Though spatial computing and all its subsegments continue to hold great potential, they also face headwinds. Factors holding them back include challenged technological advancement and cultural adoption. However, bright spots include the rise of AI- powered smart glasses.

For example, as seen in Meta’s earnings, smart glasses have offset declines in other subsegments, such as consumer VR. Altogether, it’s a mixed story with both positive and negative drivers. The good news is that the positives will mostly outweigh the negatives in the near term.

To wrap some numbers around these claims, spatial revenue is projected to grow from $28.5 billion in 2025 to $61.4 billion in 2030. That’s steep growth, driven by a projected inflection next year as new smart glasses blitz the market from Apple, Meta, Google (AndroidXR), and others.

What else is driving spatial revenues, and what are strategic implications? These questions are tackled in the latest spatial revenue forecast from our research arm, ARtillery Intelligence. This Behind the Numbers series excerpts those insights, continuing below with top-level findings.

Growth Engine

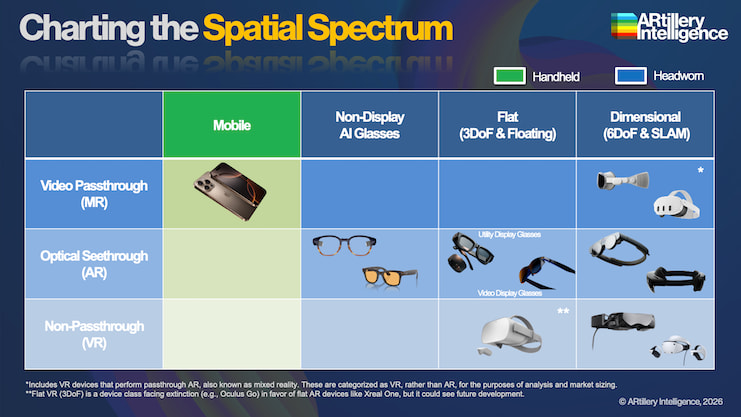

Starting at the top, spatial revenue is projected to grow from $28.5 billion in 2025 to $61.4 billion in 2030, a 16.5 percent compound annual growth rate. By segment, VR leads with $14.02 billion in 2025, followed by mobile AR ($9.02 billion) and headworn AR ($5.47 billion).

But that’s just a snapshot of today. These segments will shift in share, ending in 2030 with headworn AR in the lead, followed by VR, and Mobile AR. Put another way, VR still leads in sheer dollars, however momentum is clearly on the side of AI-powered smart glasses.

When zeroing in on VR, it has faced some declines in consumer markets. Enterprise VR has meanwhile grown, albeit gradually, largely on the strength of immersive training and its ability to breed operational efficiencies and executional efficacy. This is currently VR’s growth engine.

Meanwhile, mobile AR has traditionally scaled by piggybacking on an existing installed base of 3 billion+ global smartphones. But that usage hasn’t always translated to revenue, as consumer mobile AR revenue has underperformed, relative to the medium’s traction.

In fact, most mobile AR revenue is paid for by enterprises (B2B2C), such as immersive brand marketing. Put another way, most consumer mobile AR is brand-sponsored rather than user-purchased. The latter has some bright spots, such as Snap’s Lens+ subscription.

Underwhelming to Utilitarian

On to headworn AR, there continues to be ample anticipation for full-featured dimensional AR glasses. But these bring technological and practical challenges. Barriers include cost, bulk, and cultural resistance. Snap is hoping to crack this code with its consumer Specs this year.

Otherwise, these dimensional-AR challenges drive ‘lighter’ approaches. Though flat AR is inferior to dimensional AR in its visual UX, it can still be valuable due to utilities such as messaging, and POV viewfinders. These are experientially meaningful, even if graphically underwhelming.

The key here is that one factor has unlocked such utilities: AI. Contextual intelligence brings flat AR from underwhelming to utilitarian. This includes flat AR display glasses like Meta Ray-Ban Display Glasses (MRD), as well as non-display glasses like Ray-Ban Meta Smartglasses (RMS).

Zeroing in on the latter, the toned-down UX noted above is taken to another level by sidestepping visuals altogether. Moreover, this tradeoff of utility and style for visuals has been validated. The market has spoken… to the tune of 10 million+ lifetime units sold for RMS.

Sales momentum is also strong, while other players have begun to chase these market-validated demand signals. These include the emerging Android XR ecosystem, which could do for XR – across device classes – what Android did for the mobile ecosystem 15 years ago.

We’ll pause there and circle back in the next Behind the Numbers installment with more numbers & narratives. Meanwhile, check out the full report.