“Behind the Numbers” is AR Insider’s series that examines strategic takeaways from ARtillery Intelligence original data. Each post drills down on one topic or chart. Subscribe for access to the full library and other knowledge-building resources.

Many of us agree that XR will be transformative to life and business. But it’s a matter of when and how much. So ARtillry Intelligence ventured to quantify the revenue outlook in more precise terms. The result is our latest bi-annual XR revenue forecast, which tracks XR and its sub-sectors.

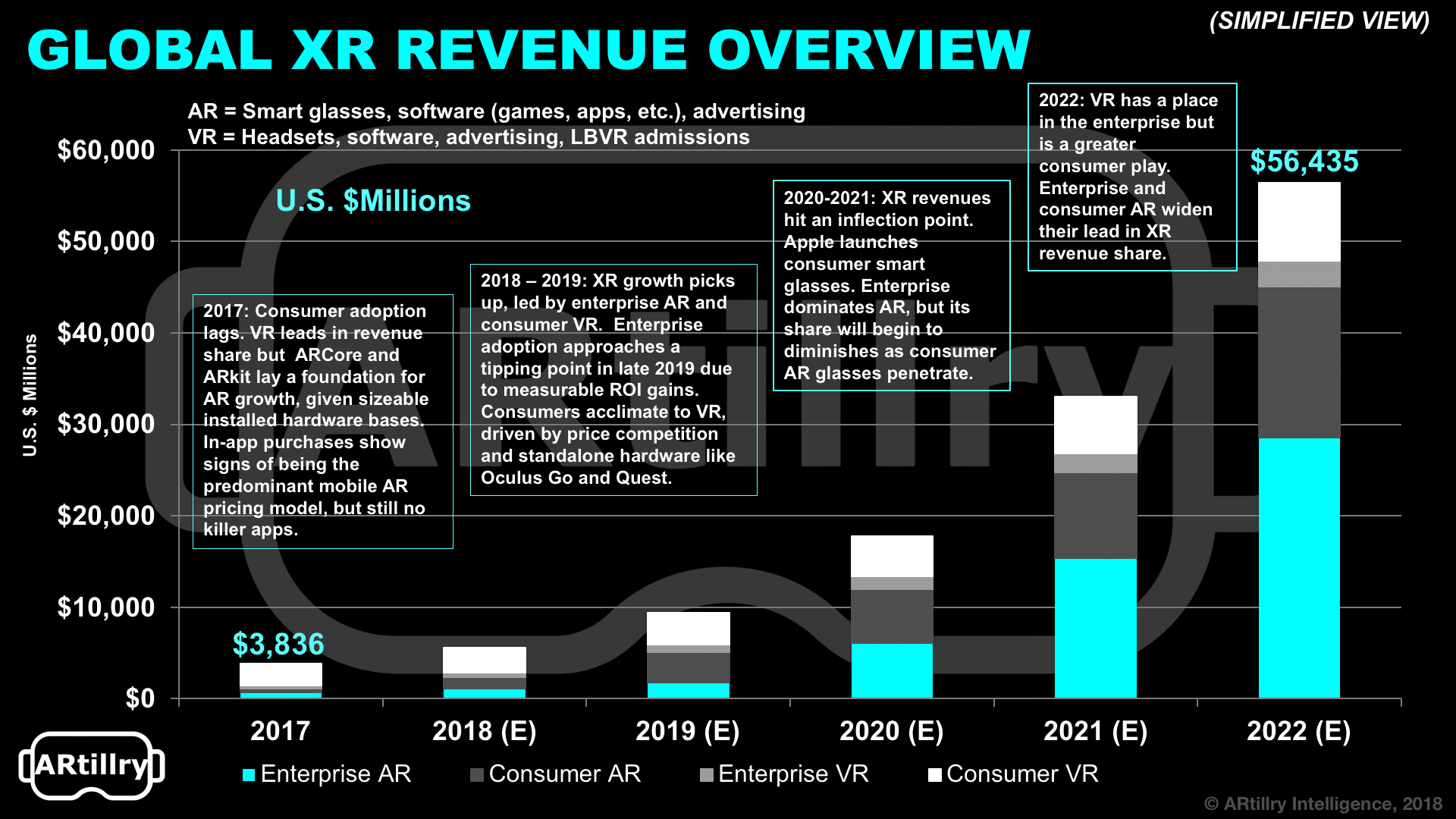

The high-level summary is that total global XR revenues will grow from $3.8 billion in 2017 to $56 billion in 2022. That includes AR, VR, and the enterprise and consumer segments of each. Those are then subdivided into revenue categories like hardware, software and advertising.

AR at Work

So where’s that money going? The largest sub-sector in outer years is enterprise AR, which will comprise roughly 51 percent of XR revenues by 2022. That has a lot to do with the scale achieved through wide applicability across enterprise verticals; and a form factor that supports all-day use.

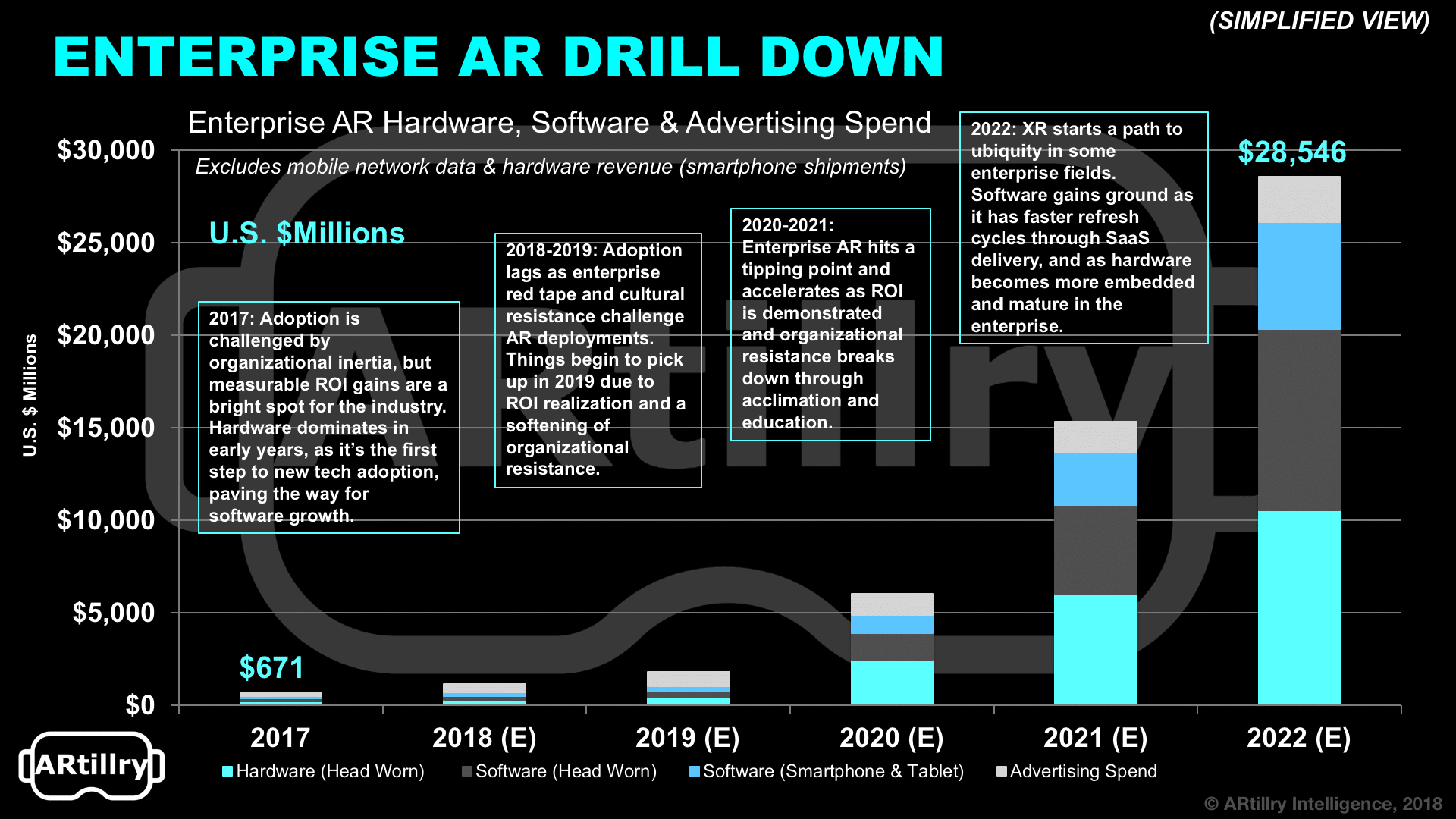

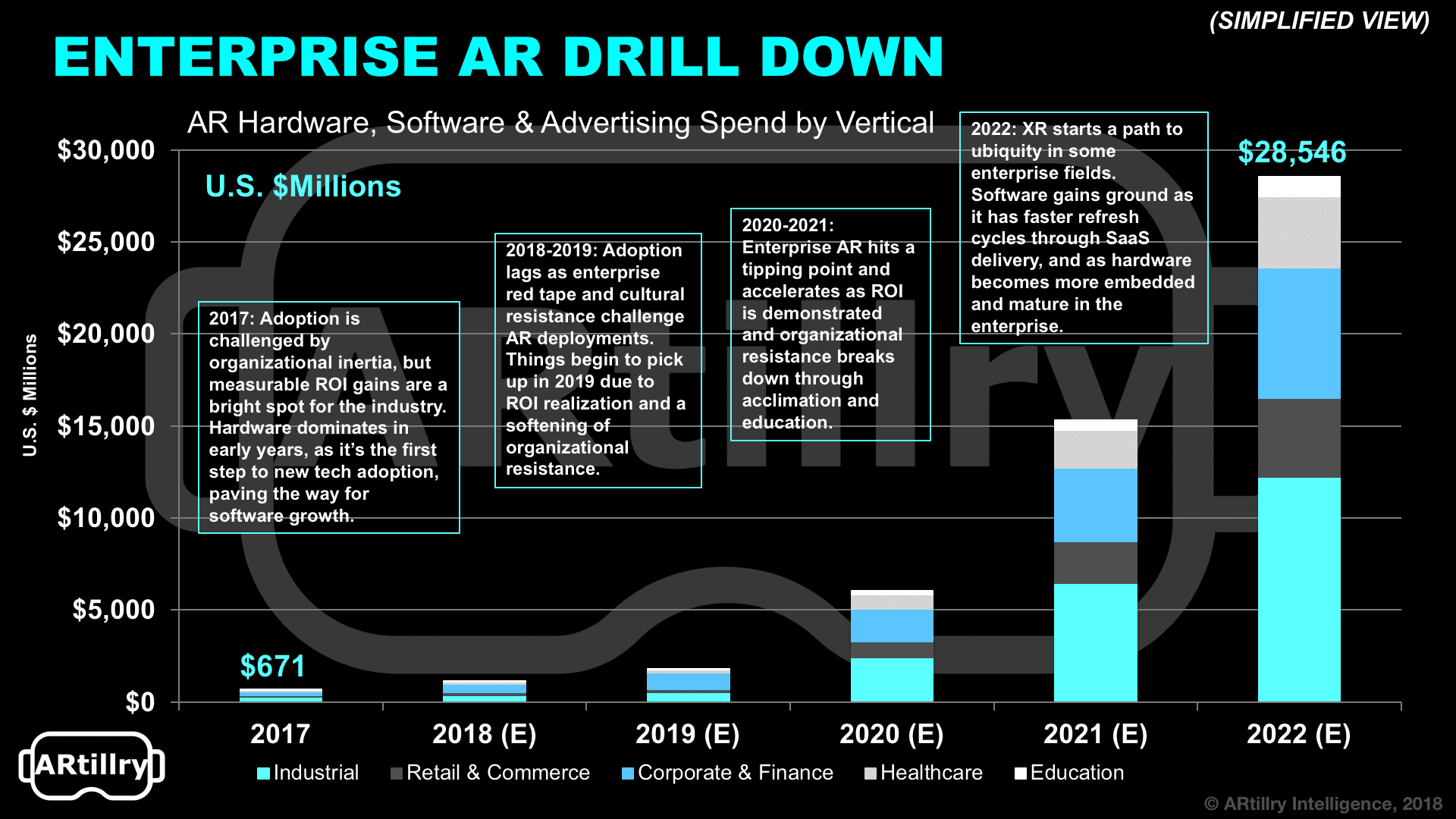

Specifically, enterprise AR will grow from $671 million in 2017 to $28.5 billion in 2022, a 113 percent compound annual growth rate. This makes it the largest XR sub-sector in 2022. To get to that point, it will build slow then happen fast as we approach a tipping point around 2020.

Adoption is currently dampened by typical organizational inertia, enterprise risk aversion and sales cycles. ARtillry Intelligence believes these factors will continue to stunt enterprise AR growth but will be outweighed eventually by momentum, support and ROI realizations currently building.

Tipping Point

The 2020 tipping point this all leads to will be followed by accelerated adoption in a sort of enterprise herd mentality. As a historical proxy, this slow then sudden adoption could follow a similar pattern as enterprise smartphone adoption over the past decade, but on a smaller scale.

As for the composition of revenue, it will be hardware-dominant in the near term as it’s the first step in enterprise tech adoption. But software will gain share over time. As usual, hardware growth creates an installed base for software, which will then gain revenue share in outer years.

The other reason software outpaces hardware is differences in their replacement cycles. Enterprise hardware will mature as it’s established in the enterprise, while software refresh rates continue at a constant pace. Recurring revenue is further reinforced through Saas models.

Lastly, how do revenues break down by vertical? Industrial settings will lead the pack, followed by retail & commerce, corporate & finance, healthcare and education. These rankings hinge on the size of the addressable market, applicability, adoption impetus and spending power.

Most of the above relates to AR’s role in operational support, such as manufacturing. But it’s also worth noting the enterprise spend for AR advertising. There, we’re cautiously optimistic on near-term revenue impact. There are positive signs but also scale and ad inventory deficiencies.

This will all be a moving target and we’ll continue to size it up twice-per-year. Meanwhile, stay tuned for more data slices from this forecast, which we’ll unpack in the coming weeks. Preview more of the report here, including methodology and breakdowns of what’s included in the figures.

For deeper XR data and intelligence, join ARtillry PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.