This post is adapted from ARtillry’s latest Intelligence Briefing: Mobile AR: App Strategies and Business Models. It includes some of its data and key takeaways. More can be previewed here and subscribe to access the full report.

Most people think of AR as smart glasses that overlay graphics and information in one’s immediate field of view, a la Google Glass. And that’s certainly a form factor being deployed in enterprise environments, as examined in last month’s ARtillry Intelligence Briefing.

But it’s also a form factor with long-term consumer potential. Intel projects consumer smart glasses to inflect around 2027 with 50 million annual unit sales, growing to 200 million by 2031 . The rationale is that smart glasses’ consumer value and utility at that point could parallel that of today’s smartphone.

But until then, AR glasses don’t pass stylistic requirements for consumer markets (size, weight, cost etc.). So consumer AR’s ruling form factor in the near term will be smartphones. You probably know the format: graphical overlays that interact with the world seen through your smartphone camera.

Further positioning the smartphone as a vessel for AR is its ubiquity and permanence as a fixture in our lives. And in addition to volume, smartphones have the goods when it comes to necessary hardware components to run basic AR, including image processing, sensors and camera.

Accelerating that capability, Apple’s ARkit and Google’s ARCore have standardized the development tools and democratized mobile AR app creation. And early apps like Pokémon Go and Snapchat – though they’re not “true AR” – put mobile AR on the map and have acclimated consumers en masse.

Adding up all these factors, mobile AR is in a strong position for growth. But it also faces some challenges and is off to a slow start. In fact mobile AR today resembles iPhone apps ten years ago – underdeveloped in product capability, standards, consumer demand and several other factors.

That makes it an opportune but also challenging period. For developers, startups, brands, media companies or anyone else that wants to explore Mobile AR opportunities, the best thing to do is stay informed. That means examine today’s best practices, historical lessons, and market trajectory.

We’ll do just that in the following pages, with the goal of informing mobile AR business strategies. That will include surveying the landscape of current product and business models, and looking to historical lessons that still apply from the smartphone era. We’ll start by quantifying the opportunity.

Mobile AR: By the Numbers

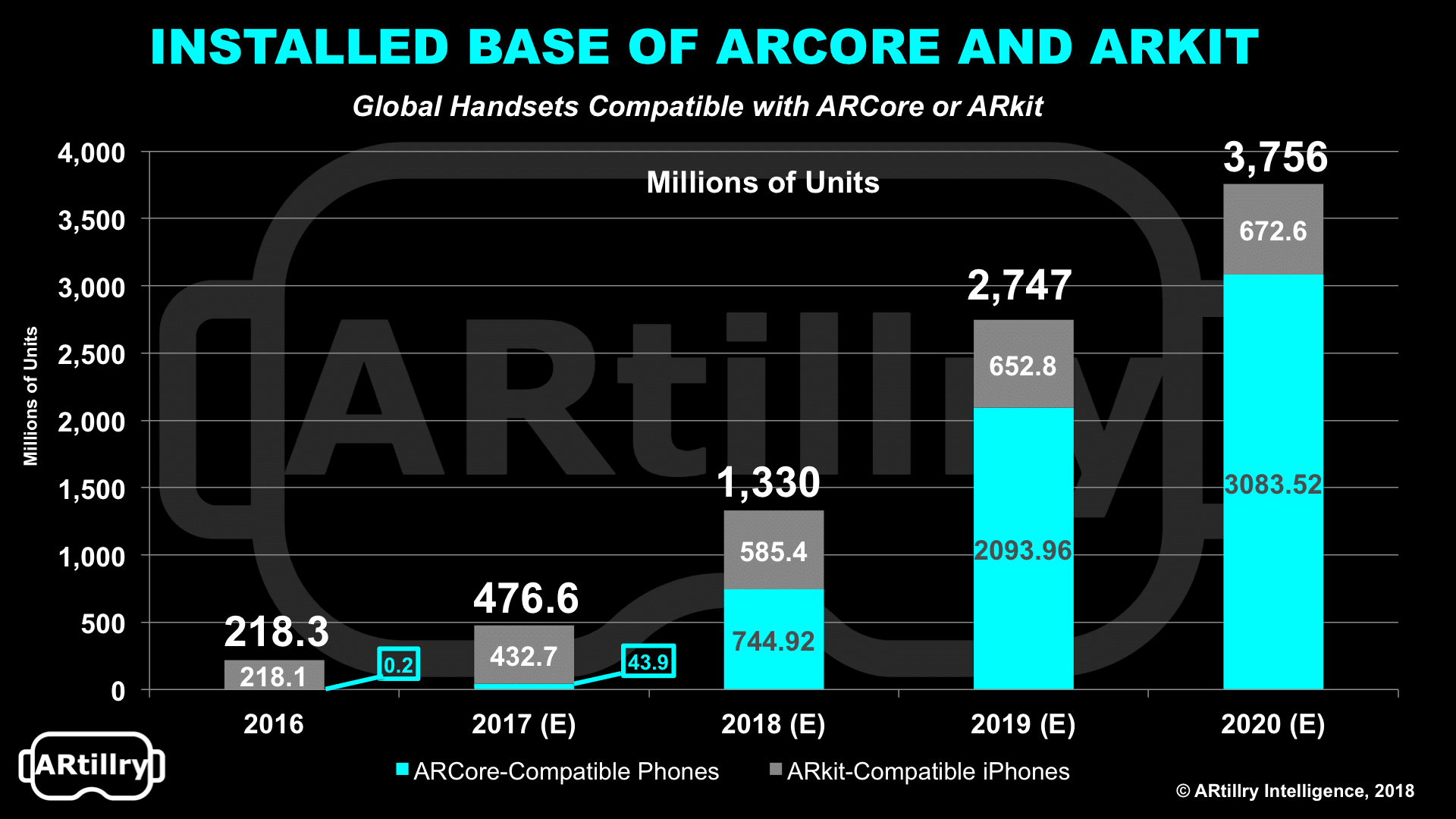

To put a number on claims made above regarding smartphone ubiquity, there are 3.5 billion global units. But more relevant for this report, how many are AR-compatible? That figure is 476 million today, growing to 1.3 billion by year-end, and 3.8 billion by 2021 – a meaningful installed base.

This volume is mostly due to Apple’s ARKit and Google’s ARCore, which apply software to make AR possible on previously un-compatible hardware (such as standard RGB cameras). Between the two, ARCore has a minority share today but will eclipse ARkit soon, due to Android’s larger installed base.

One question that arises from these figures is why are they growing so rapidly. They over-index for growth rates when compared to several growth-phase industries in the forecasting trade. For both ARCore and ARkit, they go from zero to billions over a five-year period, which should raise questions.

One reason is that the metric is unit-compatibility, not dollars. Another reason is average mobile hardware replacement cycles, which follow a set pace (currently 2.5 years). This will cause AR-compatibility – for example, A9 chips or greater in iOS devices – to cycle in rapidly.

As for the qualitative differences between ARCore and ARkit, we’ll cover those later in this report. These differences and strategic positioning are important, as platform choice is a key consideration for mobile AR developers. This was also covered in a past ARtillry Intelligence Briefing .

Mobile AR: In Dollars

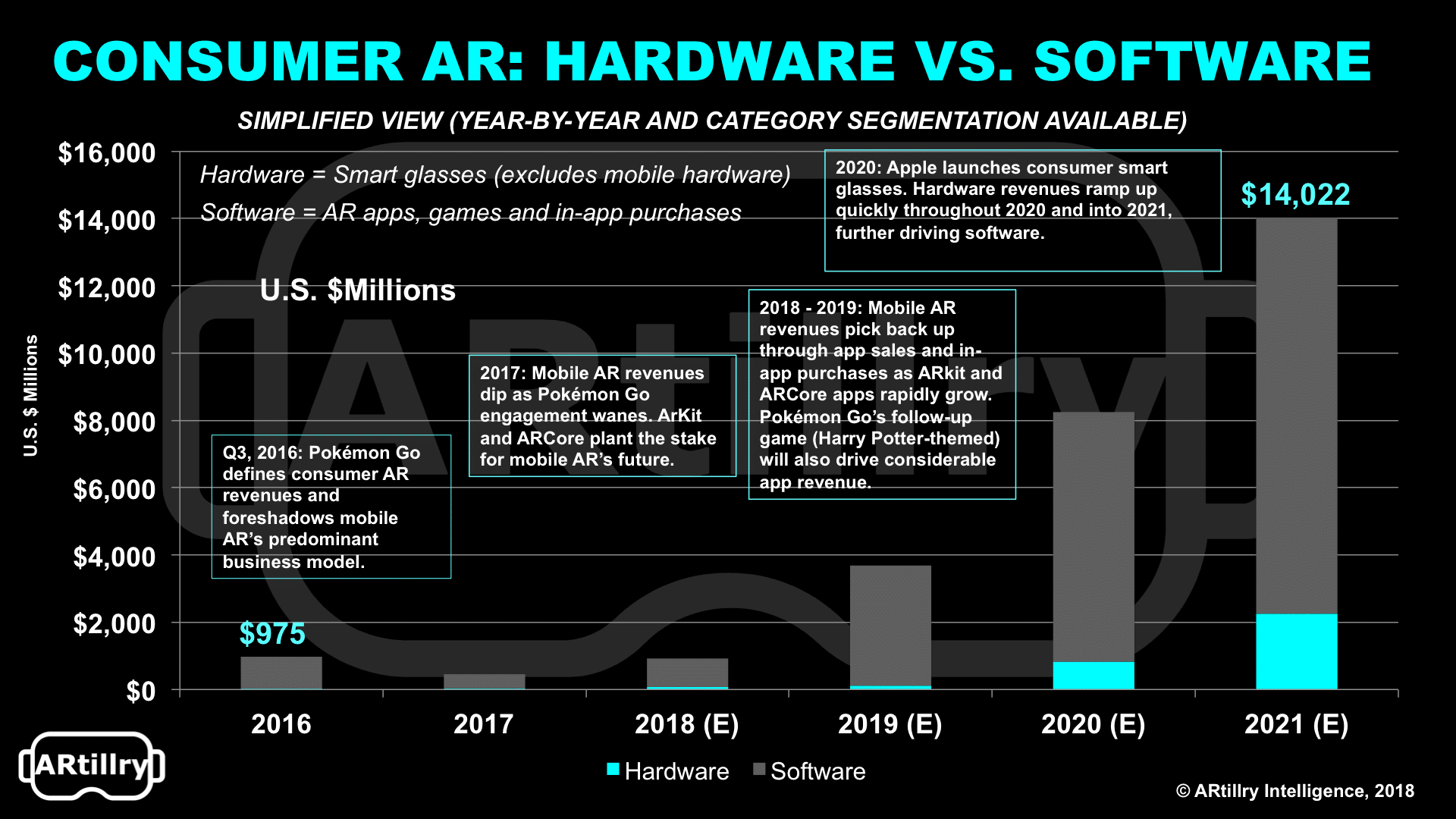

Beyond unit penetration, how does consumer AR stack up in dollars? According to our projections, it will grow from $975 million in 2016 to $14.02 billion in 2021. These figures include smart glasses, though it’s important to note that mobile dominates near-term revenue, for reasons explored earlier.

Segmenting mobile’s share – the focus of this report – It’s represented by the software portion of the below projections. This is because smartphone hardware (e.g. iPhone sales) isn’t counted in our forecast because it’s an already-existing and ubiquitous consumer purchase.

Therefore, the near term opportunity for mobile AR is in software. That broad designation includes several components, including premium app sales, in-app purchases, micro-transactions, and several other things. These are broken down further in the “business models” section of this report.

Zeroing in on just that software portion of consumer AR revenues, it will grow from 950 million in 2016 to 11.8 billion in 2021. After 2020, AR hardware will start to grow in share, as smart glasses become more viable for consumer markets including cost, style, battery life and other technical specifications.

This could include Apple’s rumored smart glasses in the late 2020 time frame. It will also include AR glasses in niche or enthusiast areas like cycling, skiing and other sporting/recreational areas. Notice that these are areas where glasses or goggles are already worn, forcing less of a behavioral shift.

But until then, the consumer AR sector will be dominated by mobile, with most of the strategy and differentiation happening within software (apps), rather than hardware. So what are those app strategies? We’ll spend the rest of this report examining different versions of that key question.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.