This post is adapted from ARtillery Intelligence’s report, XR 2018 Lessons, 2019 Outlook. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

2018 was a reflective year for XR. After an exuberant 2016, followed by a corrective 2017, XR industries settled into a moderate pace. This includes reset expectations on the size and timing of AR & VR markets, as well as acceptance that aspirations will take longer to materialize.

But we saw deep-pocketed tech giants charge ahead with XR. With strong contention that XR represents the next computing shift, they’re investing in the future of their platforms by gaining early market share and technological edge. And they’re each attacking XR from different angles.

Despite XR market softness, it was these moves from tech giants that provided confidence in 2018 for the eventual market arrival. Indeed, there’s no bigger vote of confidence in a technology and a market than billions of dollars in long-term bets. We believe this will continue into 2019.

#5. Consumer VR Begins Slow Rebound

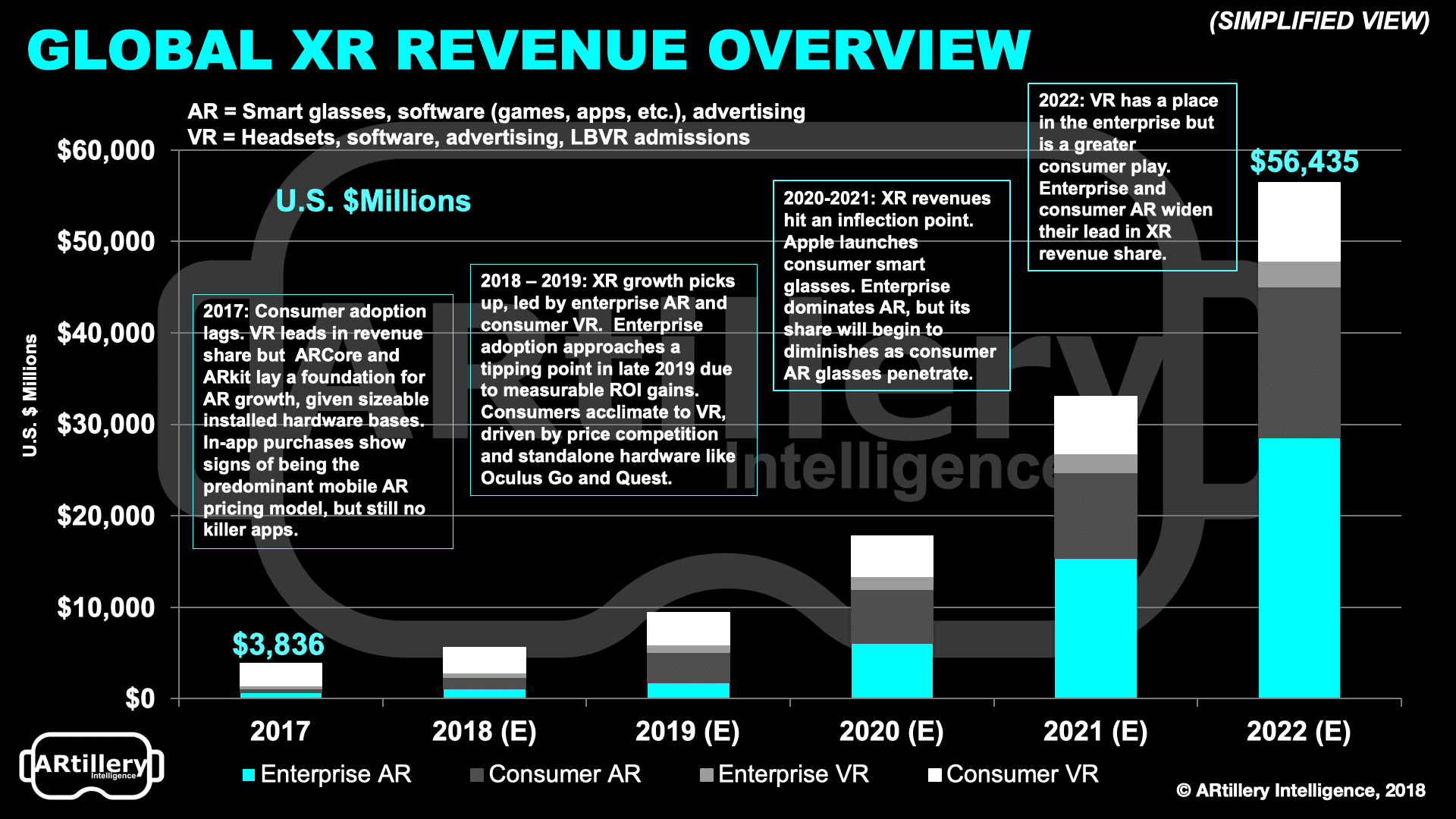

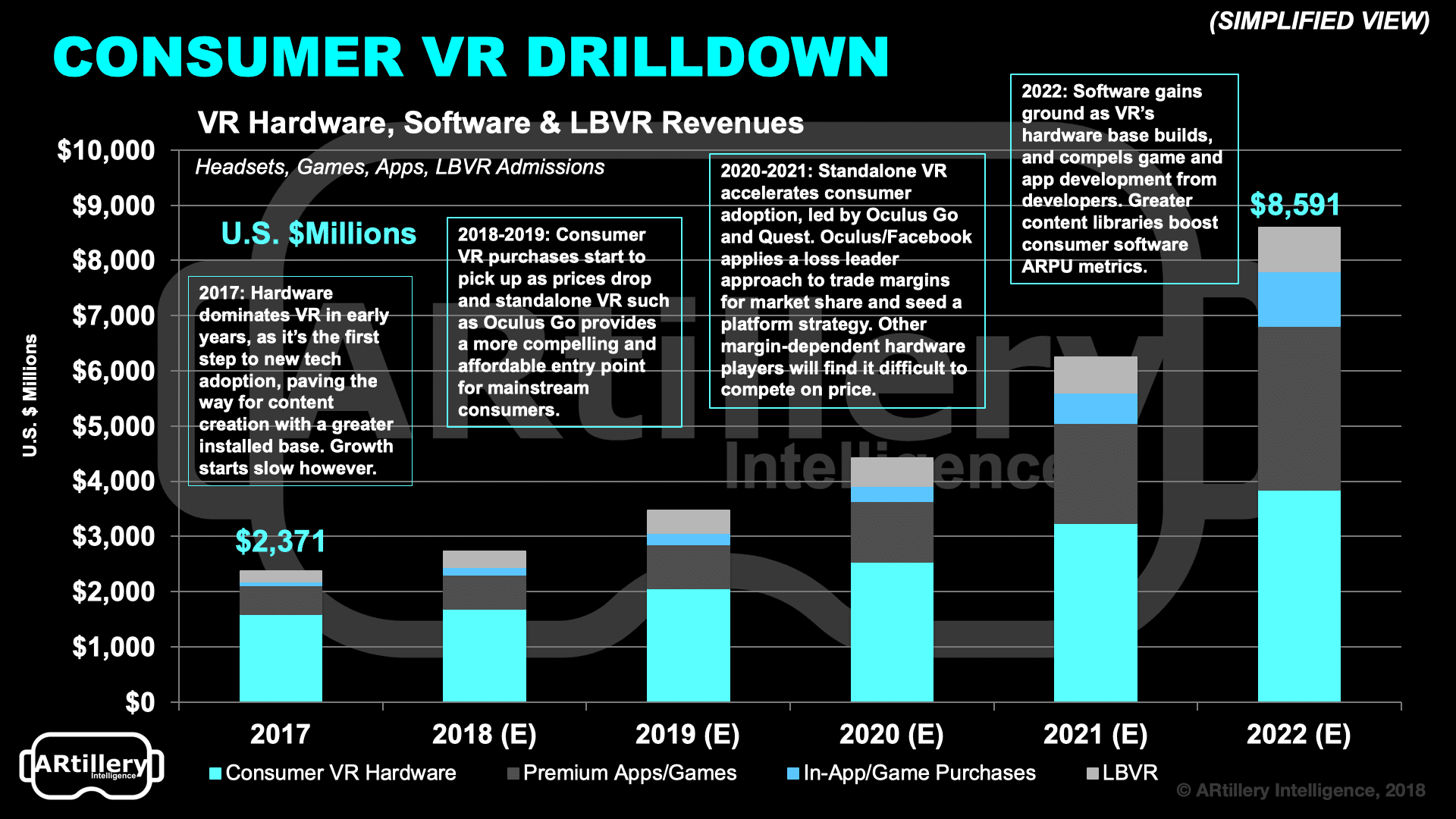

Picking up where we left off last week in drilling down on our specific 2018 lessons and 2019 predictions, consumer VR will be an XR subsegment that slowly rebounds after a tepid 2018. We project revenues to grow to about $3.5 billion next year and $8.6 billion by 2022.

Though it leads XR sub-sectors in revenue today – driven by gaming – VR revenues have flattened while other sectors trend upward. This is mostly due to revenue from early adopters who themselves plateaued in volume. With that realization, price competition took over in 2018.

That includes the $200 Oculus Go and the forthcoming $400 Oculus Quest. In fact, ARtillery Intelligence consumer survey data with Thrive Analytics (n=1959) indicate that demand inflects at $200 and $400. With an all-in price point, standalone VR will be the industry’s MVP in 2019.

Loss Leader

As background, Oculus’ Facebook backing enables aggressive pricing a la loss-leader approach to establish its platform. Early market share is the name of the game in platform wars as it attracts developers which grow the content library to in turn attract more users – a virtuous cycle.

But it’s not good for everyone. Partly due to Oculus’ pricing, margin-dependent hardware competitors have found it difficult to compete on price, and have begun to suffer or even abort VR projects. That means Oculus Quest (and Oculus Go’s holiday sales) will have a bigger impact.

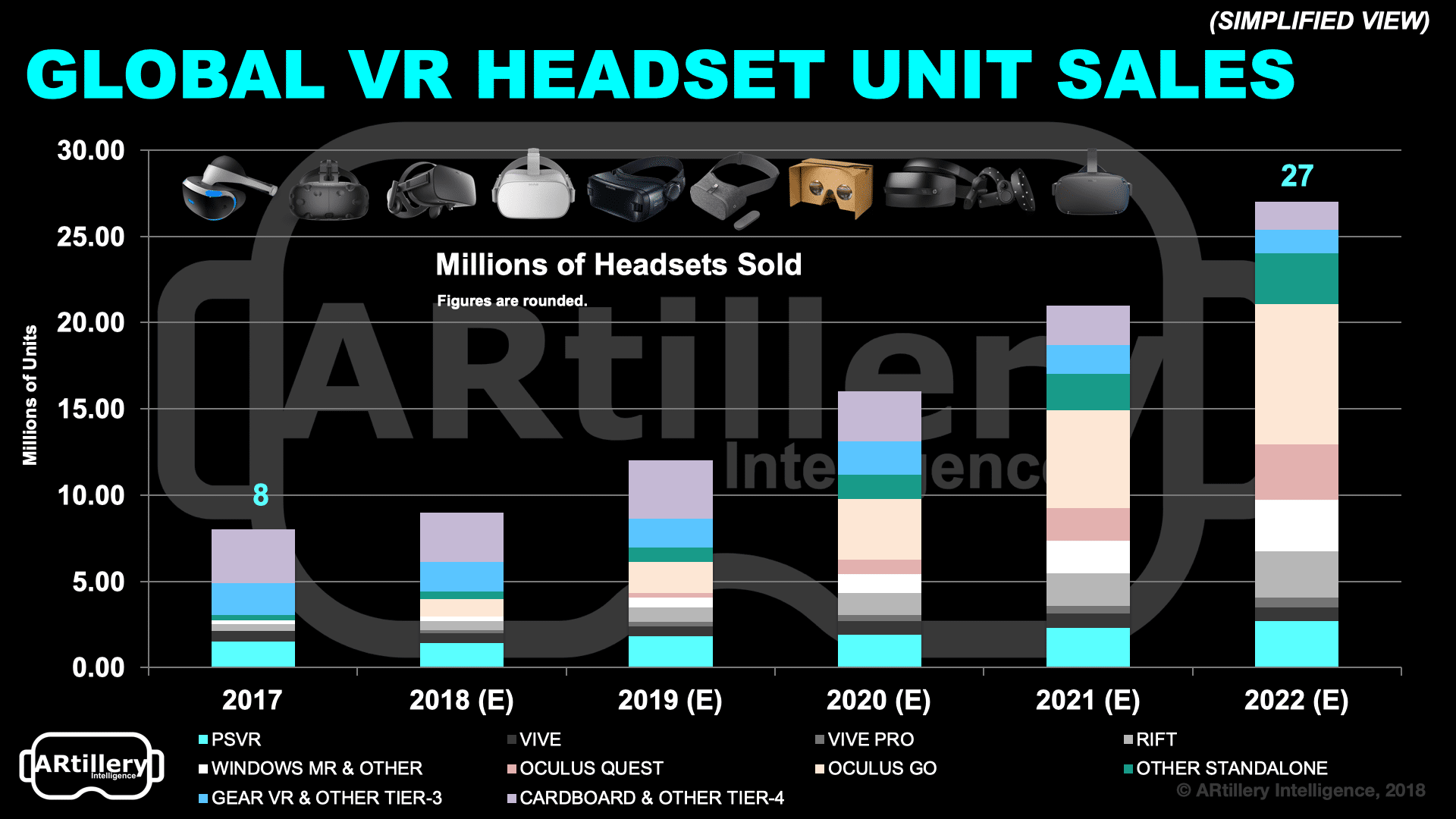

In terms of a concrete 2019 prediction, we’ll continue to see aggressive price competition from Oculus, which will benefit consumers, accelerate adoption and further contract the market . Oculus Go and Quest will pull ahead in ’19 and increase their lead of headset (unit) market share.

Magic Number

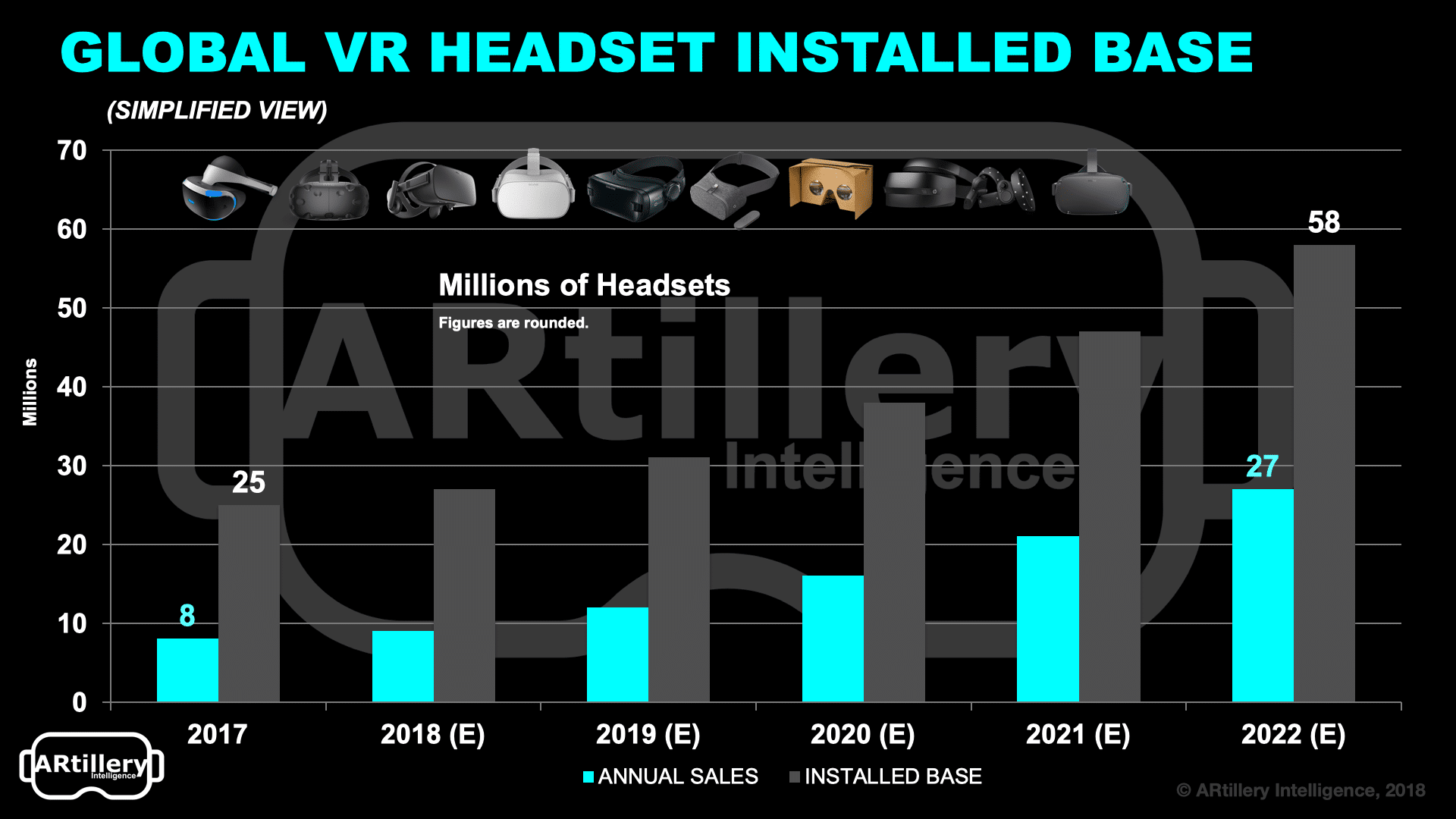

Oculus Go in particular will reach 2019 sales of 1.8 million, while Quest, launching mid-year, will reach a quarter of a million in annual unit sales. The overall headset installed base (cumulative units, not annual sales) will reach 31 million in 2019, on its way to 58 million by 2022.

This will be steady growth but won’t reach the “magic number” of 100 million units during this decade. 100 million is a historically validated milestone for hardware segments to reach a “flywheel” cycle of incentive for content creation, followed by accelerated consumer adoption.

The VR industry came to this sobering realization in 2018, and is well on its way to acceptance that VR won’t be the ubiquitous consumer product that was hoped and dreamed circa 2016. But that doesn’t mean that it can’t grow into an opportune segment of consumer entertainment.

For a deeper dive on 2108 lessons and 2019 predictions, see the full report.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.

Header image credit: Facebook/Oculus