Just like Apple’s June ARkit launch, Google’s recent ARCore unveiling has bred lots of interest its addressable market. And just like with ARkit, we’ve applied best practices in market sizing and forecasting to pinpoint that figure.

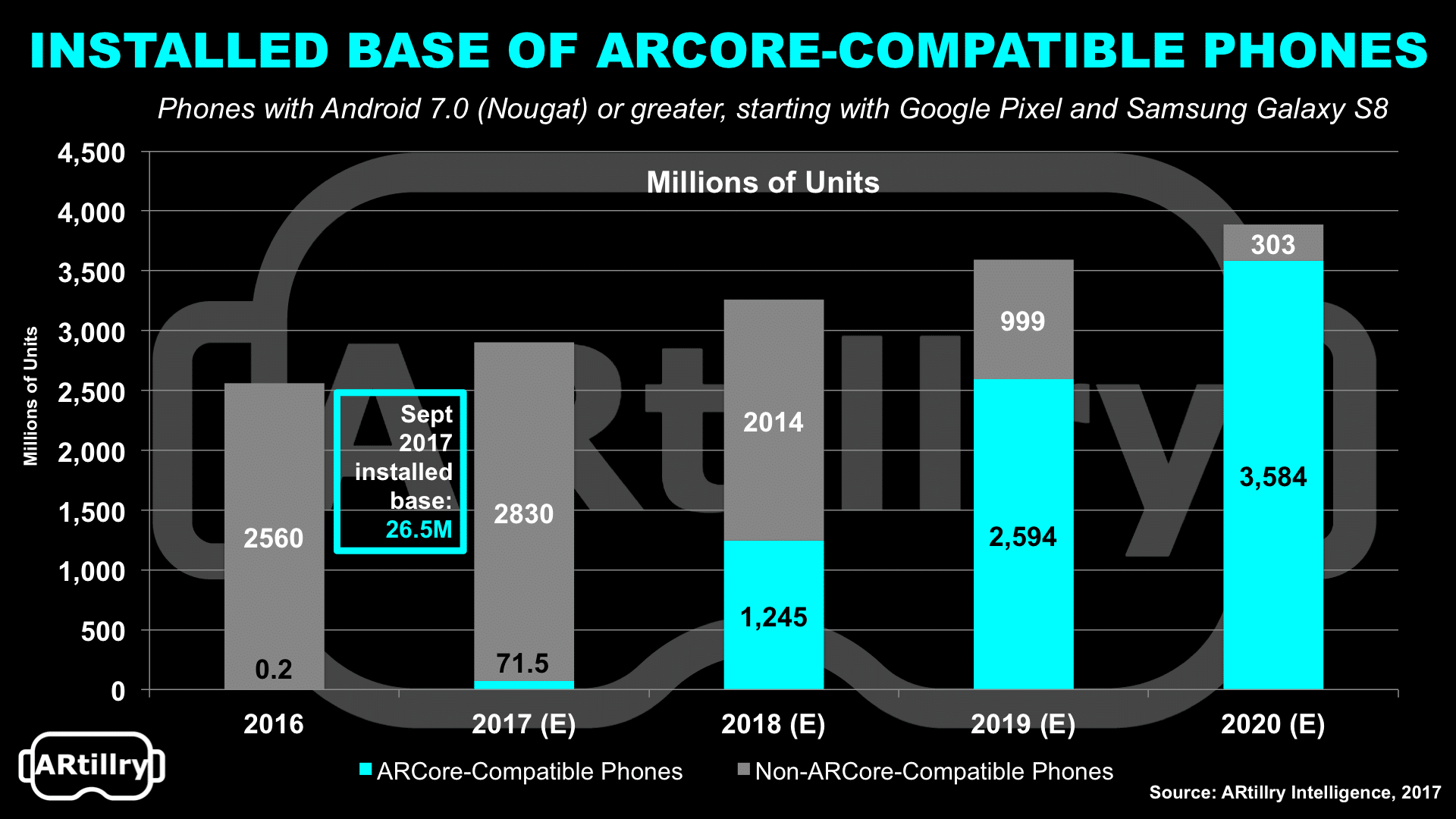

The verdict: There are 26.5 million ARCore-compatible phones today, growing to 71.5 million by the end of 2017. Based on the size of the Android universe, this will quickly accelerate over the next few years, reaching 3.6 billion units (92 percent Android coverage) by 2020.

How did we arrive on these figures? The starting point is ARCore’s current compatibility, limited to Google Pixel and Samsung Galaxy S8, running Android 7.0 (Nougat) or greater. Looking at cumulative sales figures for both devices, we’re at roughly 26.5 million total units in market.

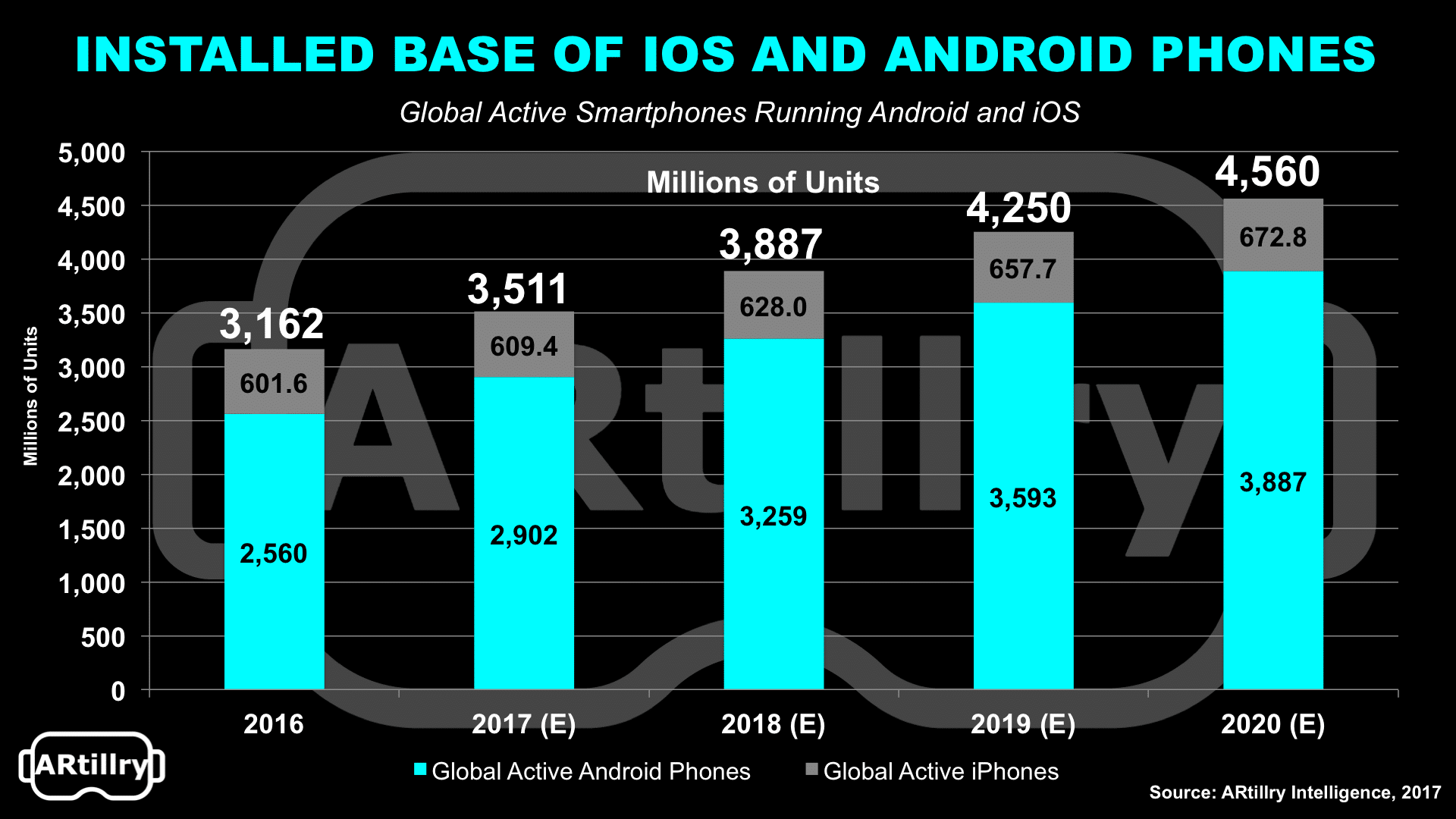

But that’s the easy part. The hard part is projecting forward. Based largely on the size of the overall Android installed base — 2.9 billion global devices today, growing to 3.8 billion by 2020 — number crunching ensued. One key forecast input is upgrade cycles in the Android Universe.

About 16 percent of Android devices usually run OS versions released in the prior year, while 32 percent run versions older than one year, 29 percent older than two years, 15 percent older than three years, and 8 percent older than four years (hence ARCore’s lack of full coverage in 2020).

There was also a major hint from Google: The company noted in ARCore’ introduction that it’s working towards a goal of 100 million compatible phones — including Huawei, Asus and LG — when the platform launches. It didn’t provide a date but we’re predicting Q1 2018.

Stepping back, one takeaway is that ARkit has a slight advantage in being first to market with a head start in developers’ invested time. But the lifespan of AR will eventually diminish Apple’s three-month head start. Greater developer attraction will ultimately come from platform reach.

Apple also has a near-term lead in the installed base of ARkit-compatible iPhones (380M), but one hardware replacement cycle (2.5 years) will give most smartphones AR-compatible optics and processing. And the Android universe exceeds iOS, by more than two billion units.

Other points of differentiation come down each platform’s approach for delivering AR. Apple’s DNA is an app based framework, while Google’s web-based DNA will be reflected in its use of Web AR. The latter could have less friction (in addition to more scale), as we’ve examined.

There is of course a lot more to these competitive dynamics and addressable market sizes, and we’re in the process of dissecting them for ARtillry’s September Intelligence Briefing. It will take a deeper dive on ARCore and ARkit, and the strategic implications for everyone. Stay tuned.

See our market-sizing and forecasting credentials here.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.