This post is adapted from ARtillry’s latest Intelligence briefing, XR: 2017 Lessons, 2018 Predictions, and specifically zeroes in on 2017 lessons. You can preview more of the report here, or subscribe to access it in full.

Weaker than expected AR & VR (XR) hardware sales defined 2017. As is often the case with emerging tech, hardware is a key leading indicator because it comes first and creates an installed base for software and overall market growth.

VR hardware’s softness in 2017 led to restrained excitement levels and readjusted market sizing. Attention shifted to mobile AR, given a greater installed hardware base, but even that has receded to some degree, given weak content thus far.

This all amounts to a bit of a shakeout, and a market correction from the XR exuberance that defined 2015 and 2016. The question is if it will continue into 2018.

Silver Lining

It’s not all bad news for XR. The sector’s early exuberance wasn’t misplaced but was mistimed. Like e-commerce in the early 2000’s, its eventual market size exceeded expectations… but not until 3-5 years later. And that’s where we now sit with XR.

It’s therefore better to view XR today as a period of early-stage R&D than one that’s ready for prime time (especially consumer VR). On that measure, there are positive signs for XR’s long-term health including investment levels in “building block” technologies.

Meanwhile other signals provide confidence: $2.1 billion in 2017 XR funding (equivalent to 2016) and strong early sales for VR hardware such as PSVR’s cumulative two-million unit sales. Standalone VR will also boost overall demand levels (more on that in a bit).

There’s also strength in location based VR, especially in China where cultural affinities for out of home gaming are an important revenue opportunity to cover the gap before VR home ownership scales. We saw the same trend with video games in the 70’s and 80’s.

TAM Right

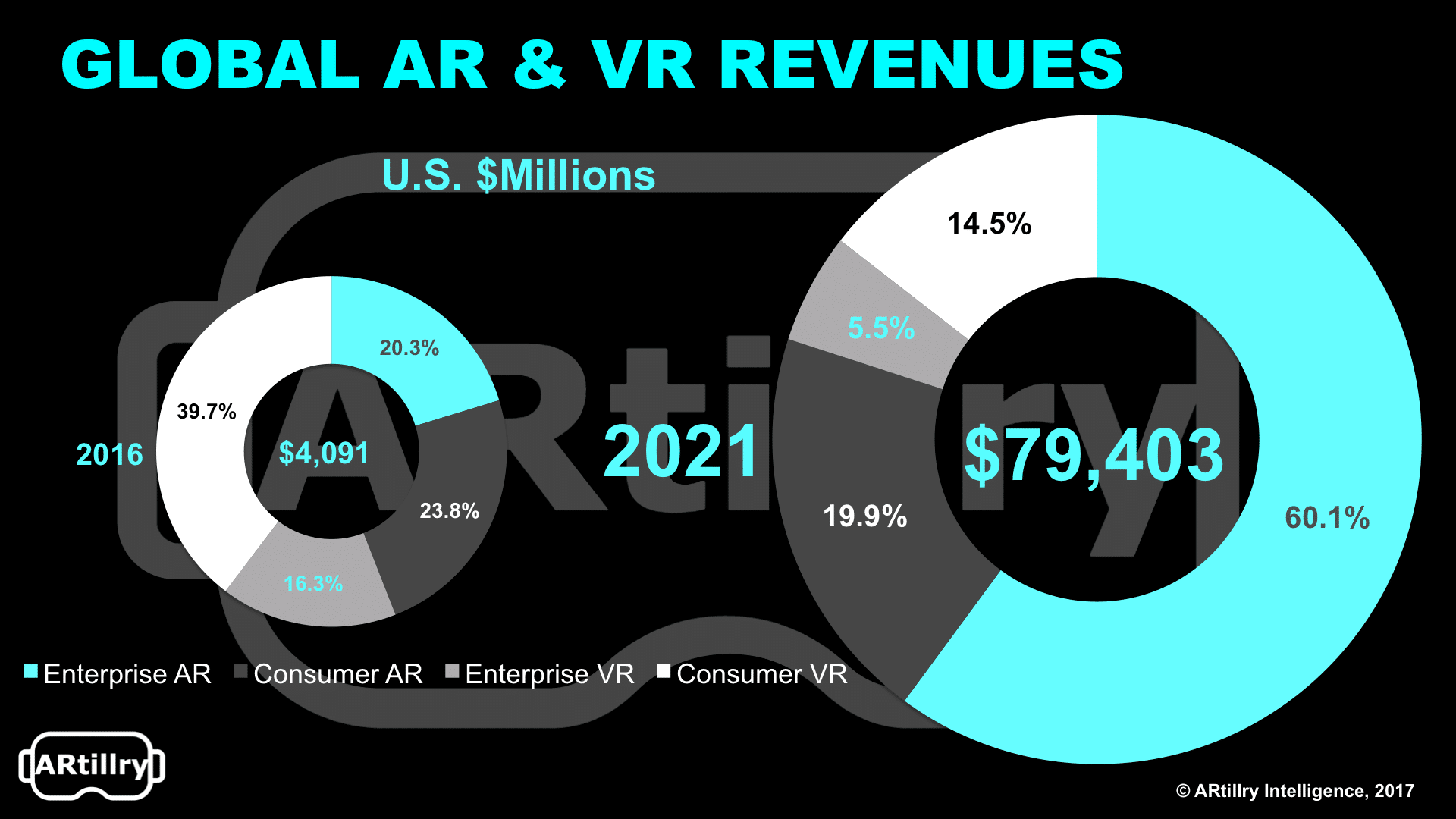

Weak VR hardware adoption caused the market to shift focus towards mobile AR’s larger installed base and total addressable market (TAM). There are 3.2 billion global smartphones, 500 million of which are AR compatible given the “democratization” of AR brought by ARkit and ARCore.

ARkit received a slow start for consumer demand and compelling content, indicating that it will take more time for mobile AR’s promise to be realized. Like VR’s “chicken and egg” dilemma, it will take time before mobile AR apps compel larger audiences and vice versa.

Meanwhile, mobile AR usage levels were weak in 2017 and will need more time to develop, along with mobile AR business models. Mobile AR revenue in 2017 was roughly $500 million, mostly from Pokemon Go, which stands as a model for mobile AR business models (in-app purchases).

Best practices for AR app design are starting to emerge, including “native thinking” “AR-first” design, and achieving stickiness for recurring usage. Meanwhile, we’ve seen mostly misfires and no “killer app” that defines the category yet. This could change in 2018.

Augmenting Jobs

Unlike slow adoption for consumer VR, enterprise AR and VR have a clearer ROI story and receptive buyer. This includes measurable bottom line impact from operational efficiencies through AR-guided manufacturing and assembly (speed, error reduction, etc.).

In 2017, we began to see ROI proof points through pilots and case studies. Best practices have also begun to develop with respect to selling XR integrations into enterprises and navigating famously-cumbersome sales cycles for large organizations.

These best practices include “speaking the language” of enterprise software sales. They also include building teams that have strong cross-disciplinary orientation such as technical chops, business development and vertical domain expertise for target markets.

Optimizing VR

Weak consumer VR adoption has created a greater impetus to define user demand and preferences. ARtillry Intelligence consumer data in 2017 revealed that the top adoption factor for consumers is content, followed by price (reason could dictate the opposite).

However, content is held back by a classic chicken and egg dilemma where a low installed base dampens content creation and vice versa. This will change over time as falling hardware prices boost adoption. Again, price is the second biggest adoption factor.

According to ARtillry Intelligence, the price target where consumer interest in VR spikes the most is $200. This brings VR to a giftable range and one that can appeal to a much greater swath of the consumer public. And that’s what we’ll begin to see in 2018.

This is where the newest batch of standalone VR headsets could have real impact, including the $199 oculus Go announced in 2017 for mid-2018 launch. More on ARtillry’s 2018 predictions — building from all of the above 2017 lessons — can be seen here.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.

Header image credit: Oculus