“Behind the Numbers” is ARtillry’s series that examines strategic takeaways from its original data. Each post drills down on one topic or chart. Subscribe for access to the full library and other knowledge-building resources.

Many of us agree that XR will be transformative. But it’s a matter of when and how much. So ARtillry Intelligence ventured to quantify the revenue outlook in more precise terms. The result is our latest XR revenue forecast. This week we examine the consumer VR portion.

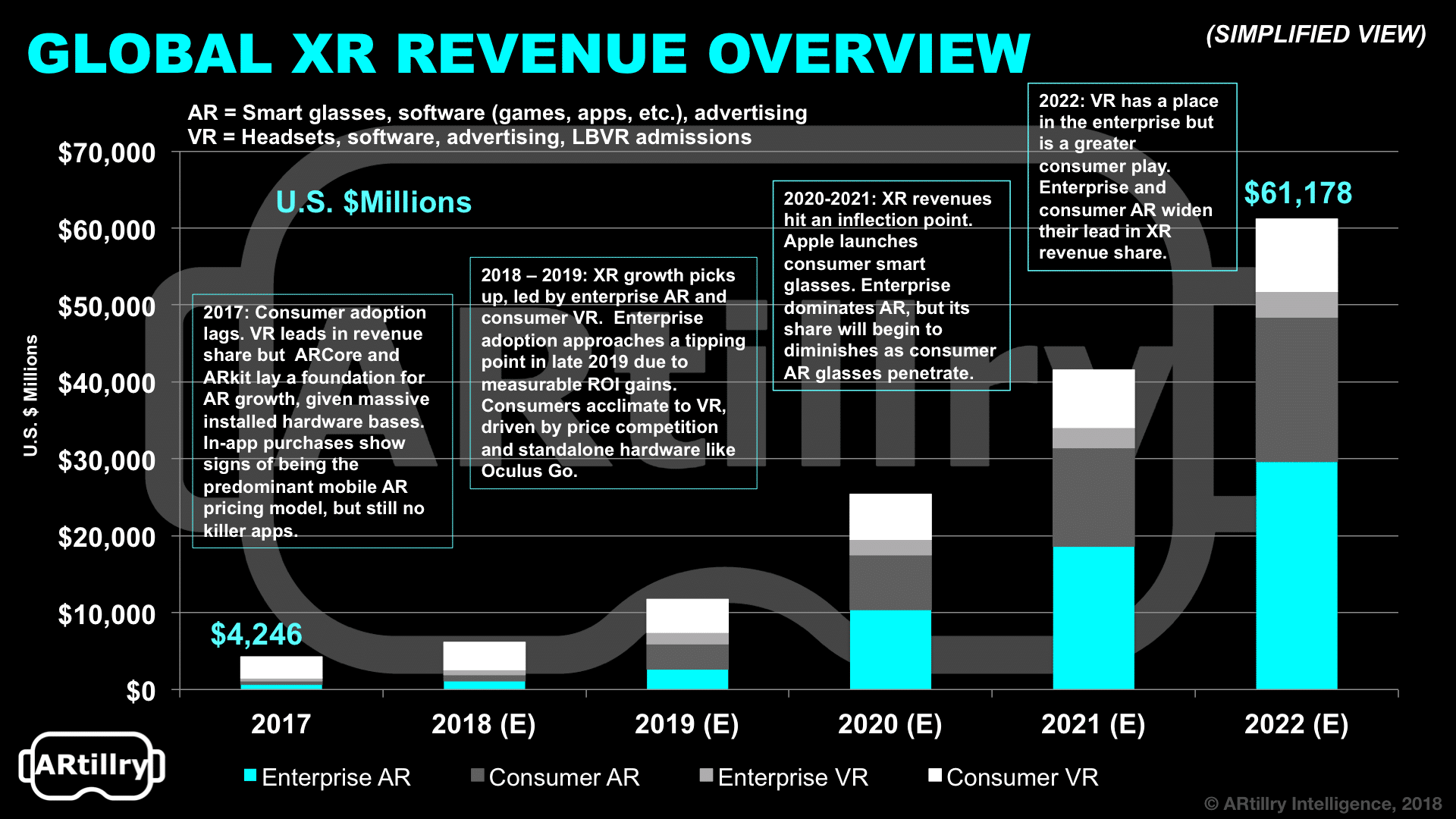

But before we do that, what’s the overall XR revenue outlook? We project it to grow from $4.2 billion in 2017 to $61 billion in 2022. That includes AR, VR, and enterprise and consumer segments of each. Those are then subdivided by hardware, software and advertising revenues.

So where’s that money going? The largest sub-sector is enterprise AR, which will comprise roughly 48 percent of all XR revenues by 2022. That has a lot to do with the scale achieved through wide applicability across enterprise verticals; and a form factor that supports all-day use.

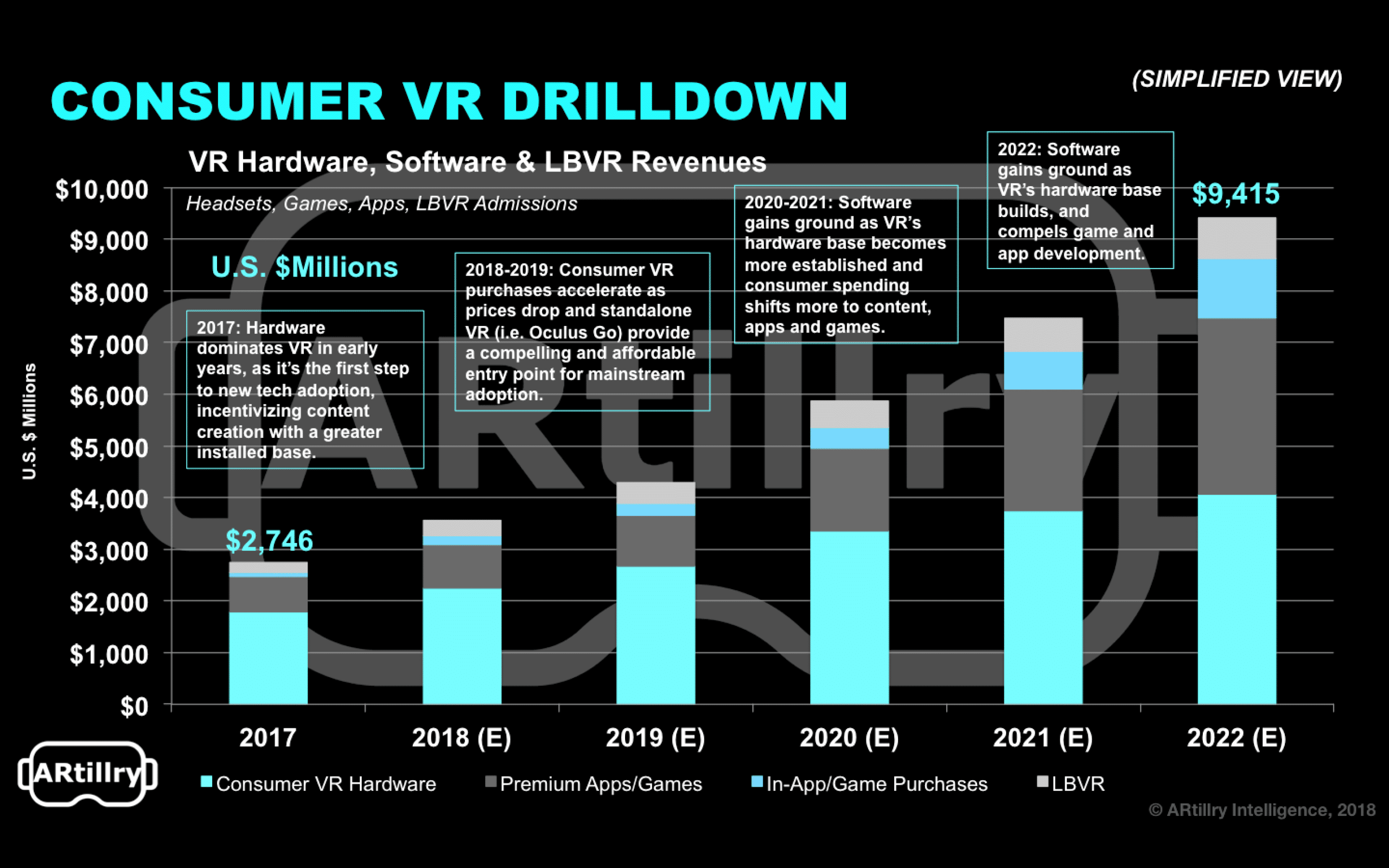

Moving on to Consumer VR, it’s the third largest revenue category in the outer years of the forecast, right behind consumer AR. Specifically, we project it to grow from $2.7 billion in 2017 to $9.4 billion in 2022, a 28 percent compound annual growth rate (see figures below).

Like enterprise VR, it will be hardware-dominant in early years as its installed base is established. Over time, software (in this case, games and apps) will eclipse hardware revenues with a faster refresh cycle. This hardware/software interplay is common as tech sectors mature.

A greater installed base of hardware will also incentivize VR content creators to invest in development, resulting in more robust VR libraries and greater software spending per user (ARPU). Historical parallels for this dynamic can be seen in mobile apps and console gaming.

Premium apps will dominate software revenues but in-app purchases will contribute, especially in gaming. The opposite is true in consumer AR, where mobile dynamics cause in-app purchases to dominate. Installed software and apps will rule early years, losing share to WebVR in later years.

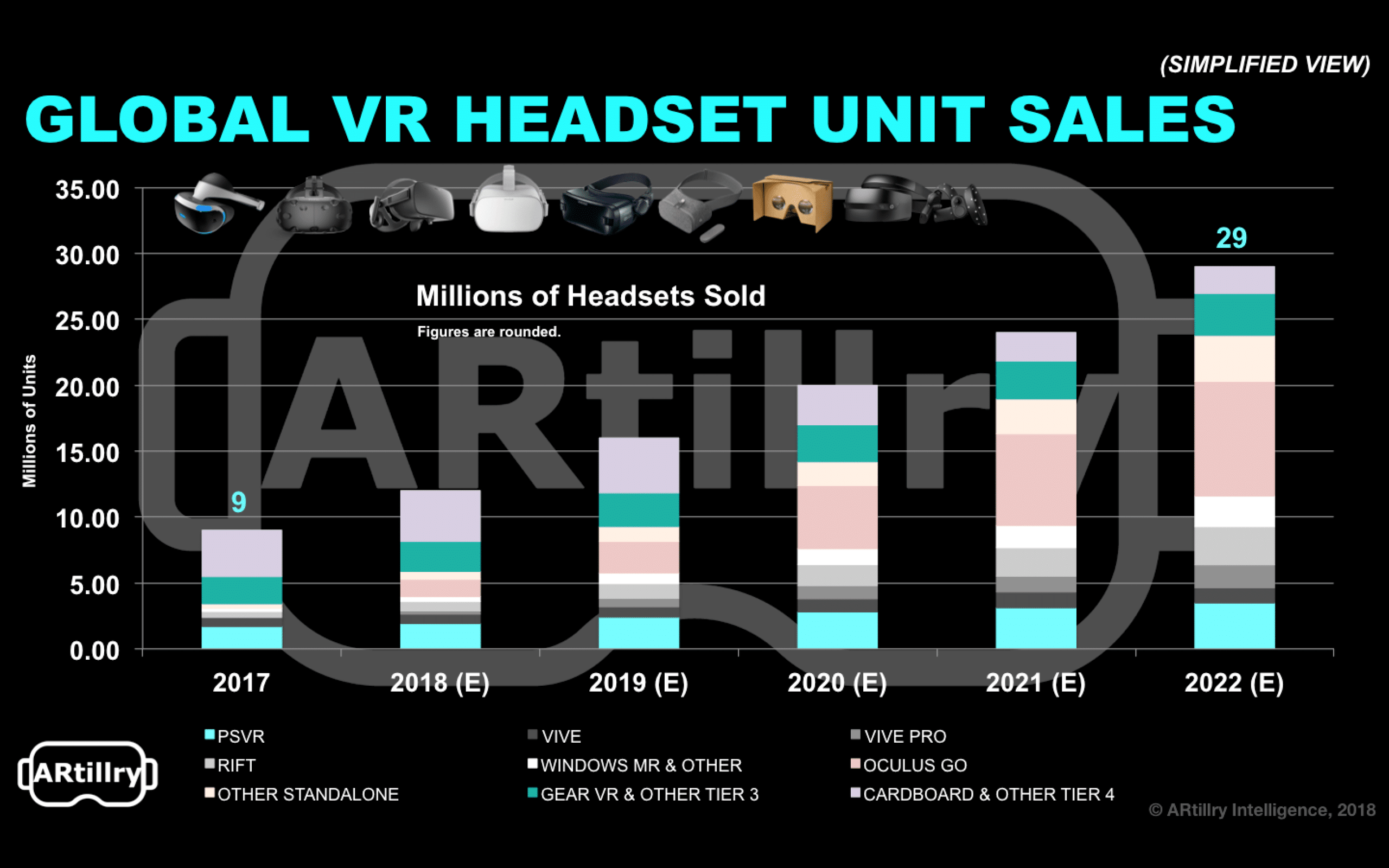

Price competition among VR headset manufacturers (e.g. Oculus, Sony, Samsung) will meanwhile accelerate consumer adoption. Oculus Go, at a $199 price point, hits a sweet spot for quality and affordability, and we project it to reach unit sales of 1.3 million this year.

Oculus – with the advantage of Facebook-backing – has the flexibility to apply loss-leader pricing in order to trade margins for market share. That will give it a strong competitive position versus players that are dependent on hardware revenue (i.e. HTC, Samsung).

But much of this will be proven in the coming months as we see if Oculus Go can reach these price-motivated penetration levels. Given a giftable price point, and solid specs/performance, we believe that the the 2018 holiday quarter will be a “moment of truth” for Oculus Go.

This will all be a moving target and the above just scratches the surface. Stay tuned for more data slices from this forecast, which we’ll unpack in the coming weeks. Subscribe for the full report and preview more of it here, including methodology and breakdowns of what’s included in the figures.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.