What are the variables that impact consumer VR uptake? As examined in ARtillry’s August Intelligence Briefing, they include things like available content. Taking that a step further, there are broader macro factors that have an impact.

An excerpt of ARtillry’s report is below, covering this question. It’s a combination of pricing, hardware advancement and the enterprise market. The latter has the potential to warm up consumers to the idea of VR, and give them a first taste, as we explored last week.

About the report itself: Working with Thrive Analytics, ARtillry authored questions to be fielded through its established survey engine. This first wave of Virtual Reality Monitor surveys 2000 U.S. adults to reveal consumer behavior patterns. Then we built a report around the findings.

Part V: An Expansive Market

This report covers a large portion of the VR market in terms of today’s products and use cases. But in a quickly evolving sector, there are other areas to acknowledge briefly. They include VR’s use in enterprise (productivity, manufacturing, etc.), expansion of headset lines, price and native content.

Enterprise Expansion

Though a lot of attention around VR is fixed on consumers (including this report), there is equal if not greater potential in enterprise contexts. This is due to a clearer ROI in areas like remote collaboration and training, which can reduce travel costs, improve output and other measurable bottom-line impact.

“For us there are clearer benefits in the enterprise,” Presence Capital Partner Amitt Mahajan told ARtillry. “You can really model out what [AR & VR] mean for business, or how much it’s going to affect their bottom line and what that means in terms of a payback period for hardware investments.”

Besides price and ROI, one of VR’s (and AR’s) biggest consumer adoption barriers is style, especially when asking someone to put something on their face. But that’s not an issue at work, when style isn’t really a factor, and where some individuals are already accustomed to wearing safety glasses.

“Almost all of the reasons to not adopt these things as a consumer go away in the enterprise,” said Mahajan. “If you make an employee more effective, or you make it so that they are able to perform a job at all, the form factor does not matter. People will put that thing on.”

Much of these claims apply in an AR context, in terms of graphics guided assembly that enhances one’s field of view. But it can also very much happen in a VR context in terms of employee remote collaboration, or training. Walmart for example has recently adopted VR to train its employees.

Headset Expansion

This report examines the most prevalent headsets in the market. But that market is about to expand significantly. As capability improves and costs come down for VR components, we’ll see Tier-1 VR capabilities packaged in smaller and more portable formats. This will drive new market entrants.

For example, Microsoft’s Windows Mixed Reality (WMR) platform is being licensed to manufacturers such as Lenovo and Acer to build lower cost VR headsets that operate in tandem with Windows 10. These will exist somewhere between Tier 1 and Tier 2 in terms of quality, and be priced around $400.

Price Competition

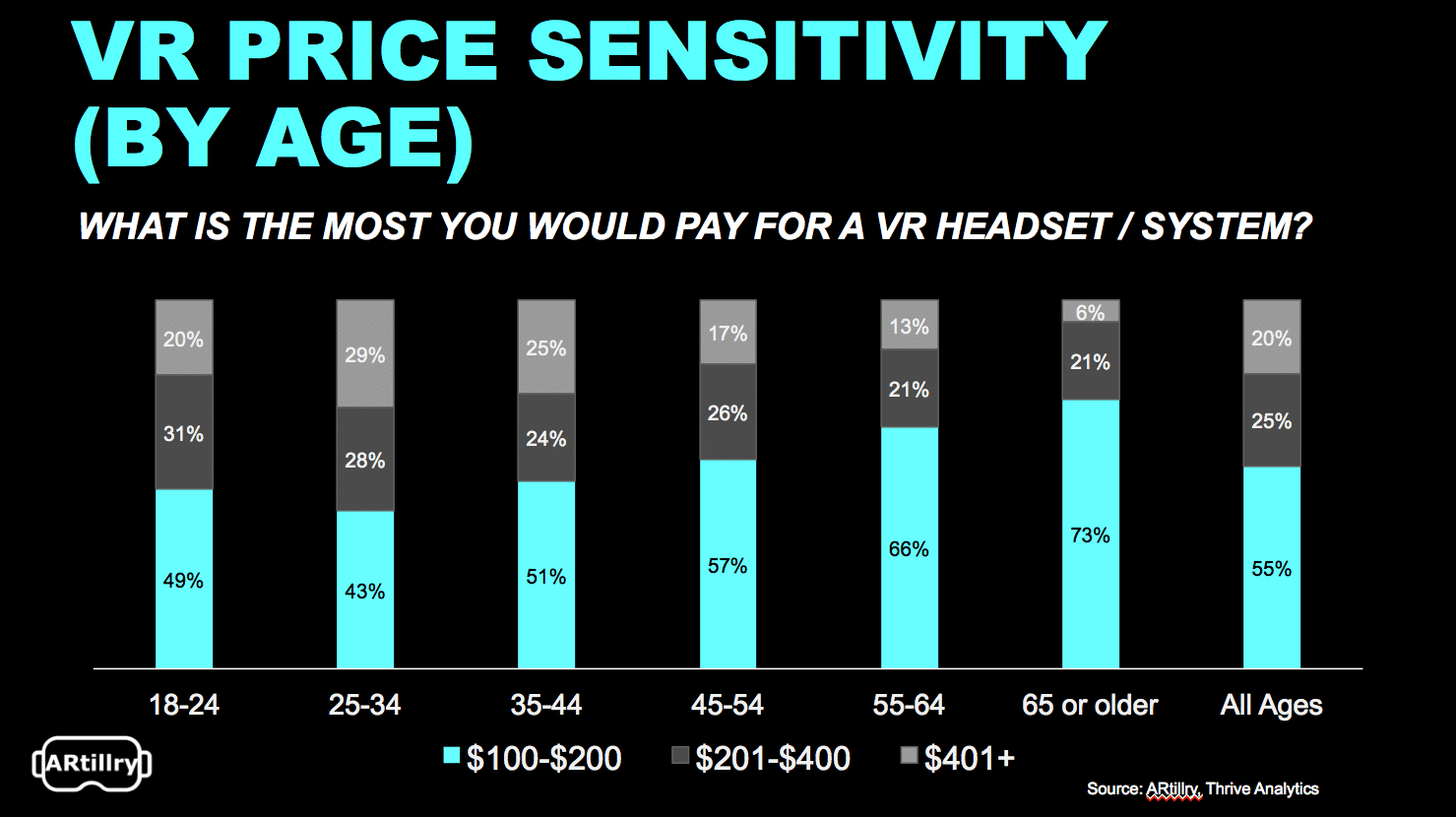

$400 is a significant price point examined throughout this report. It’s also the price that Oculus chose for its “summer of Rift” sale. Initiated in July, and returning to $499 in September, it has successfully boosted sales, according to Oculus. It also prompted HTC to lower the Vive price from $799 to $599.

These prices again must be qualified with the caveat that a PC with high-end graphical processing is required. So the “all-in” price for Rift and Vive usually exceeds $1000. The PSVR is $399, while the PS4 console is $399 and necessary peripherals can be $100+, altogether approaching $1,000.

Tier-2 headsets (Gear VR and Daydream View) cost between $59 – $129, and don’t require a dedicated PC. They do require a compatible smartphone, but that cost can be negated for consumers who consider a smartphone an already fixed/sunk cost in their lives (most U.S. consumers).

ARtillry believes we’ll see continued price competition, as emerging tech sectors often involve trading margins and unit economics for market share. The latter can produce greater long-term value, given that “platform wars” can be won on gaining early market share through device penetration.

This can have a domino effect, as content volume on a given platform is a function of the size and quality of the developer network working with that platform. Those developers are in turn attracted to platforms with the greatest revenue potential, which are often those with the greatest installed base.

And that starts with device penetration and competitive pricing. The lesson is to watch headset pricing and adoption as leading indicators for VR opportunity. Media companies looking for brand extension, for example, should develop apps on platforms with greater reach and demographic alignment.

Native Content

The most successful VR apps will apply “native thinking,” meaning they’re built specifically for the form factor. In other words, those that utilize the unique aspects of VR immersion tend to perform best. Those that take existing 2d media and shoehorn it into a VR view conversely do not resonate.

This is analogous to the “native thinking” that was a success factor among smartphone apps. Apps that utilize the unique hardware functions (accelerometer, GPS, camera, etc.) generally outperform those that simply put existing media on a smaller screen. The same principle will apply in VR.

Therefore, it’s surprising to see activities like watching movies – a 2D format – score high on desired VR activities in VRM. The previous statement isn’t meant to disparage consumer’s stated interest, but to hypothesize that many won’t know what they want until they try VR, as examined earlier.

In fairness, many of the high-ranking activities reported by VRM respondents do indeed have capacity for immersive and native experiences. These include exploring the world, watching sports, test driving a car, and social interaction. ARtilllry believes these areas represent strong business opportunities.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.