There’s been a lot of excitement over mobile AR. But to really quantify the opportunity requires a deeper look at the installed base of AR-compatible devices. So ARtillry set out to do just that in its latest report, ARCore & ARkit: The Acceleration of Mobile AR.

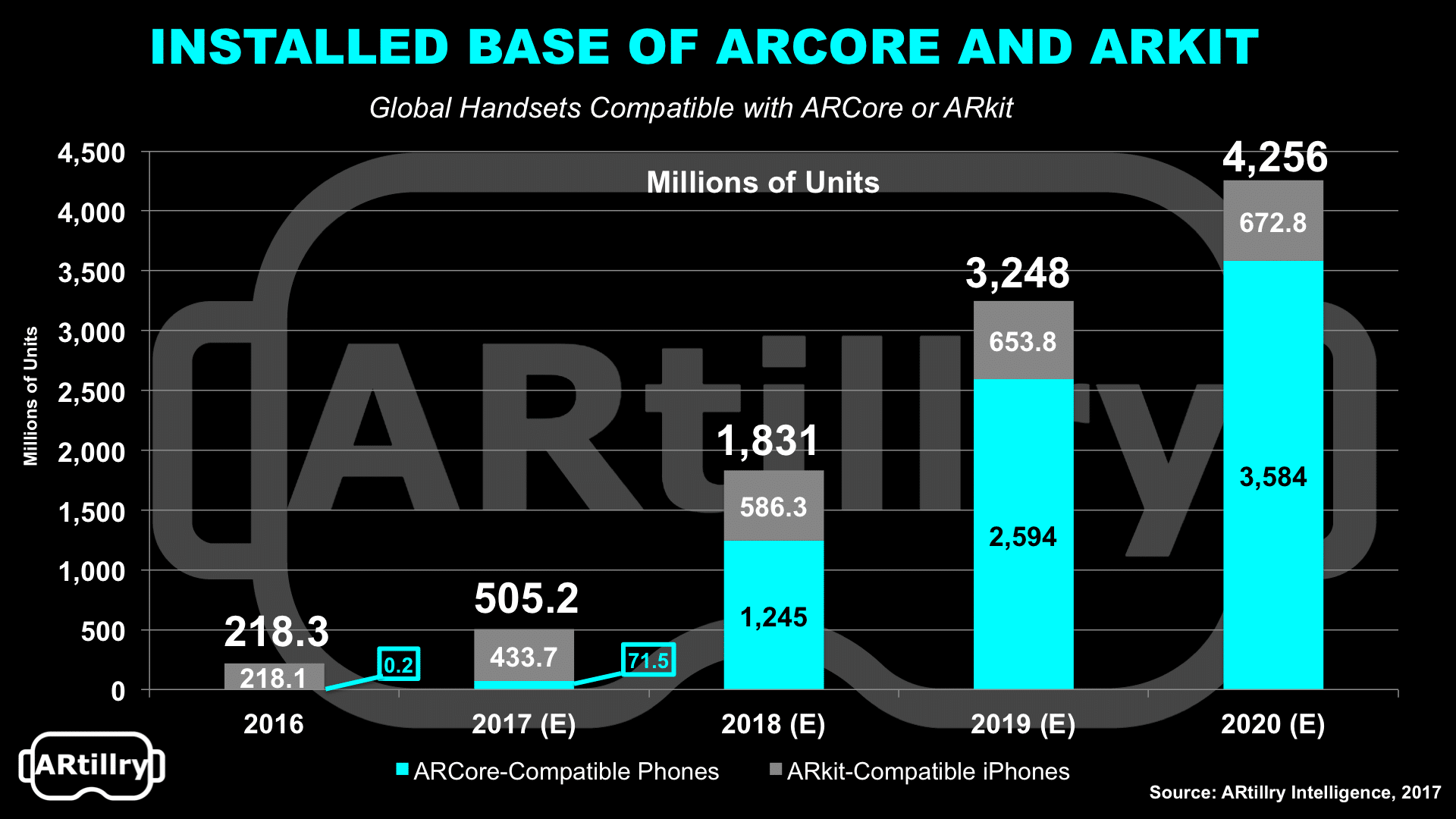

The verdict: There will be a half-billion AR-compatible smartphones by the end of 2017 and 4.2 billion by 2020. That may seem like steep growth, which it is, but it’s a function of hardware replacement cycles for iOS and Android (2.5 years), which will turn over rapidly.

How will it come together? Competition between Google and Apple — stemming from their battle positions in the smartphone era — will intensify and drive mobile AR. That will be a double edged sword: competition is good but it also fragments the market with two platforms.

One thing that’s clear is Apple has the short-run reach advantage. This is due to a more unified hardware and software set that supports wider ARkit compatibility. But Google will have the longer-term scale as ARCore compatibility cycles into the larger Android universe.

That will take longer for ARCore, given a fragmented base of Android devices that makes it difficult for Google to mandate AR-capable optics, and to push software updates comprehensively. In fact, only 16 percent of Android devices usually run OS versions released in the previous year.

Beyond OS are hardware specs, such as optics and sensor calibration. Currently the Pixel, Pixel 2 and Samsung Galaxy S8 are compatible with ARCore but we’ll see more OEMs comply over time, starting with Huawei, Asus and LG. For ARkit, iPhones 6s or later have the goods.

ARkit and ARCore also carry their parents’ DNA. For Apple, it’s all about apps; for Google, the web. For developers, that means ARCore could reach more users, but ARkit could be more monetizable though standard app revenue models (i.e. downloads, in-app purchases, etc.).

There’s a lot more to it of course, covered in the full Intelligence Briefing. You can read an excerpt below, covering the report’s key takeaways, and stay tuned for lots more.

Key Takeaways

Competition between Google and Apple has intensified over the last decade’s “mobile OS wars.”

— Now those OS’ respective AR development kits represent the next competitive battleground.

— Like the mobile OS wars, mobile AR will force platform decisions from developers and users.

Disappointing AR & VR headset adoption has shifted attention and investment to mobile AR.

— There are 3.2 billion global smartphones today and ARtillry projects 4.6 billion by 2020.

— ARCore will reach 3.6 billion smartphones during this time, and ARkit will reach 673 million.

— This installed base will incentivize developers to place AR into the hands of billions.

— Compatibility will start slow but grow fast over the next phone replacement cycle (2.5 years).

ARCore and ARkit work with standard RGB cameras found in most smartphones.

— Developers don’t have to build AR technology from scratch, nor rely on physical barriers like — markers or depth cameras. They can focus instead on end-user experiences.

ARkit has a slight head start in developer interest and invested time.

— ARkit also has technical advantages in its mapping and iOS development stack (i.e. Metal and Swift), which create more elegant integrations with ARKit.

— Apple’s classic vertical integration of hardware and software gives it greater control over things like camera optics and software updates.

ARCore has a longer-run advantage in attracting developers, due to Android’s greater scale.

— ARCore is also more open, with a broader arsenal of lower-friction development tools (Tilt Brush and Blocks) and support from adjacent software (Daydream, Tango and Lens).

— Google is banking on web delivery for AR, accessed through interlinked mobile websites instead of Apple’s friction-heavy and siloed app approach.

Regardless of platforms and the apps built on them, data will be the unsung hero of AR.

— Geo-relevant data (store or product information) will be critical.

— Object recognition data will let AR apps tap into previously chartered territory (area mapping), lessening the mobile compute burden for new AR experiences.

— These data assets will be most effective if shared openly in a cloud repository.

AR success will result from “native thinking.” Build for the capabilities and limitations of the medium, rather than that of legacy formats (a classic pitfall of new technologies).

— AR Success factors will also come from new modalities such as audio (sound “overlays”).

Attracting developers will be critical (between ARCore and ARkit, and from other sectors).

— Due to mobile AR’s capacity for scale, it will attract VR developers with transferable 3D design and modeling skills, or experience with game engines like Unity.

— Yesterday’s VR developers will be today’s mobile AR developers and tomorrow’s AR glasses developers – the ultimate AR endgame.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.