VR traction over the past few years has been slower than many had anticipated. But it’s still finding small wins and is growing at a fairly healthy pace. So the question is how well it’s landing with consumers today, and are those sentiments trending in the right direction?

So we set out for answers. Working closely with Thrive Analytics, ARtillery Intelligence authored questions to be fielded through its established survey engine to more than 98,000 U.S. adults. The result is Wave VI of the research, and a narrative report we published to unpack the results.

Known as VR Usage & Consumer Attitudes, Wave VI, it follows similar reports over the last few years. Five waves of research now bring new insights and trend data to light. And all five waves represent a collective six-digit sum of U.S. adults for robust longitudinal analysis.

Among the topics tackled: How is VR resonating with everyday consumers? How often are they using it? How satisfied are they? What types of experiences do they like most? How much are they willing to pay for it? And for those who aren’t interested in VR… why not?

Early Stages

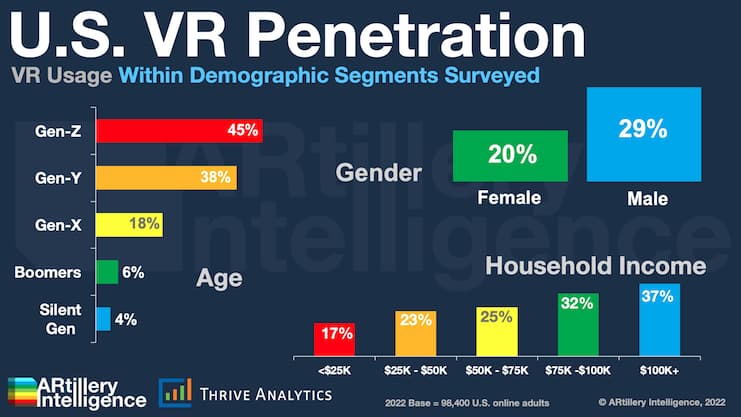

Diving into these questions and starting at the top, what’s VR’s overall penetration? This year’s survey pegs it at 23 percent of U.S. adults. It’s still in early stages of its industry lifecycle, and we expect usage to accelerate as consumer comfort levels – and the technology itself – advance.

As for who these users are, 29 percent of male respondents in the survey reported using VR versus 20 percent of female respondents. 45 percent of Gen-Z and 38 percent of Gen-Y (millennials), report VR usage, versus 18 percent of Gen-X and 6 percent of baby boomers.

This means there’s an inverse relationship between age and VR usage: Adoption goes up as age goes down. There’s also a correlation between VR usage and household income: they go up together. The largest income group for VR adoption (37 percent) is $100K+ in household income.

Another question is how VR’s penetration represented in these survey results translates to overall market size. Given that this is a U.S.-based survey, applying the above 23 percent figure to the U.S. adult population (329.5 million) indicates that roughly 75.8 million adults have tried VR.

To pause for definitions, these totals measure U.S. adults who have used VR at least once. This broad definition lets us start with a baseline, then drill down. For example, how do these overall usage figures break down by frequency? That’s always a key marker for consumer traction.

Name of the Game

Drilling down, most VR users engage weekly (31 percent) and daily (29 percent), followed by monthly (20 percent). This means that 80 percent of VR users engage monthly or more. This is a strong signal for VR engagement levels, compared to most other forms of consumer technology.

As for trending, daily use is down 3 points, while weekly and monthly use is flat. The dip in daily use could be due to the waning stages of the Covid era. In other words, a return to outdoor and IRL activity will naturally cause gaming and entertainment to decline to some degree.

Why is all this important? As noted, frequency is a key health indicator for consumer tech. In VR specifically, adoption barriers can be high (play area/boundary setup, dedicated time for immersive media, etc.). So the name of the game is ease of use and replayability.

This challenge is being addressed with the continued growth of standalone headsets like Meta Quest 2 and Pico 4. Given their ease of use and growing penetration, these frequency metrics could improve. Meanwhile, VR frequency already shows positive momentum in this survey.

We’ll pause there and pick things up in the next installment of this series, including other variables in consumers’ VR usage. What headsets are they using? What are the most popular use cases? How satisfied are they with VR? And how much are they willing to pay for it?