This post is adapted from ARtillery Intelligence’s report, Mobile AR Strategies & Business Models. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

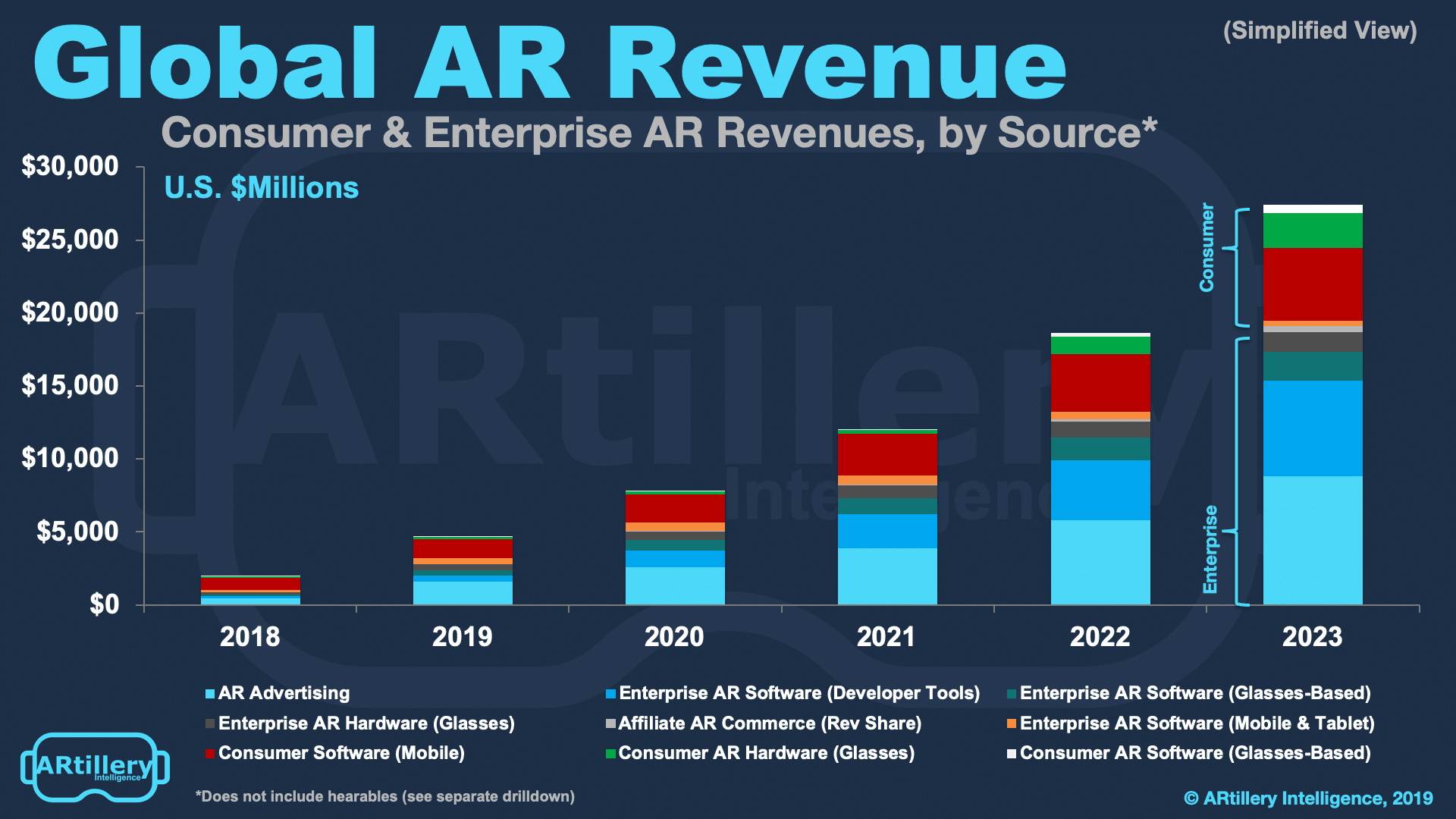

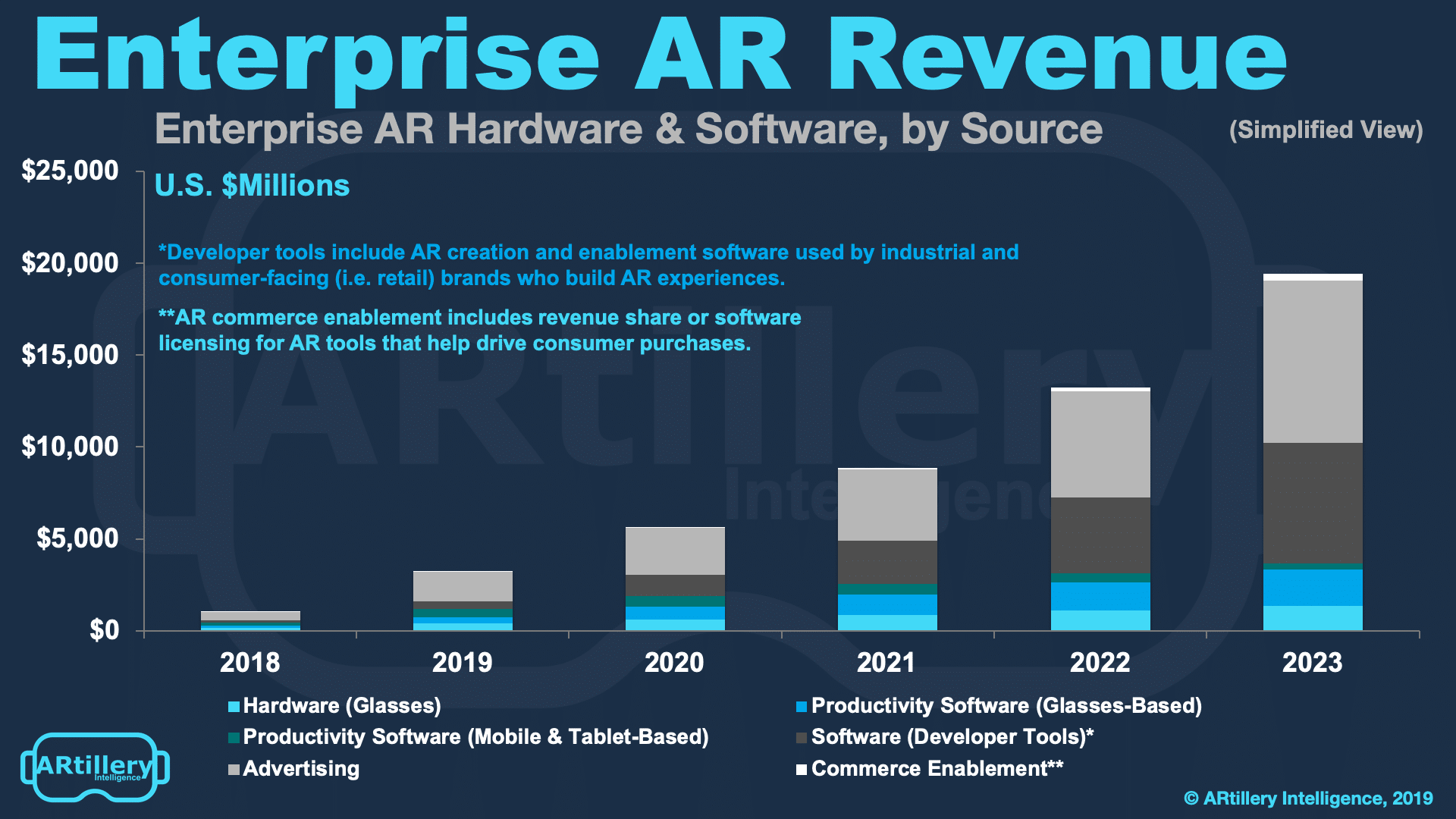

In AR’s early stages, a common question continues to be asked: where’s the money? There have been oscillations in excitement and doubt over AR, but the ultimate proof point will be revenue. Though aggregate revenues have disappointed, there are segments that are bearing fruit.

So we’ve determined the three biggest revenue categories for consumer-based mobile AR. We’ve examined them on qualitative and quantitative levels. The former entails product models, leading companies and best practices. The latter entails market sizing and revenue projections.

But before we dive into these models, continuing today with AR-as-a-Service, what are they at a high level? We categorize them as follows:

1. Advertising (brands pay)

2. In-app purchases (consumers pay)

3. AR-as-a-service (enterprises pay)

Drilling Down on ARaaS

We left off last week talking about AR-as-a-Service (ARaas) with some introductions and high-level examples. Going one level deeper, what forms will it take and where will the greatest value be realized. The short answer is wherever AR can be democratized and scale to new personas.

For example, one area builds on the AR commerce use case of product visualization. This involves “try-before-you-buy” experiences for everything from cosmetics to couches. It’s been very popular with users and effective for consumer brands, but there are also challenges.

For example, product visualization requires digitizing a given brand’s products. This is relatively easy if there’s a limited range of products, such as with BMW’s iVisualizer app. But it gets more complicated with product catalogs with thousands or millions of models or color/size variants.

“Whenever anyone asks what they need to do to get ready for the future, I say make digital twins of everything in your inventory,” Unity’s Timoni West told us. “A lot of companies don’t have that right now or they have CAD files for 3D printing that are way too big and won’t work for mobile.”

In the near term, IKEA, Wayfair and others offering AR visualization rely on individual solutions to scan products. But the real opportunity is for specialized and standardized methods that can help them scale up 3D image libraries; and bring the opportunity within reach of down-market players.

E-commerce platform Shopify has done this by bringing AR product visualization to 600,000 businesses. Using the USDZ file format, Shopify merchants can create 3D graphics that are immediately usable in Apple’s Quick Look AR feature. This is where ARaaS will shine.

“Wayfair and IKEA have their own means and methods they’ve created in-house, because there’s nothing out there that’s scalable, affordable and easy,” said 8th Wall VP of Product Tom Emrich at a Cambridge House event. “These are startup opportunities that, as an investor, I’m looking at.”

AR Cloud Startups

As we’ve explored for the past few years, advanced consumer AR experiences will require a pervasive and spatially-anchored data layer that devices can dynamically tap into. Companies building different components of the AR cloud will be an important part of the spatial ecosystem.

They qualify as ARaaS because they’re providing software to AR app and experience developers to tap into the AR cloud. That includes companies like 6D.ai, which provides an API for apps to access AR cloud data. In return, they contribute spatial maps collected through the app use.

Others include Ubiquity 6. Its Reality Editor is a low-friction tool to build web AR experiences that can be viewed through its spatial browser. It eventually wants to be at the center of a marketplace of AR digital goods creation, and is starting with its low-friction display.land spatial mapping tool.

These are a few examples and other AR cloud startups include Scape and YouAR. Business models are developing and will be packaged in various ways (not necessarily SaaS pricing), such as Ubiquity 6’s potential affiliate marketplace revenues and 6d.ai’s variable-use pricing.

We’ll be circle back next week to continue this discussion around AR-as-a-service and other forms its taking, such as gaming and Niantic’s Real World platform Meanwhile, see more about this report here. Revenue models will be a quickly moving target as AR finds its footing.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.