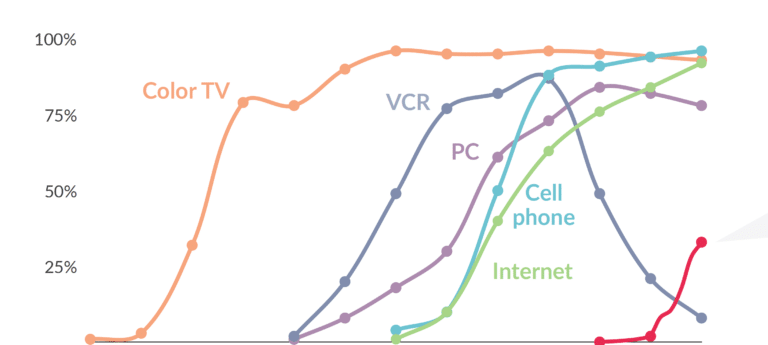

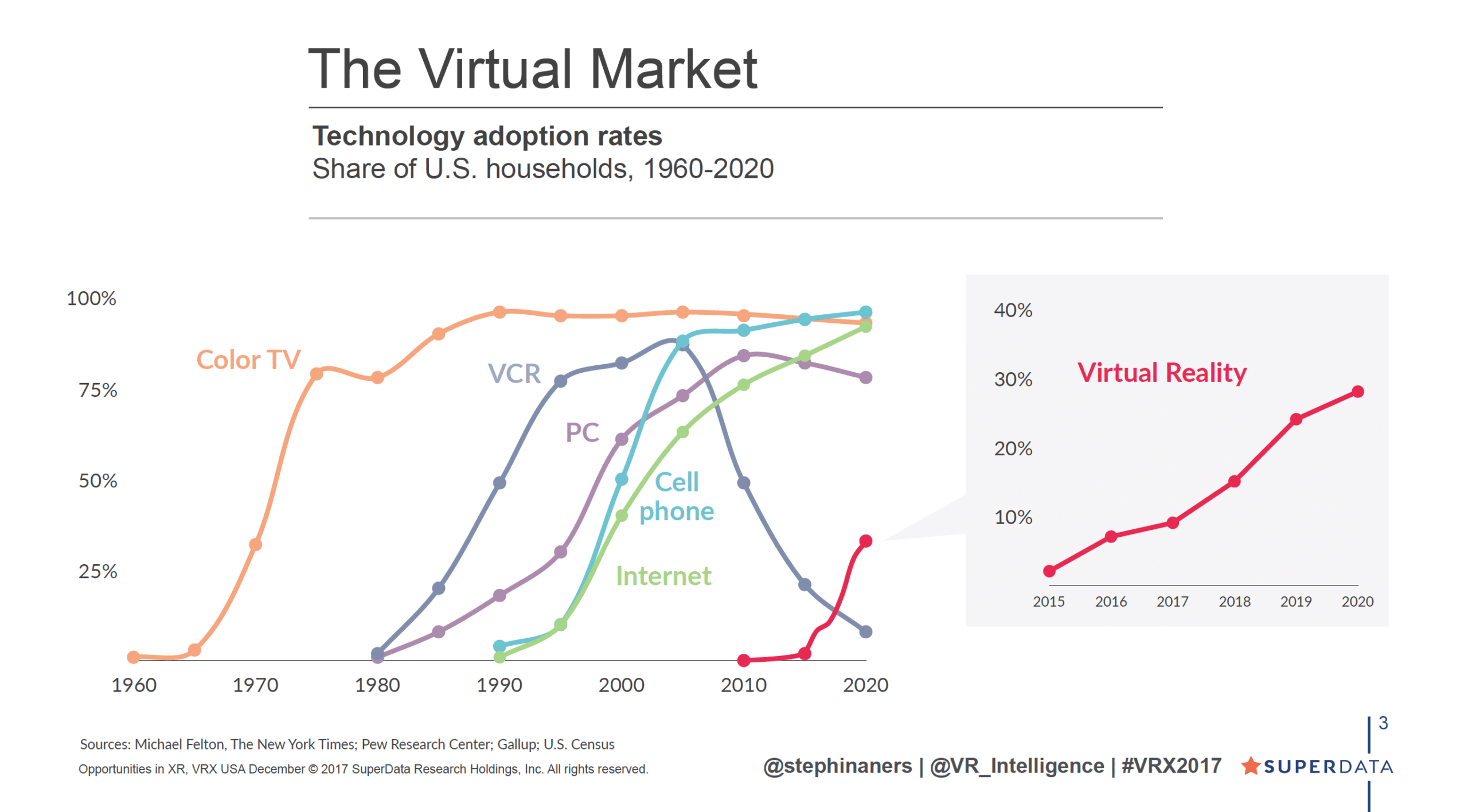

Consumer VR isn’t growing as fast as many expected, or as the hype cycle of the past two years may have indicated. But how big is it and where is it trending? We’ve indicated in the past that total headset penetration is about 17 million units, or about 13 percent of U.S. households.

Superdata presented new projections at the recent VRX show that indicate that VR headset penetration is currently aligned with that figure, at about 11 percent of U.S. households. But more interestingly, the firm projects adoption to grow to about 30 percent of households by 2020.

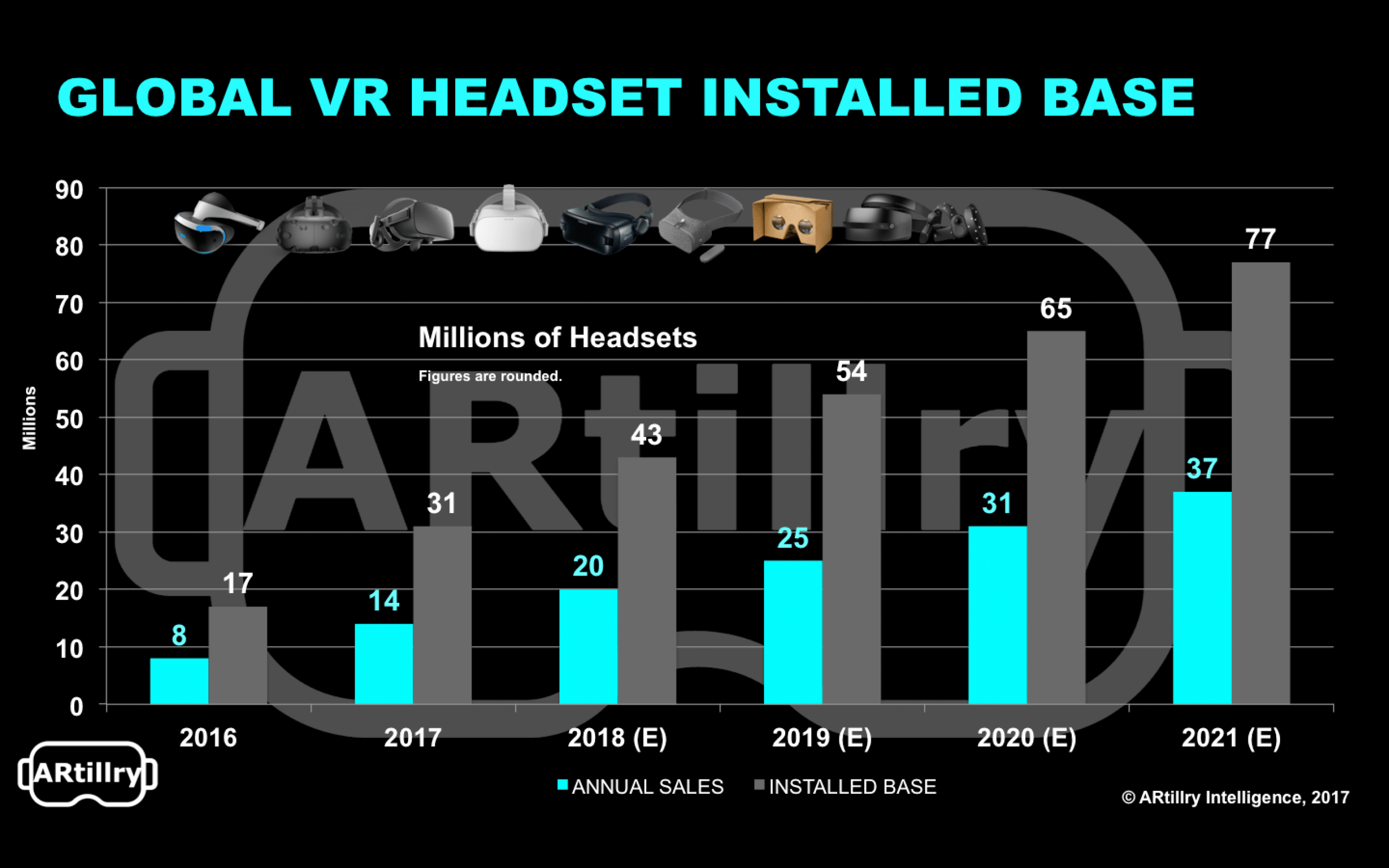

That would be about 38 million headsets, given 125 million U.S. households. Presumably this is an installed base figure (cumulative active headsets), as opposed to annual sales (a different metric). ARtillry Intelligence recently projected a 2020 global installed base of 65 million headsets.

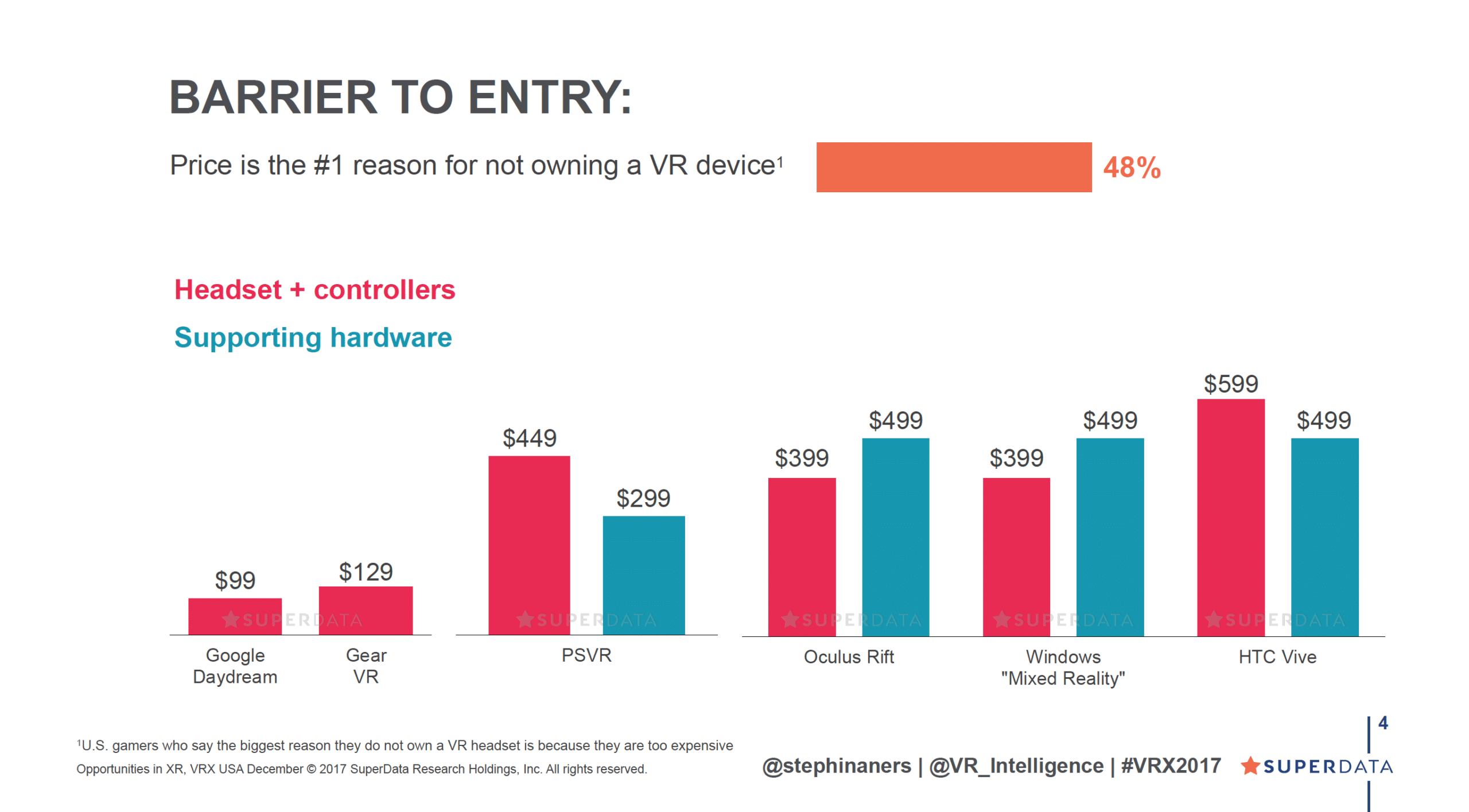

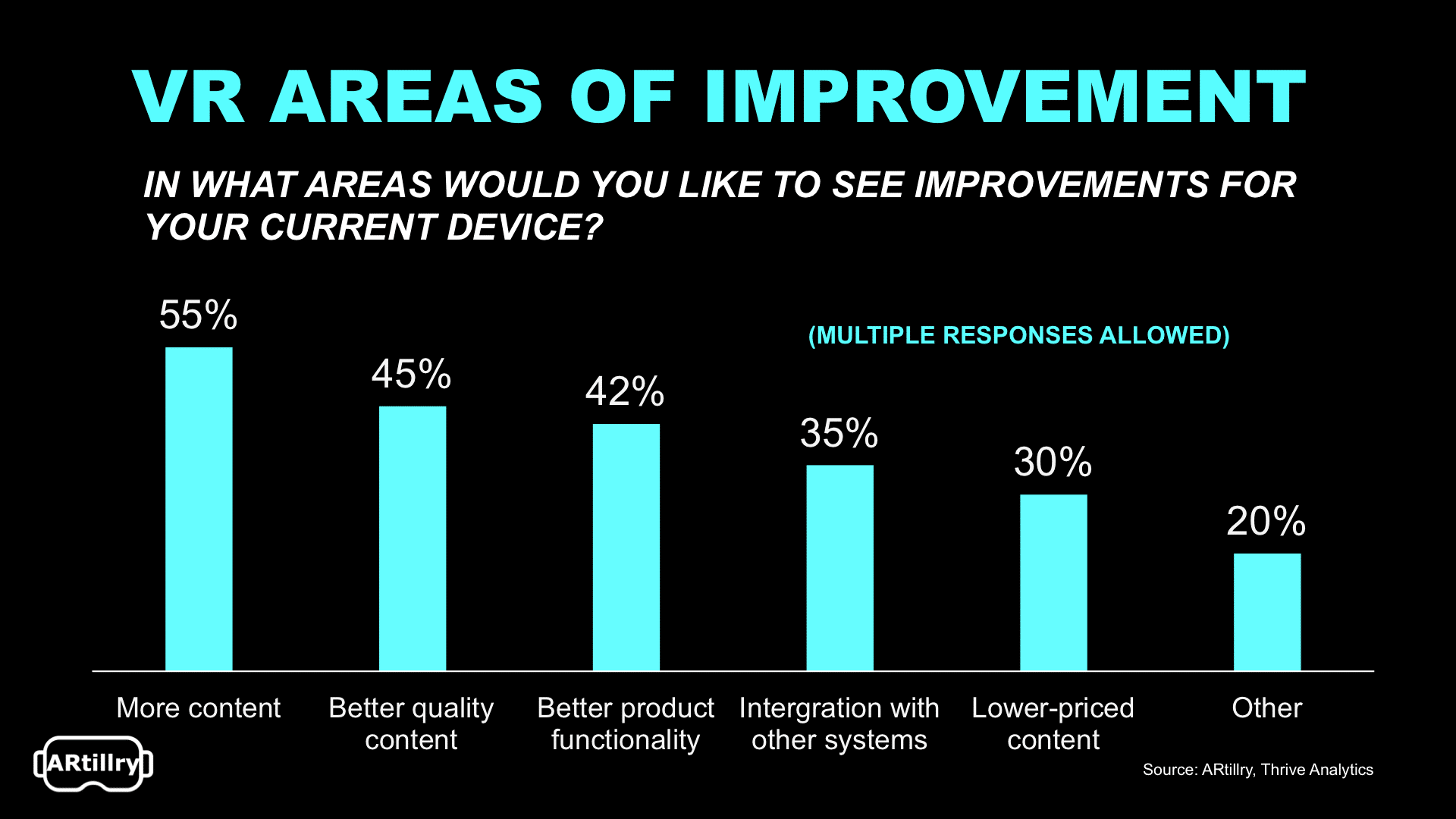

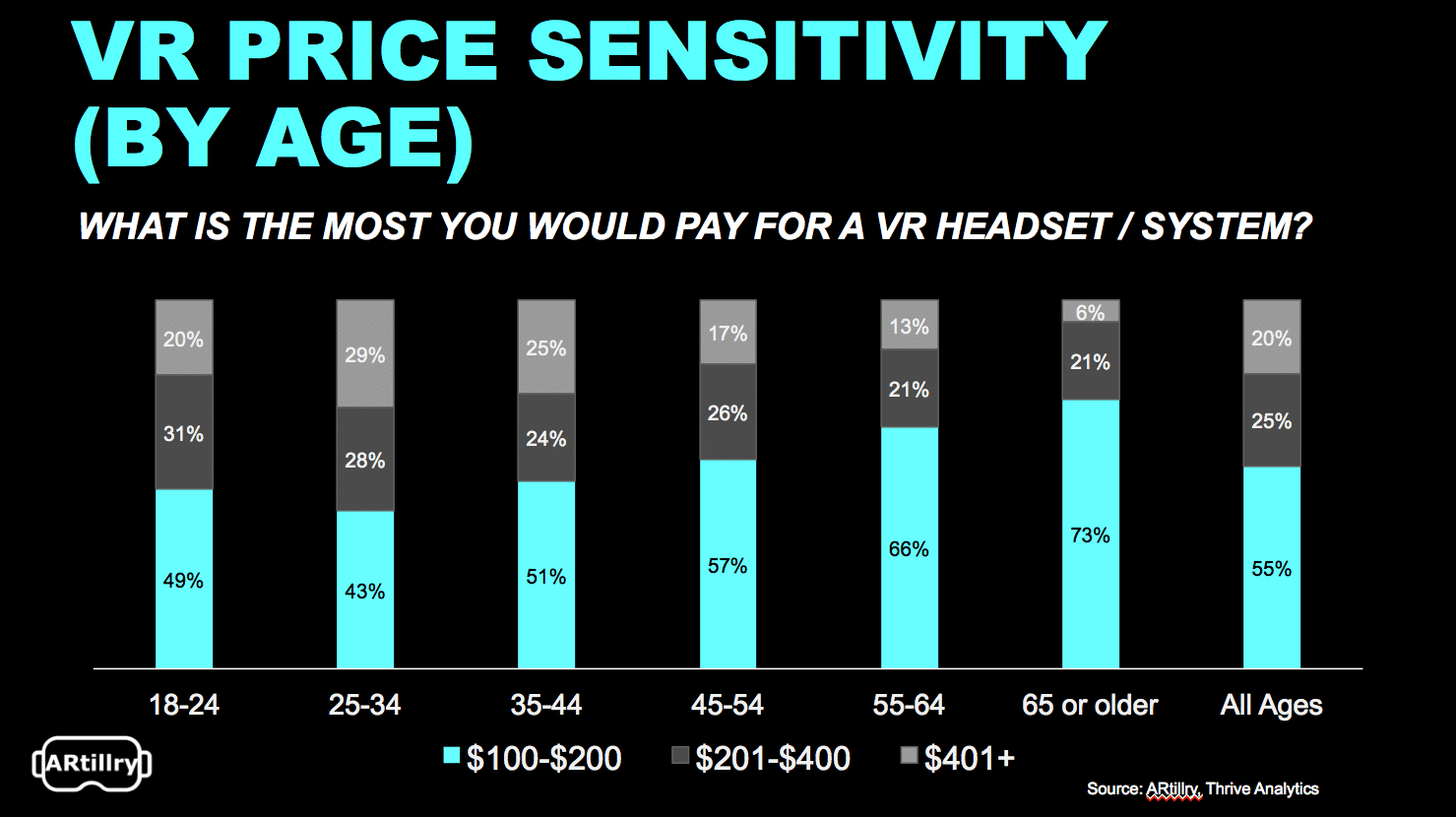

As for adoption drivers, it will be all about price. Superdata pegs price as the biggest adoption driver (and inhibitor). This once again aligns with ARtillry Intelligence data (below) that indicates price as one of VR’s greatest adoption factors, although we found content to be a greater factor.

Either way, price will be impactful and we’re seeing lots of price competition. Perhaps most impactful will be Oculus Go’s $199 price tag, which is right in the sweet spot for VR adoption. And its standalone format means no addiitonal costly hardware purchases (such as a PC) required.

More data points are included below and more of our pricing analysis can be seen here. Subscribe to ARtillry Insights for lots more data and analysis.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.