Virtual reality continues to be challenged in gaining traction. Its world-changing potential that was trumpeted during the circa-2016 hype cycle didn’t pan out. But that doesn’t mean it’s dead. There are several bright spots and the sector continues to move forward at a moderate pace.

So to quantify the VR industry today and projected forward, ARtillery’s Intelligence’s latest revenue forecast does a deep dive on market sizing, growth drivers and strategic implications. It also breaks down findings in the latest episode of ARtillery Briefs (video and takeaways below).

Breaking it Down

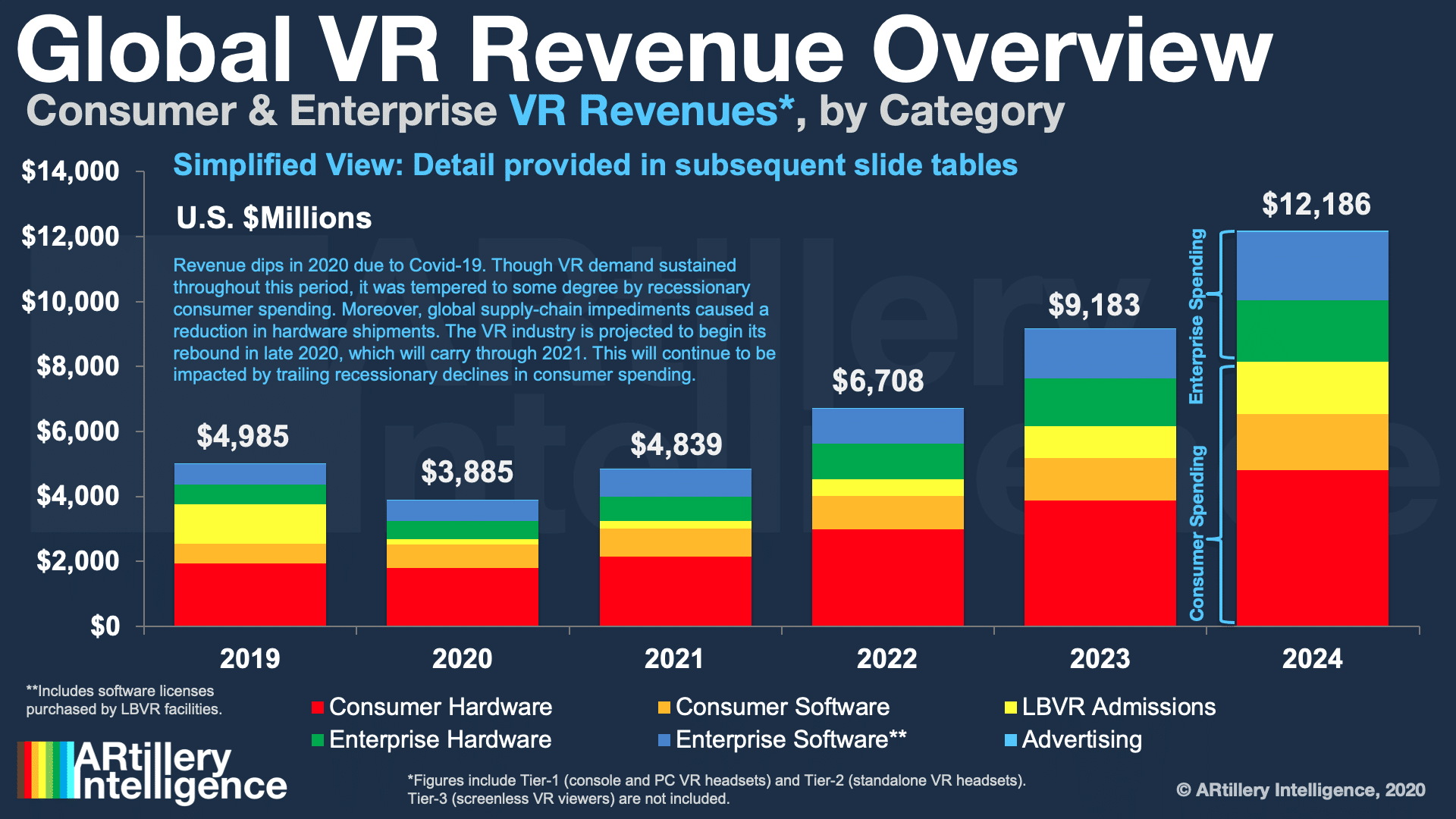

So what did the forecast uncover? Global VR revenue will grow from $4.98 billion in 2019 to $12.19 billion in 2024. This consists of consumer and enterprise spending, the former leading today due to gaming’s dominance as a VR use case. But enterprise VR is still finding a home.

Another way to subdivide these figures is hardware versus software. The former leads in spending share, as it often does in emerging tech sectors when an installed base is getting established. Over time, software spending catches up and builds on that base — a common pattern.

The biggest factor driving that hardware base today is Facebook’s VR investments, most notably the Q4-launched Oculus Quest 2. The device has a compelling spec sheet and overall experience, which is signaled so far in universal praise and several indicators of strong early sales.

Another key factor is pricing, as VR’s early and unproven stage means that it’s highly price-elastic. But Quest 2 carries a mainstream-friendly $299 price tag. This is notably one of the price points at which demand inflects according to our consumer survey data with Thrive Analytics.

This pricing results from Facebook’s VR long-game. It’s making little to no margin on Oculus Quest so that it can get the price down and get more people into VR. That’s a key step in its long-term goal of kickstarting a network effect. It’s classic loss-leader pricing.

Rising Tide

Beyond Oculus, we don’t want to discount other hardware, as there are notable players in the market. For one, PSVR remains the market share leader, and that has a lot to do with Sony’s installed base of more than 100 million consoles and a user-friendly price point.

We also see HTC continue to lean into the enterprise with Vive PRO, Cosmos, and Focus (and their many variants). There also continues to be movement with Windows Mixed Reality, most notably HP Reverb G2. Other independent standouts include Varjo XR-1 and Valve Index.

Altogether we project PC, console and standalone VR hardware unit sales to go from 5.4 million last year to 14.3 million in 2024. The latter correlates to a cumulative installed base of 34 million units. PSVR leads today, but Quest 2 and its future variants could soon take a market share lead.

Lastly, to address the elephant in the room, Covid-19 has impacted VR. The industry has seen some attrition, mostly due to supply chain impediments. But demand has grown over the past year as VR aligns with Covid-era demand signals like gaming, escapism and remote collaboration.

There was roughly a 10 percent dip in shipments in 2020, but VR will bounce back by late 2021. We’re already seeing positive signs as Facebook beefs up its supply chain to fulfill high demand. This positions it well as the world recovers and VR establishes its place in a post-Covid world.

See the full episode below and access the report here.