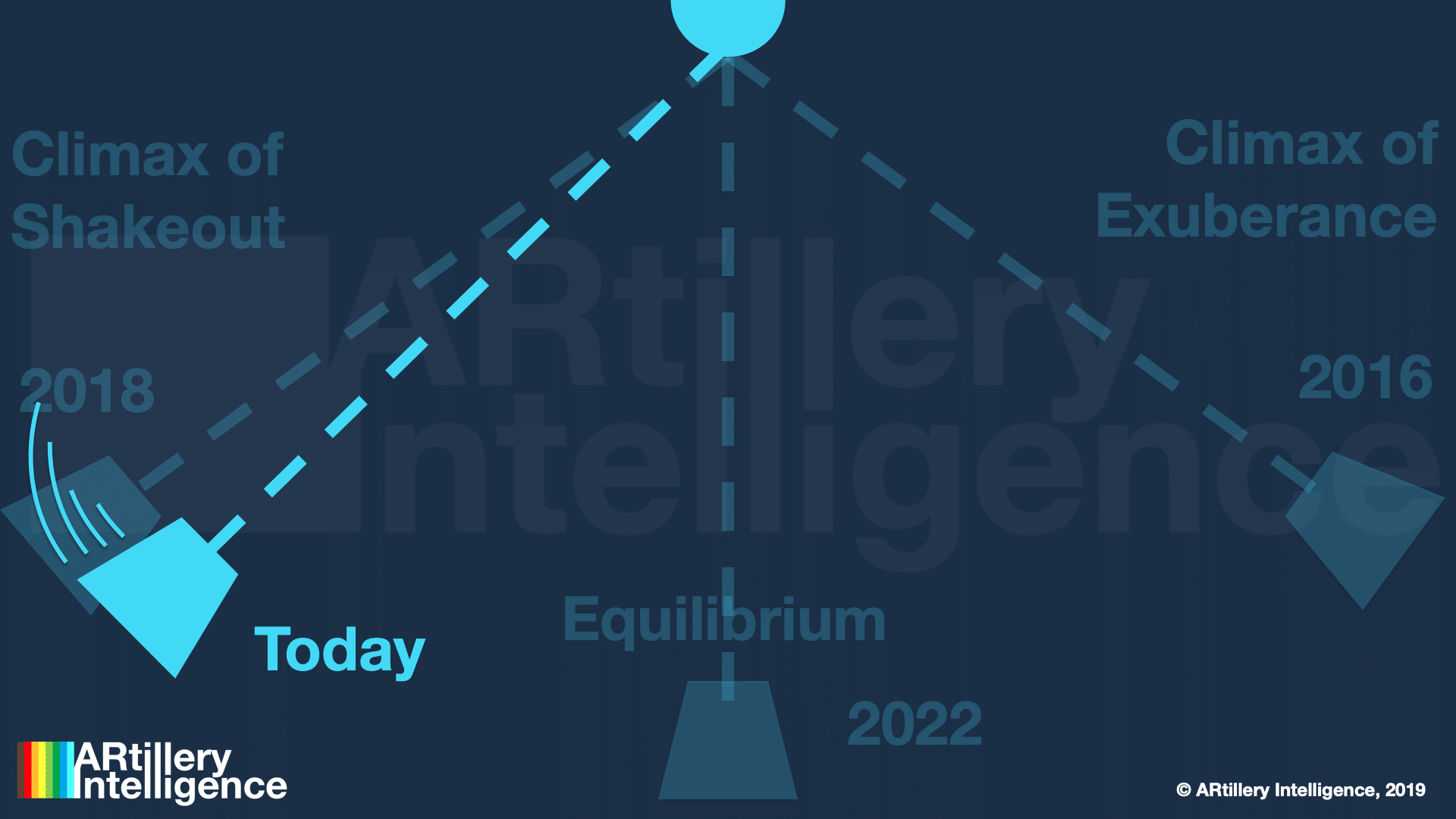

They say that patience is a virtue. This applies to the current state of the spatial computing industry. After passing through the boom and bust cycle of 2016 and 2017, the last two years were more about measured optimism in the face of industry shakeout and retraction.

At the precipice of 2020, that leaves the question of where we are now? Optimism is still present but AR and VR players continue to be tested as high-flying prospects like ODG, Meta and Daqri dissolve. These events are resetting expectations on the timing and scale of revenue outcomes.

But there are also confidence signals. 2019 was more of a “table-setting” year for our spatial future and there’s momentum building. Brand spending on sponsored mobile AR lenses is a bright spot, as is Apple AR glasses rumors. And Oculus Quest is a beacon of hope on the VR side.

To synthesize where we are and where we’re going, our research arm ARtillery Intelligence has published its annual year-end recap and year-forward outlook. This includes five predictions, listed below. Following last week’s look at the first prediction, today we’ll drill down on #2.

1. Apple Glasses Don’t Arrive in 2020

2. AR Wins With “Training Wheels”

3. Advertising Keeps the AR Revenue Crown

4. Industrial AR’s Inflection is Still One Year Away

5. VR Has an Evolutionary (not revolutionary) 2020

Prediction 2. AR Wins With ‘Training Wheels’

The spatial computing industry is learning that its circa-2016 ambitions aren’t translating to mainstream adoption. This is causing a sobering realization throughout the sector that mainstream consumers aren’t as excited about AR (or don’t understand it) as its proponents are.

This is mostly due to confusion over the technology, or the fact that its proposed use cases are a mismatch with mainstream interest. Therefore, any potential killer apps will have to meet users halfway in terms of their existing interests and cognition. This strategy will be critical in 2020.

This means a few things: AR providers that can acclimate consumers to AR by tapping into existing behavior will succeed in boosting adoption. One example is Ubiquity6’s strategy to condition users to scanning spaces by giving them a free tool to capture and share 3D models.

This taps into an existing area of interest (social sharing), and represents the types of training wheels that AR needs. Support can also be seen in the most popular form of AR – selfie lenses. They’re shared with friends in the same channels as photo sharing, and build on existing behavior.

Another example is Houzz. As we recently examined, it holds a central design principle to put AR in users’ direct path. Though easier said than done, this eliminates friction or possible breakpoints for users to drop off. AR is too early and unproven to get users to go out of their way.

Sleeping Giants

Instagram is another example and is AR’s biggest sleeping giant. It has already conditioned a shopping and transactional use case, which is now enhanced by AR. It will succeed in driving AR ad revenue by adding the technology to existing product and fashion discovery behavior.

Another example of the “training-wheels” principle is the broader product category of wearables. The sector’s existing growth will feed into AR by acclimating users to wearing sensors on their bodies. Apple is already conditioning this use case (AirPods & Watch), as is Snap (Spectacles).

Speaking of Apple, it will further exercise this training-wheels approach in the ways described in prediction #1. To get users acclimated to AR glasses, it will start with a use case that they’re already comfortable with: watching TV and movies. It will then ease them in to “true AR.”

Another way that AR will get over the adoption hump is with utilities that provide tangible value to consumers – in addition to the social and entertainment use cases that have erstwhile ruled AR. This includes most notably visual search (Google Lens) and navigation (Google Live View).

Meanwhile, we see compelling wild cards like Tilt Five. With the enormous perspective and technical chops of CEO Jerri Elsworth, it plays on the concept of “AR somewhere” as a stepping stone to “AR everywhere.” This embodies training wheels perhaps more than anything above.

Boiling it Down

Boiling down all of the above into a concrete prediction, all of these players will invest heavily in these precursors to AR, pursuant to longer-term strategies to future proof their businesses. Apple will invest in wearables to offset iPhone sales declines, and condition the world for AR glasses.

Snap will do the same with Spectacles by feeling out user demand and acclimating consumers for future AR glasses. Google will accelerate the adoption of visual search and navigation by incubating them in search, including lots of calls to action in that well-traveled venue.

Of course all of the above is speculative and based on market signals we’re tracking closely. It will be a moving target, and we’ll course correct as market factors unfold. We’ll also hold ourselves to task in 2020 for all predictions. Stay tuned for more and see the full report here.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.