Like many analyst firms, one of the ongoing practices of AR Insider’s research arm ARtillery Intelligence is market sizing. A few times per year, it goes into isolation and buries itself deep in financial modeling. One such exercise zeroes in on mobile AR revenues.

This takes the insights and observations accumulated throughout the year and synthesizes them into hard numbers for spatial computing (see methodology and inclusions/exclusions). It’s all about a strong forecast model and lots of rigor in assembling reliable inputs.

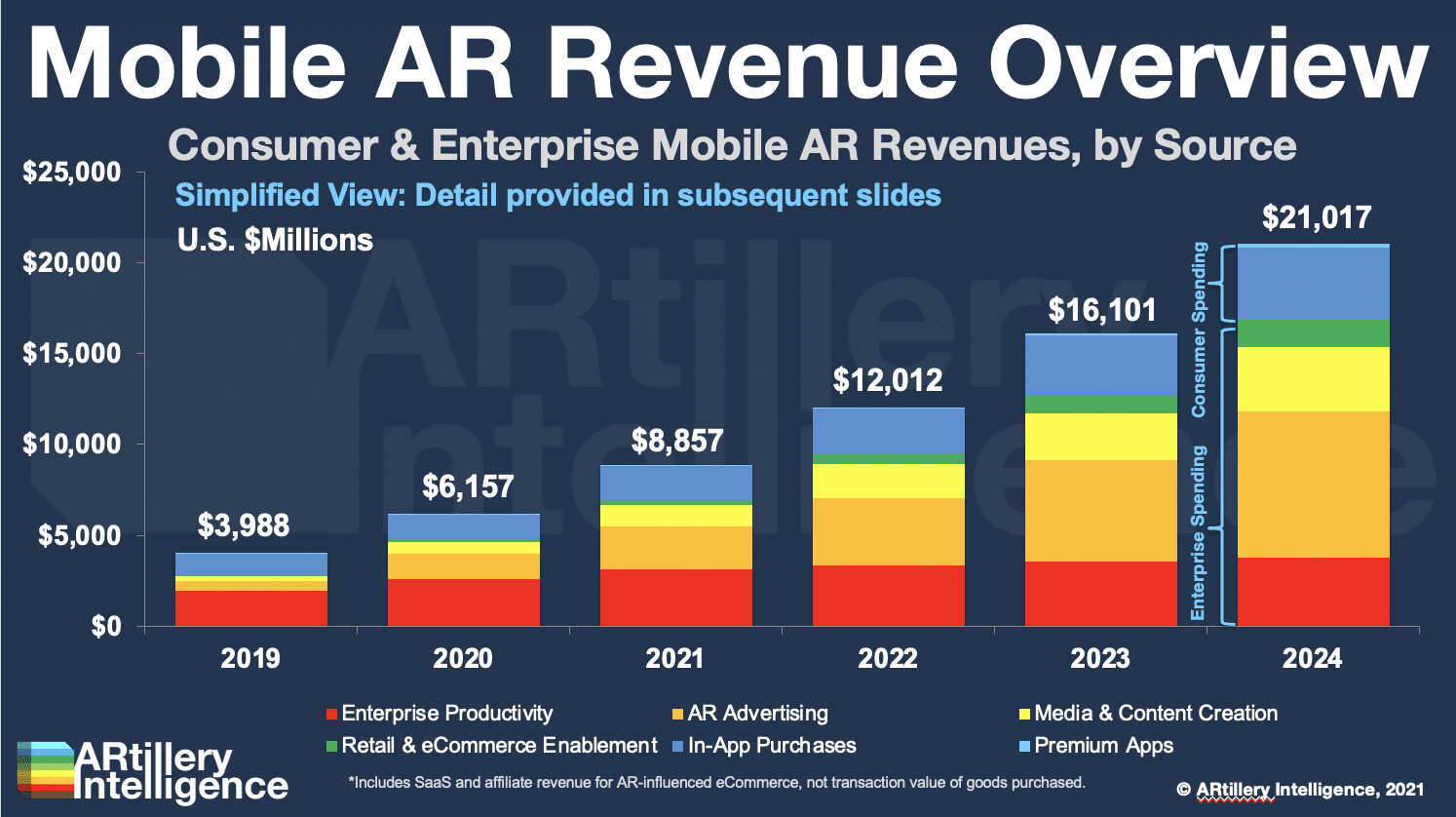

So what did the forecast uncover? At a high level, global mobile AR revenue is projected to grow from U.S. $3.98 billion in 2019 to U.S. $21 billion in 2024, a 39 percent CAGR. This sum consists of mobile AR consumer and enterprise spending and their revenue subsegments.

Picks & Shovels

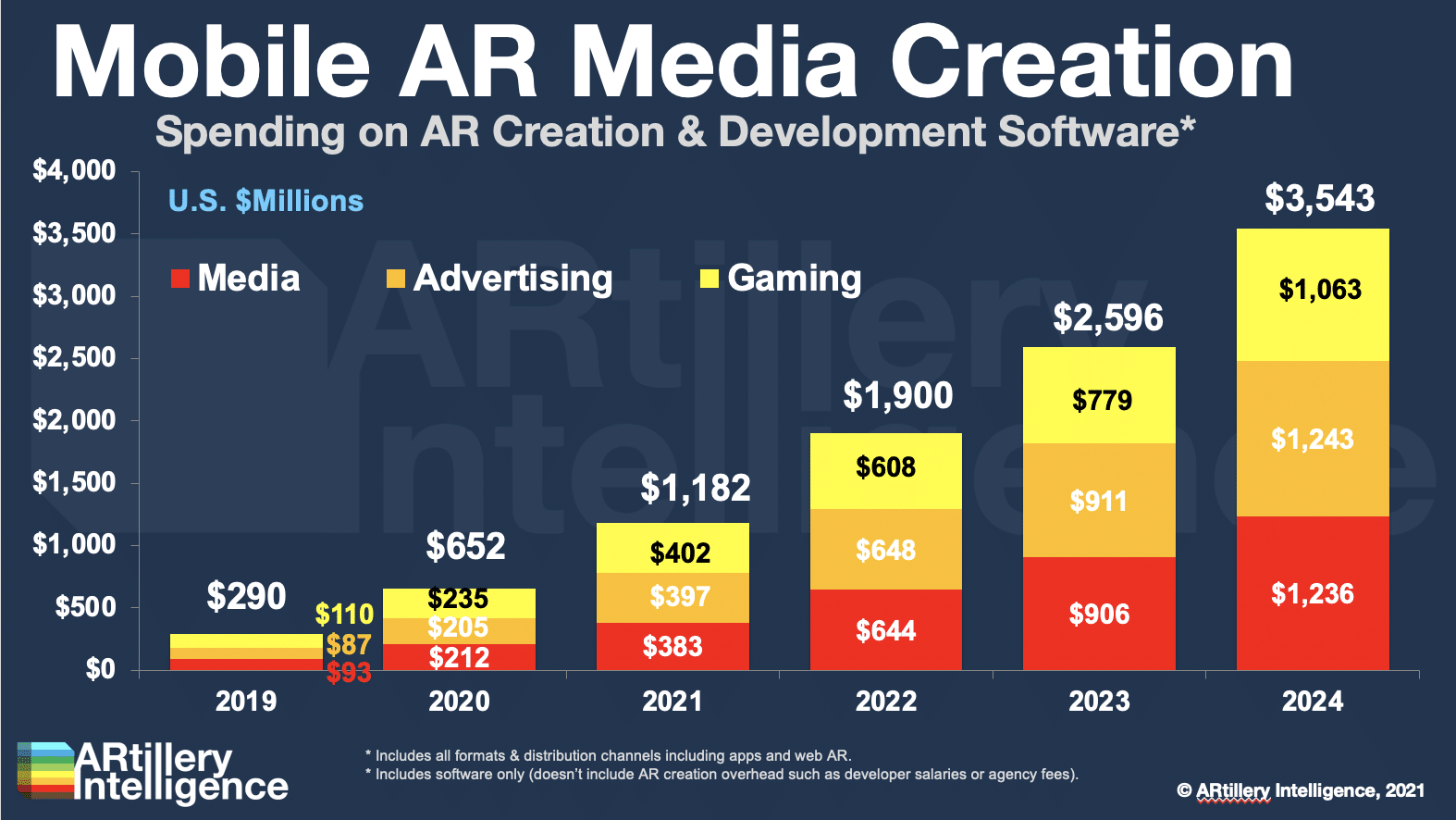

After our last Behind the Numbers segment tackled spending on mobile AR enterprise productivity, we now turn attention to another form of enterprise spending: media & content creation. Here, we’re talking about software that enables companies to build consumer-facing AR.

This spending category is projected to grow from $290 million in 2019 to $3.5 billion in 2024, a 65 percent compound annual growth rate (CAGR). It includes software that enables enterprises or developers to create consumer-based AR experiences such as games, ads & entertainment.

Buyers of this technology (software license or SaaS) include end-users (B2B) or companies that wish to develop AR for their customers and constituents (B2B2C). The latter will be an opportune subsegment of the broader AR industry, as it will represent the proverbial “picks and shovels.”

These functions will grow in demand as AR itself does, as they lower barriers to creation and accelerate time to market. The value is in democratizing AR experience creation. This includes tools like Unity, and several other platforms in the expanding AR creation value chain.

Business Case

As for breakdowns in this enterprise spending, it’s divided fairly evenly across the primary content-creation areas of media, advertising, and gaming. Advertising leads these categories slightly, due to brand AR adoption, and a strong business case with demonstrable ROI.

Spending on Mobile AR media and content creation software is also driven by, and correlated to, the addressable market of AR developers and creatives, which are estimated to reach 1.91 million this year. This includes the global base of AR-active creative professionals and developers.

Of course, the overall universe of creative professionals and developers is much larger: the above figures represent the subset that actively engages in AR creation. Over time, larger numbers could convert to AR, given low-friction tools that target creative pros, such as Adobe Aero.

To further qualify all of the above, this is just one slice of mobile AR spending which in turn is a segment of overall AR revenue (the rest being headworn). We’ll keep a close eye on all of these sub-segments and their shifting revenue shares. Meanwhile, check out the full report here.