Like many analyst firms, one of the ongoing practices of AR Insider’s research arm ARtillery Intelligence is market sizing. A few times per year, it goes into isolation and buries itself deep in financial modeling. The latest such exercise zeroes in on mobile AR revenues.

This takes the insights and observations accumulated throughout the year and synthesizes them into hard numbers for spatial computing (see methodology and inclusions/exclusions). It’s all about a strong forecast model and lots of rigor in assembling reliable inputs.

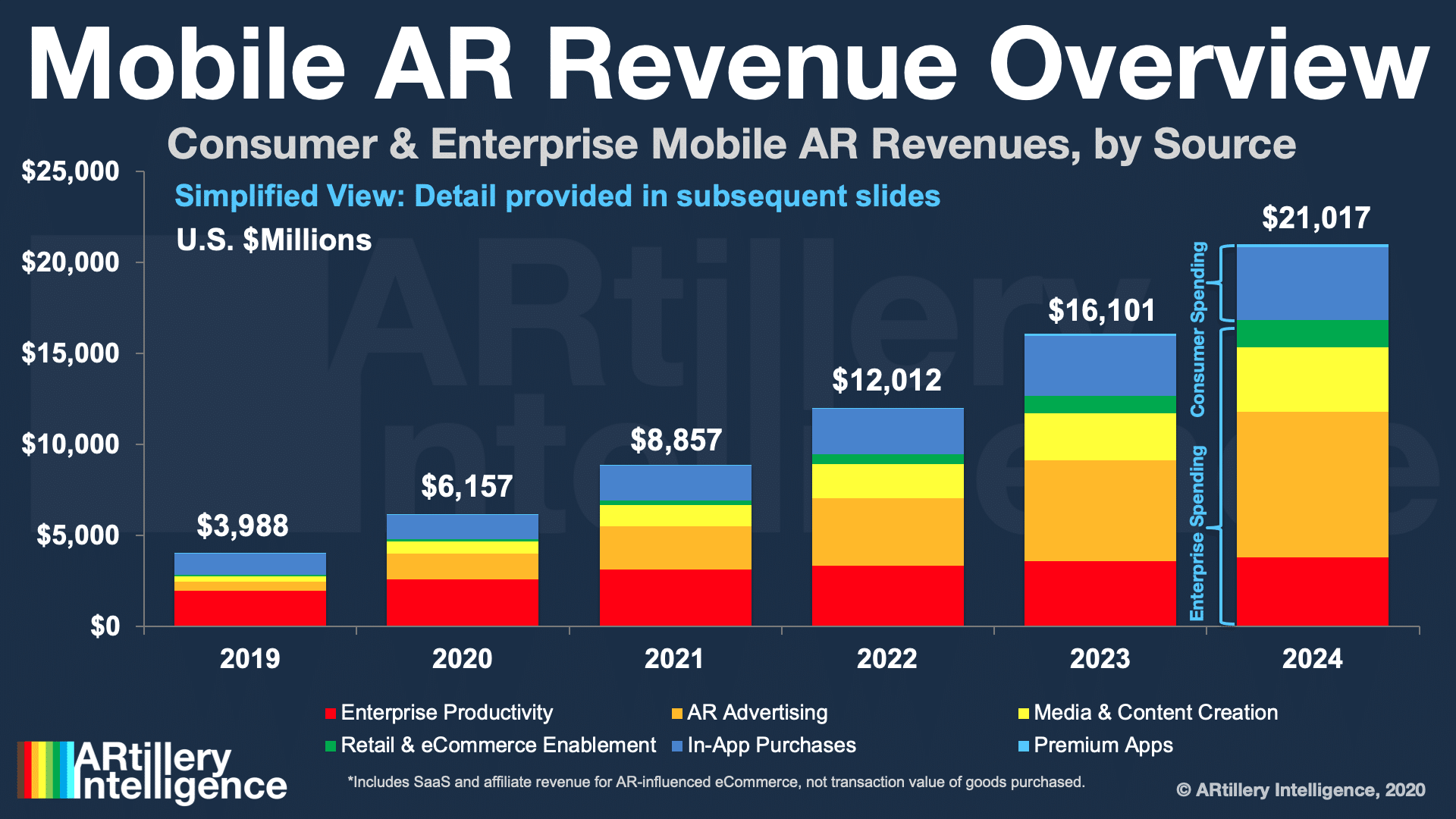

So what did the forecast uncover? At a high level, global mobile AR revenue is projected to grow from U.S. $3.98 billion in 2019 to U.S. $21 billion in 2024, a 39 percent CAGR. This sum consists of mobile AR consumer and enterprise spending and their revenue subsegments.

Obtain or Enhance

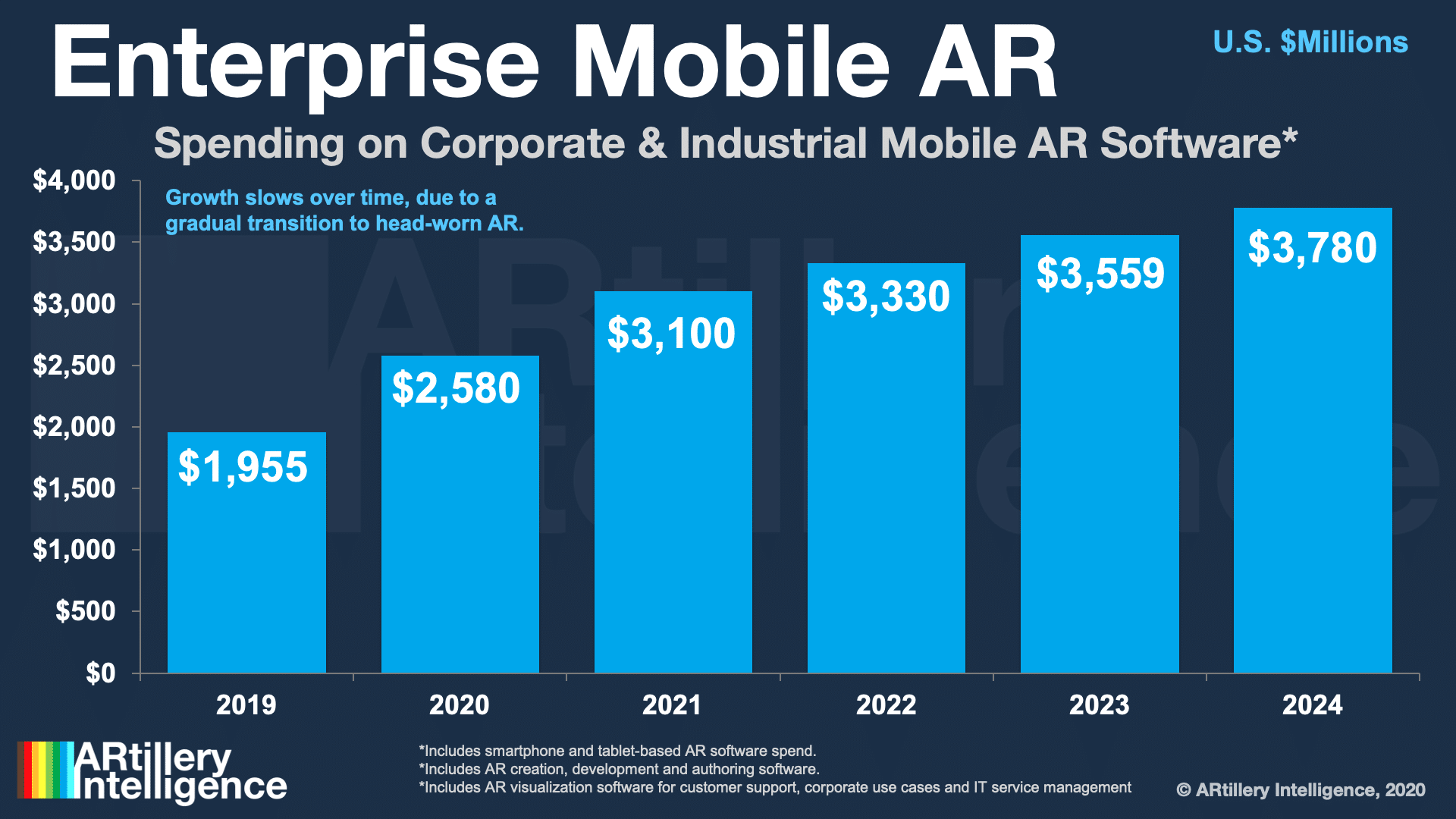

After our last Behind the Numbers segment tackled consumer mobile AR spending, what about its enterprise counterpart? We’re talking about enterprise spending on mobile AR software to gain productivity boosts or operational efficiencies through line-of-sight guidance and visualization.

Spending will grow from $1.95 billion in 2019 to $3.78 billion in 2024, a 14 percent compound annual growth rate (CAGR). This growth slows in later years as the field transitions to head-worn AR (note: these values apply only to smartphone-based AR. Head-worn AR is quantified here).

This spending includes visualization software that enables line-of-sight or live-guided support for assembly, maintenance or tech support. It also includes software that helps enterprises (or software vendors that serve them) author AR experiences that fit the same description.

This area’s strength and growth potential stems from its broad applicability. It can include everything from assembly to heavy-equipment maintenance to IT support. These functions cut across several industries and verticals, causing a sizeable addressable market.

Historical Patterns

Enterprise AR growth has so far been slowed by barriers like organizational inertia. For example, one of enterprise AR’s biggest pain points is the dreaded “pilot purgatory.” But AR continues to demonstrate a strong business case that will eventually overpower cultural resistance.

As this happens, adoption could follow a similar pattern (though on a lesser scale) as seen in enterprise smartphone adoption, including a tipping point that’s followed by accelerated adoption. But the timing of that tipping point will more likely benefit mobile AR’s successor, headworn AR.

Meanwhile, another adoption accelerant looms: Like many areas of mobile AR, Covid-era constraints compel enterprise AR productivity as remote AR supports social distancing. This will boost short-term traction while exposing the technology and accelerating its long-term adoption.

Stay tuned for more forecast tidbits and insights over the coming weeks. Meanwhile, find out more about the market-sizing methodology or access the entire report here. There will be lots to unpack as the mobile AR market unfolds and brings us expected and unexpected outcomes.

Header image credit: CareAR