This post is adapted from ARtillery Intelligence’s latest report, Industrial AR: Benefits & Barriers. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

In February 2018, we wrote a report that was part of the monthly flow of ARtillery Intelligence briefings. Entitled Enterprise AR: Impacting the Bottom Line, it defined how AR is being deployed in industrial enterprises like Coca Cola; and the operational efficiencies they accomplish.

Part of that report was also to examine some of the biggest challenges these companies face in implementing AR, including cultural and budgetary factors. We now revisit this analysis with 18 months of market analysis to draw upon. Many things have changed and some remain the same.

The high-level assessment is that all of industrial AR’s theoretical benefits still apply, and many are being demonstrated through real deployment (explored in this report). But some of the challenges we identified are even more pronounced today, while new organizational challenges loom.

The biggest phenomenon that’s accelerated over the past 18 months is “pilot purgatory.” As its name suggests, and as you may have heard in industry narratives, this is when AR is adopted at the pilot stage, but doesn’t progress from there. It’s the biggest pain point in industrial AR today.

Quantifying Industrial AR

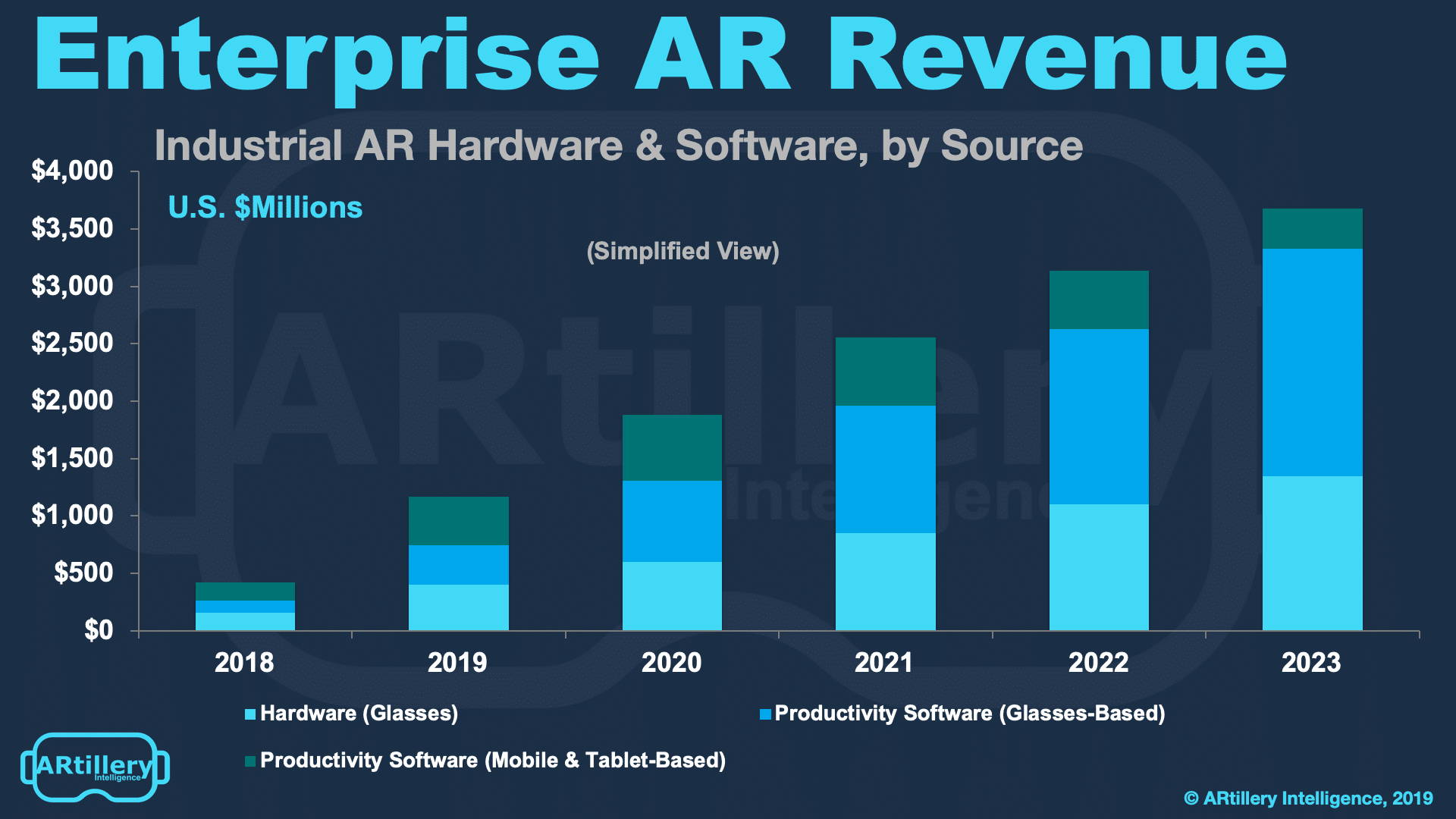

A bigger question is what’s the revenue opportunity for industrial AR? ARtillery Intelligence’s latest AR industry revenue forecast projects it to reach $3.7 billion by 2023. That includes revenue from AR hardware (smart glasses) and software to accomplish the functions we outlined last week.

In summary that includes an evolving suite of visualization tools to support assembly, maintenance and other industrial functions. It includes remote assistance for guiding front line workers with human support; pre-authored sequences that are more automated; and recording best practices.

We should also specify here that the common definition of “enterprise AR” is what we’re classifying here as “industrial AR.” Enterprise spending on AR is broader than industrial use cases (and measured separately), including brand advertising, retail and b2b software for AR creation.

Back to industrial AR, revenue is led by software for mobile devices, as it’s trusted hardware and lower hanging fruit. That’s followed by AR glasses, which represent industrial AR’s hardware base. Glasses-based software will pull ahead in outer-year spending, as it builds on that installed base.

Vertical Challenge

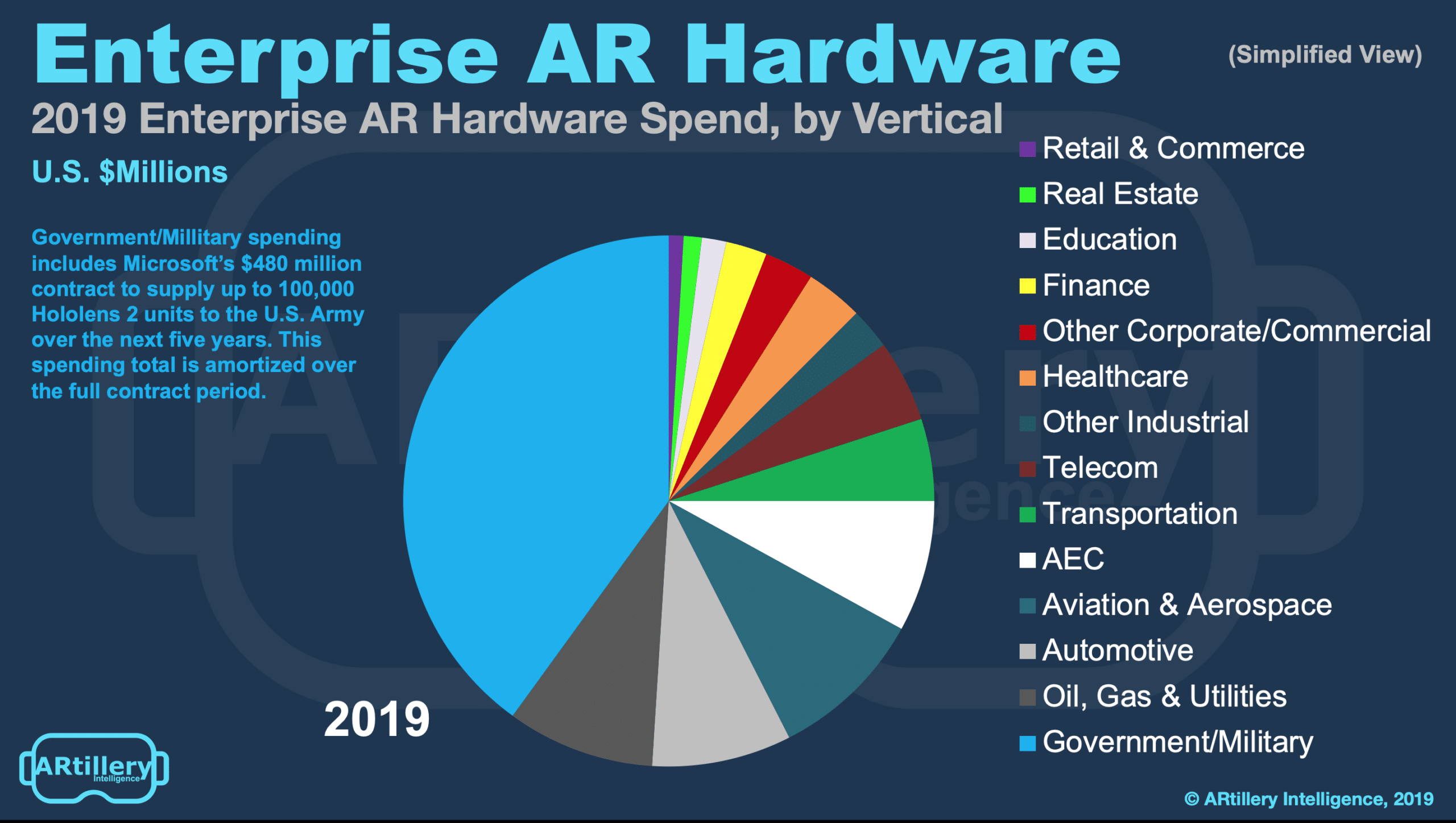

As for vertical segmentation, the largest source of spending is government and military. That’s mostly due to the U.S. Army’s $480 million contract to buy and deploy 100,000 HoloLens units over the next five years. This amount is amortized over the full contract period in this forecast.

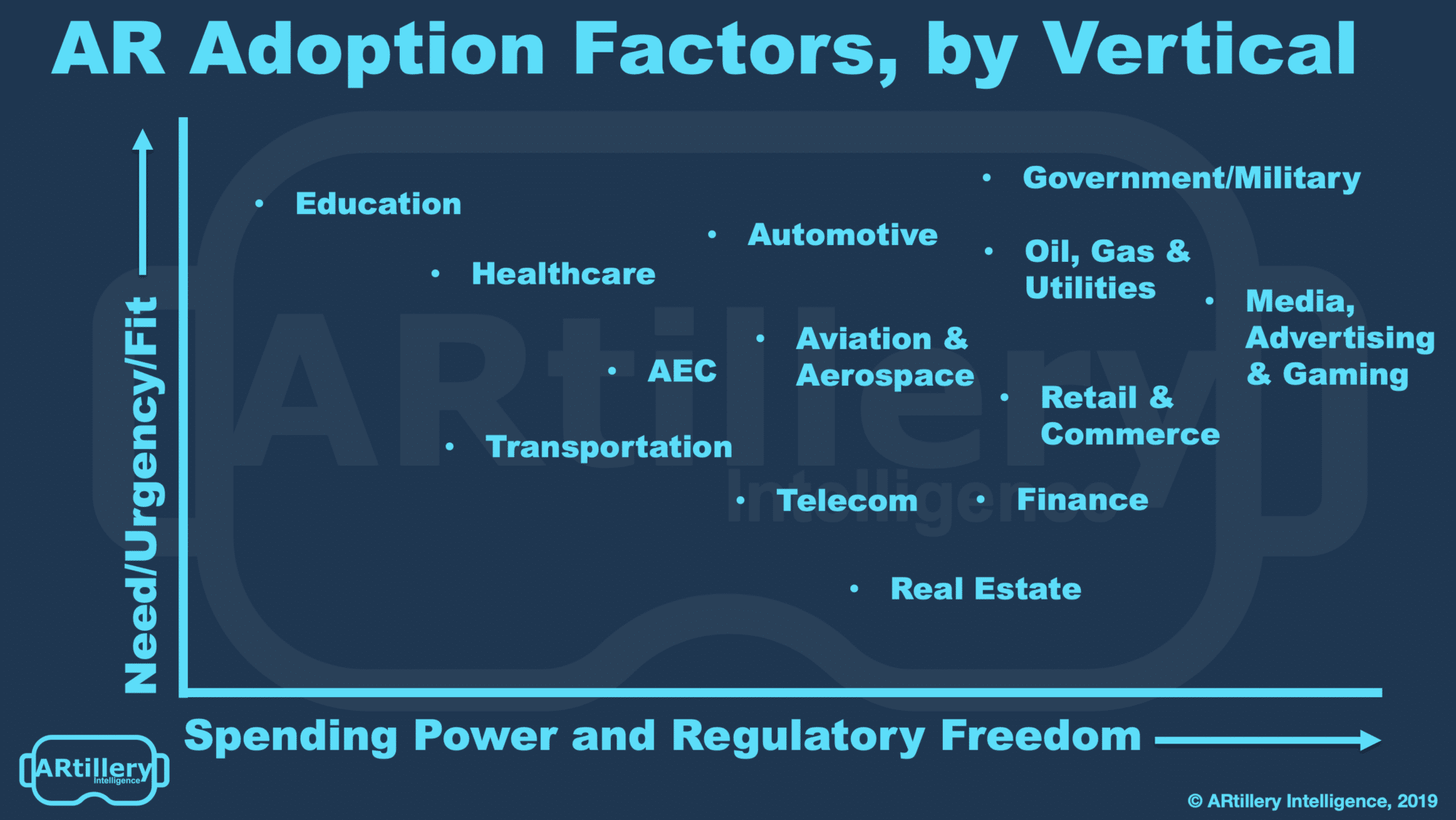

Other highly adoptive industrial verticals include oil, gas & utilities, automotive and aviation & aerospace. These verticals have a unique mix of criteria (see graphic below) that increase AR adaptiveness. We’ll expand this later in the report when examining AR targeting strategies.

Meanwhile, another key distinction in these figures is the degree to which they’ve been dialed back from previous ARtillery Intelligence projections (and other firms’ projections). This is due to the market’s slower than expected adoption and several other demand signals we track.

Just like enterprise smartphone adoption over the past decade, AR adoption will build up to a tipping point which is followed by accelerated adoption. We’re confident that will still happen, but it will be later than previously estimated due to the adoption inertia evident in today’s market.

See more details about this report or continue reading here.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.