AR Briefs is a video series that outlines the top trends we’re tracking, including takeaways from recent reports and market forecasts. See the most recent episode below, and past installments are here.

XR has seen volatile levels of interest and investment over the past 24 months. Like past technological waves, the excitement isn’t necessarily wrong… but it is early. So we’ve ventured to quantify XR revenues in our latest bi-annual forecast, and episode of AR Briefs (below).

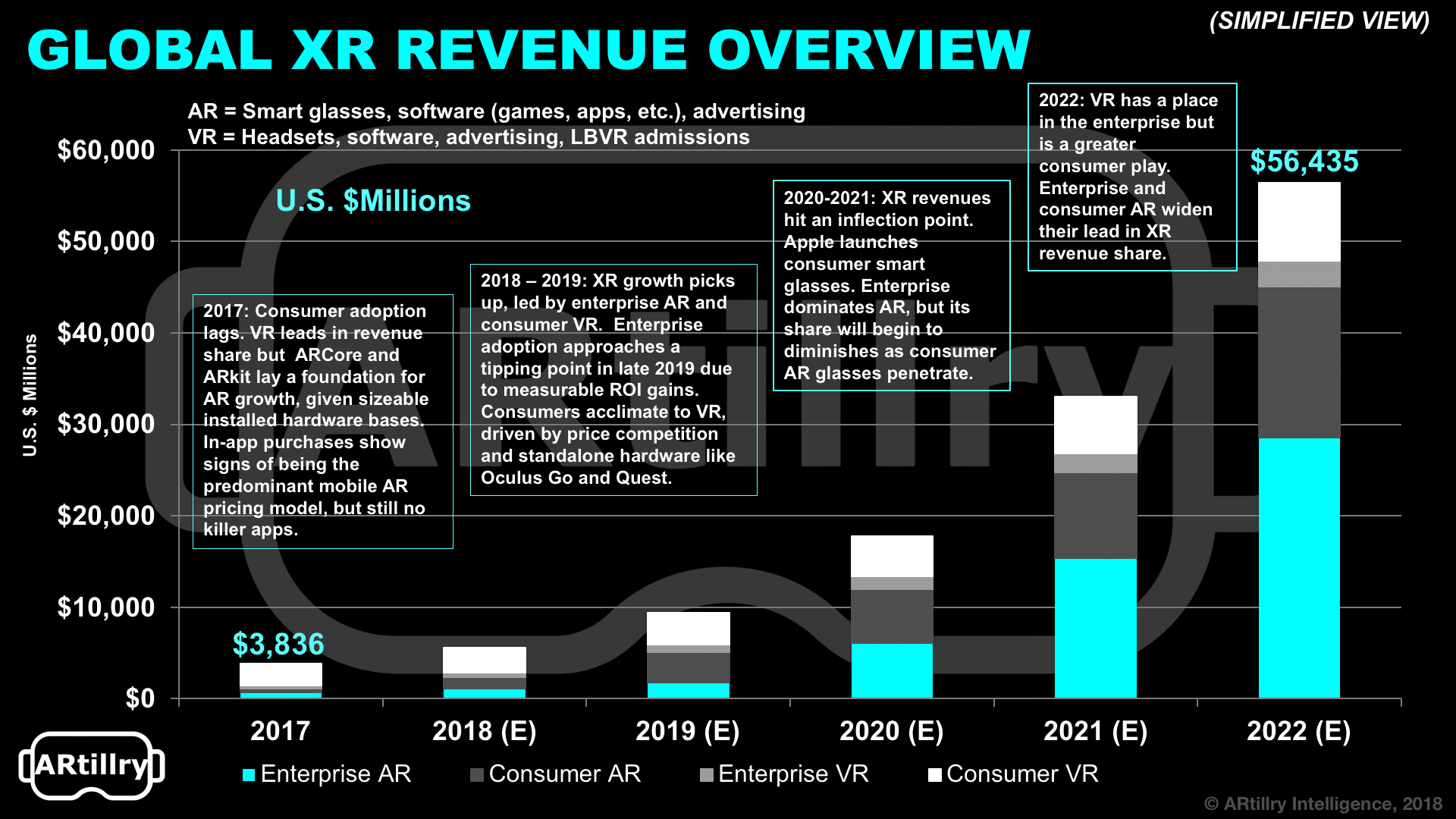

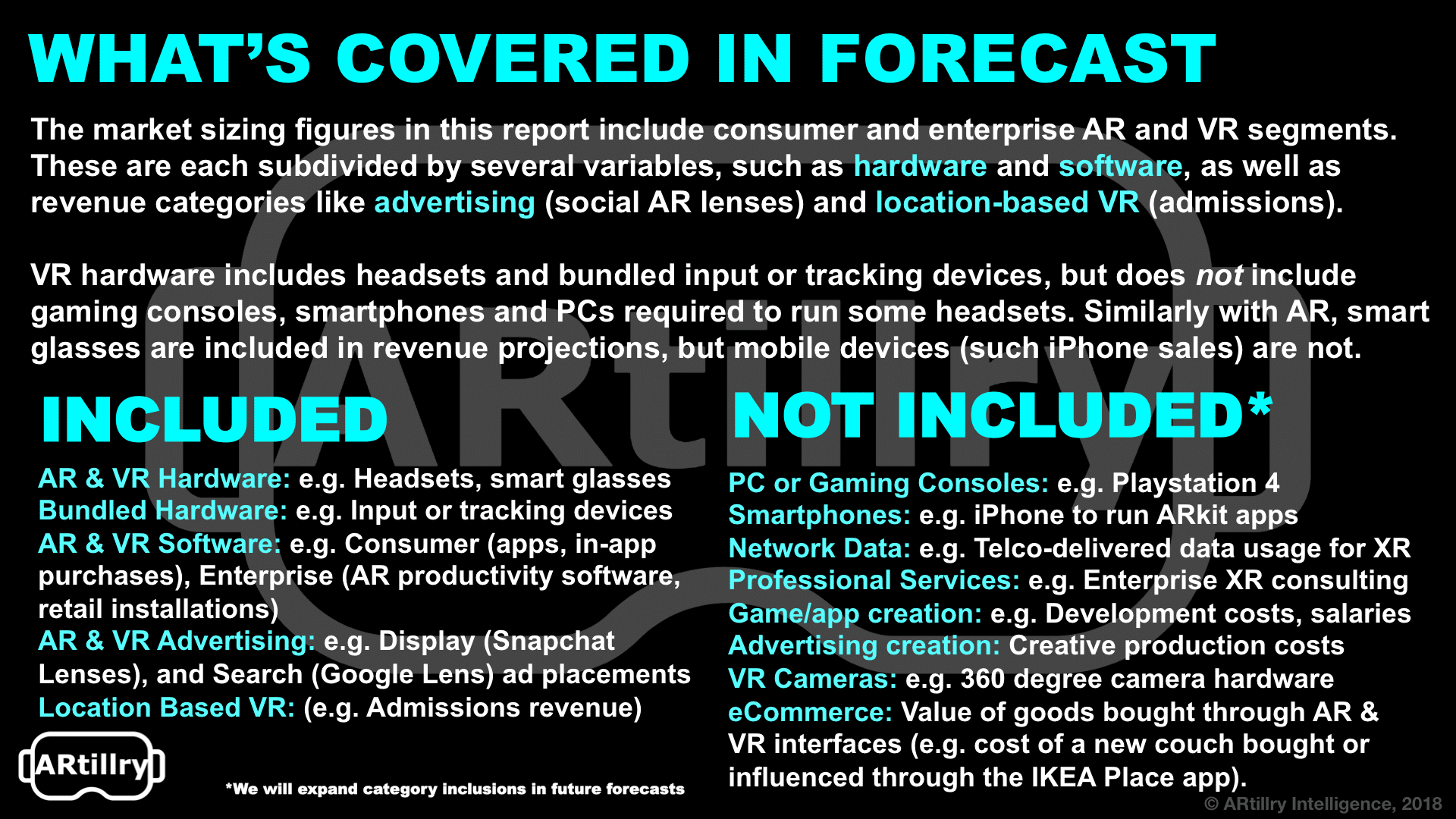

The high-level summary is that total global XR revenues will grow from $3.8 billion in 2017 to $56 billion in 2022. That includes AR and VR, and enterprise and consumer segments of each. They each follow different dynamics, drivers and business models, which guide our financial models.

So where’s that money going? The largest subsegment in outer years is enterprise AR, which will comprise roughly 48 percent of XR revenues by 2022. This is driven by the scale that’s achieved through wide applicability across enterprise verticals; and the business case for productivity gains.

But even despite those advantages, there’s typical enterprise inertia and risk aversion. XR’s momentum will build to a tipping point in 2020, after which we’ll see accelerated adoption. So it will build slow then happen fast, just like with enterprise smartphone adoption about a decade ago.

Historical Lessons

Sticking with AR, its consumer segment is the second largest sub-sector in the outer years of our forecast, with 2022 projected annual revenues of $16.5 billion. And that’s driven by mobile AR in the near term, given its scale and installed base of compatible smartphones.

So that means the revenue source for consumer AR won’t be hardware and smart glasses but rather software from mobile AR apps, and that will evolve from the business model validated by Pokemon go, primarily in-app purchases (IAP). Our consumer survey data also support IAP.

But what everyone’s really waiting for is an AR killer app, which we could see emerge sometime late next year, when AR developers truly gain their native footing. And we believe that will be social or gaming oriented and rely on the development of the AR cloud and other enablers.

As a historical comparison, it took 2-3 years after the first iPhone before we saw killer apps, such as Waze and Uber and Foursquare in the 2010 timeframe. We could see that same timeframe elapsed from last year’s ARkit launch, not to mention the same lesson in native thinking.

Moment of Truth

As for VR, it’s actually the opposite of AR in that consumer markets will lead its revenue growth versus enterprise. That has a lot to do with VR’s form factor alignment with gaming and entertainment. Conversely, its isolation inhibits lots of enterprise use cases (e.g. industrial).

Consumer VR will start to accelerate this year, driven by Oculus Go which carries the advantages of price, a solid spec sheet and a rich content library inherited from GearVR. And with a giftable price tag of $200 we believe that this holiday period will be a moment of truth for Oculus Go..

A lot of this stems from the fact that Oculus – with the advantage of Facebook-backing – has the flexibility to apply loss-leader pricing to trade margins for market share, pursuant to its long game platform strategy. And that applies to the entire line with Go, Rift and Quest next year.

But all of that just scratches the surface… you can check out the report here, the latest ARtillry Briefs episode below and more about our methodology here. Stay tuned for more analysis and narratives as we unpack this massive data set, and continue to update it twice per year.

For deeper XR data and intelligence, join ARtillry PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.