“Behind the Numbers” is ARtillry’s series that examines strategic takeaways from its original data. Each post drills down on one topic or chart. Subscribe for access to the full library and other knowledge-building resources.

100 million units is a sort of “magic number” when it comes to consumer hardware. As we saw with smartphones circa 2008, that milestone creates a level of ubiquity that incentivizes developers, content creators and a healthy ecosystem of supporting technologies.

“If there isn’t at least a near term probability of 100 million devices in the marketplace that can play it, [developers] won’t build,” Unity CEO John Riccitiello said last year. “A couple hundred million devices creates an umbrella for the industry to flourish… we’re a few years from that.”

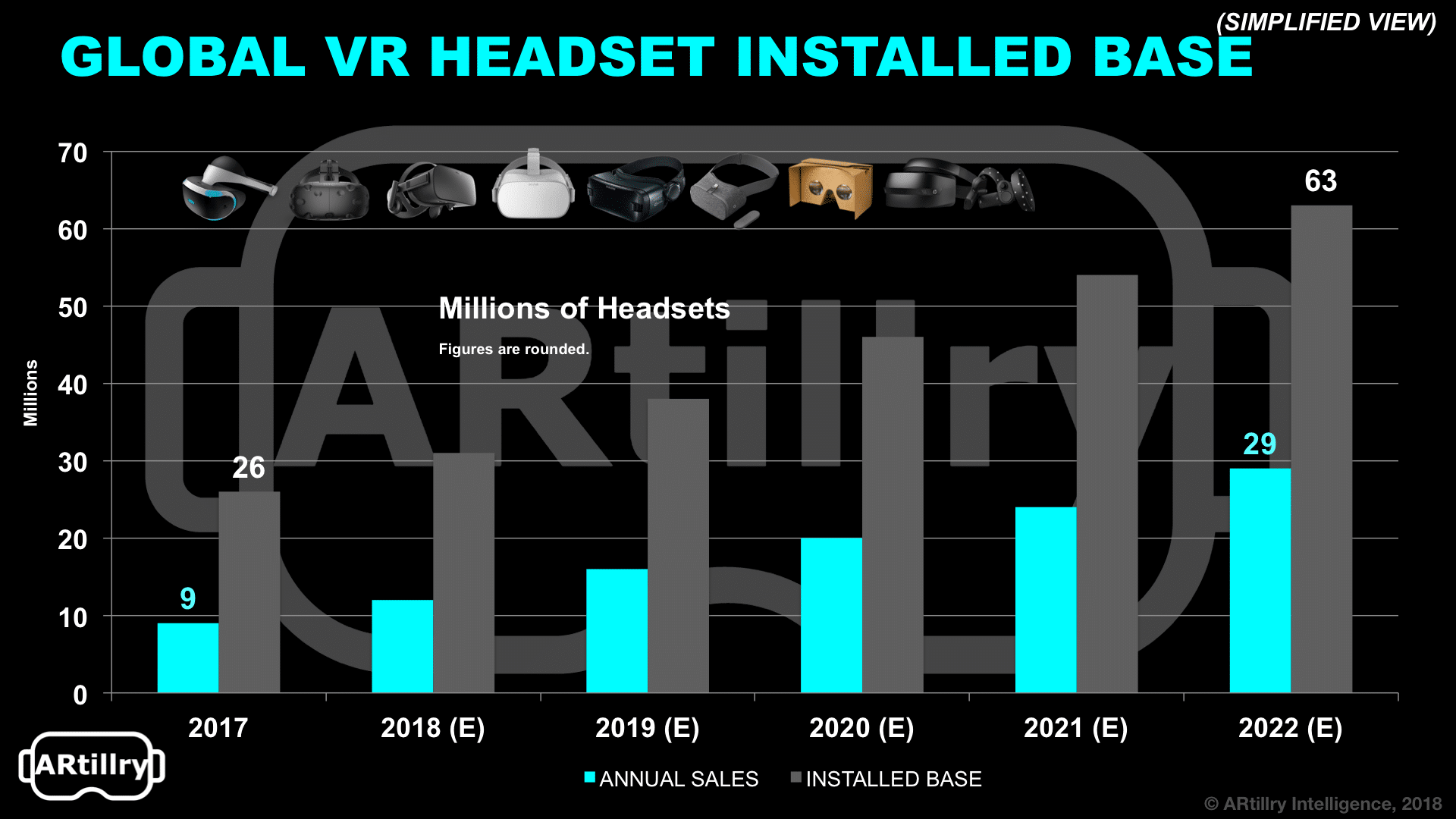

With that backdrop, where are we with VR headsets? The current installed base is about 30 million units which includes lots of Google Cardboard (breakdown below). Another question is when we’ll reach 100 million units. Our projections put it somewhere between 2022 and 2025.

To clarify, installed base is a different metric than annual sales. Given a replacement cycle of 2-3 years, an installed base is a cumulative measure of active devices in market. It builds over time as a function of new sales and as older units that cycle out, which we measure in our forecast.

One challenge for the VR industry is that sales growth has slowed over the past year. After a surge of excitement and early adopter sales in 2016 and early-2017, demand receded a bit. One saving grace is proposed to be the $200 Oculus Go, and its holiday 2018 “moment of truth.”

Not only is $200 a giftable price point, but it’s the price under which demand and interest inflect according to our VR consumer survey. Beyond price, the lack of on-boarding friction, setup and wires make Oculus Go (and other standalone headsets) a lot more mainstream friendly.

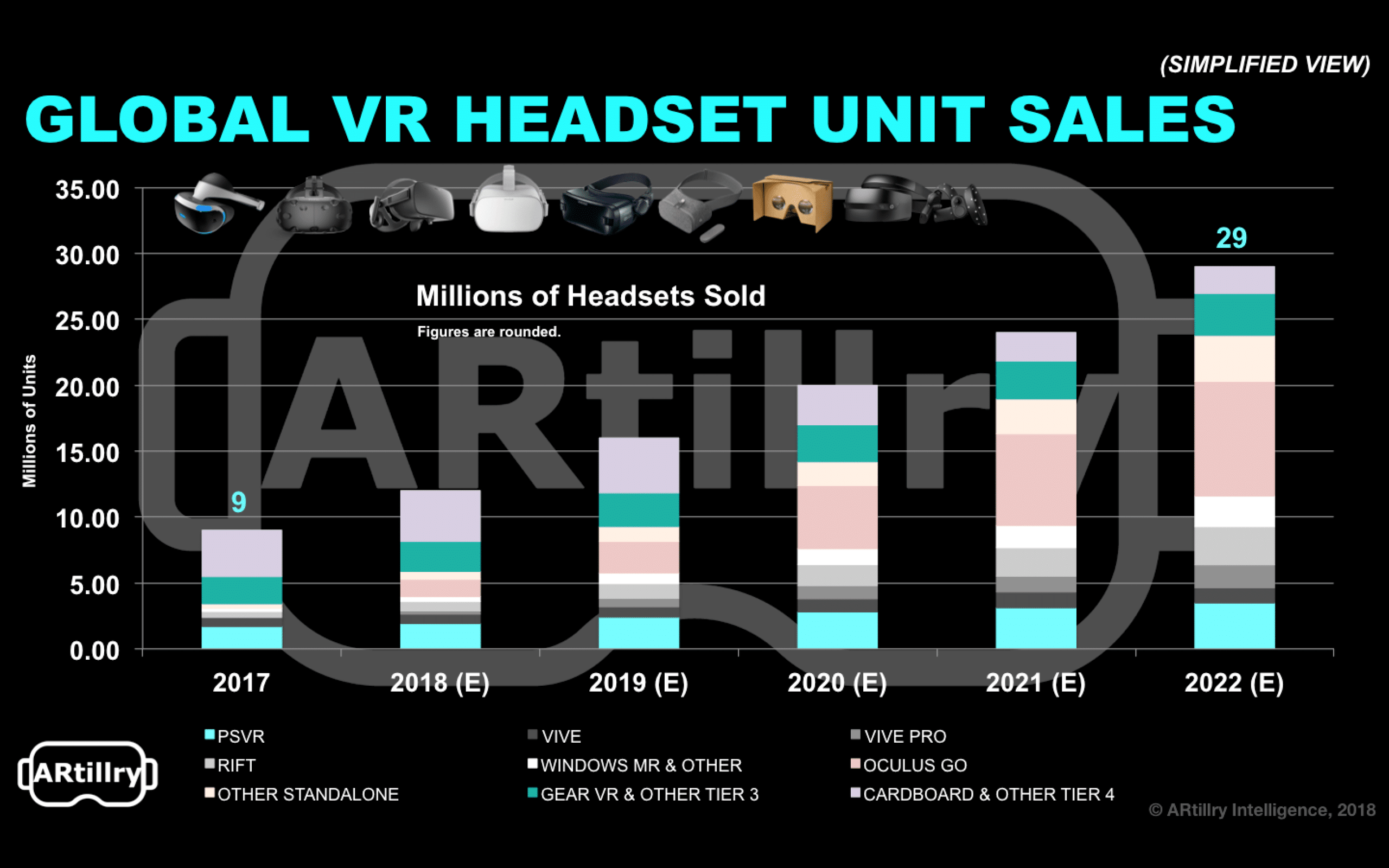

These are all the reasons why we’re fairly bullish on Oculus Go, further fueled by Oculus’ loss-leader pricing and content investments. Segmenting by device (see above) shows a potentially strong future for Oculus Go, including 1.3 million unit sales we project for 2018.

Further breaking down headset market shares, it should be acknowledged that the majority of in-market headsets are lower-tier units including Cardboard and Gear VR. If you just count tier-1 headsets (Rift, Vive, and PSVR), headset sales are a lot lower and mostly led by PSVR.

Tier 3 (mobile VR) sales growth has also slowed, which has a lot to do with discontinued promotions. The leading player in that tier, Samsung, ran several promotions in 2016 & 2017 that involved free Gear VR headsets with the purchase of a Galaxy S8 or other compatible phone.

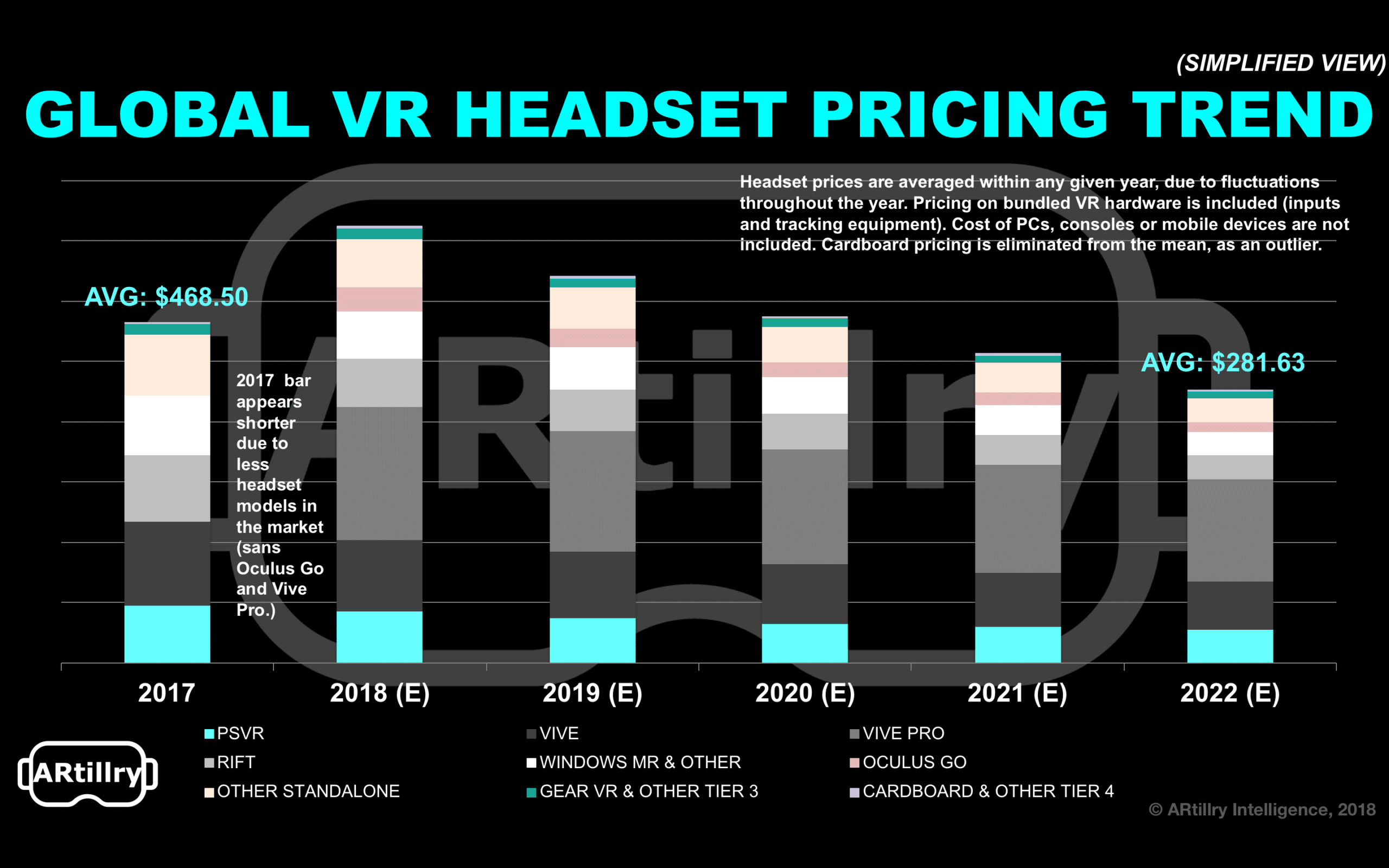

Back to pricing, the entire industry will benefit from the dynamics of Moore’s Law. Not only does it boost capability (and with it, VR appeal), but it lowers prices. Those price drops are already showing momentum. Plotted forward, we see headset average pricing drop to $282 by 2022.

All of the above will play out over the next few years, and we’ll course correct our projections as the market validates or disproves assumptions. It will be an important time for VR, as the health of the industry and the domino-effect of content investment start with the hardware installed base.

The good news: once 100 million units is reached, 200 million comes a lot faster. That’s because incentivized developers and supporting technology will flow in and create more content, which attracts consumers. That in turn attracts more content and developers, and around we go.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.