Mobile AR hit an inflection point in 2017. It started with Facebook’s Camera Effects Platform in April, followed by Google’s “visual search” and “VPS.” Then in June we saw Apple’s ARkit, followed by Google’s August ARCore launch.

Those last two are perhaps most impactful because of the tools they create for developers to build more advanced AR. Mobile AR can really scale when it’s in the hands of developers, and when they’re incentivized by an installed base in the hundreds of millions of devices.

We’ve recently quantified that installed base (ARCore & ARkit), but decided to take it one step further. ARtillry’s latest Intelligence Briefing takes a deeper dive on ARCore and ARkit. How do they differ? What does it mean for consumers? AR developers? What happens next?

Executive Summary

Over the past six months, the tech sector has reined in its initial excitement about glasses-based augmented reality (AR). This includes realigned expectations on the time horizon to consumer ubiquity. But in the meantime, the AR world is keeping busy with another opportunity: mobile AR.

Beyond specs (battery life, field of view, etc.), AR glasses’ detriment is form factor: It needs to be sleek and cheap enough to sway consumers to reconcile a key point of friction: personal style. The bar is set high for anything people are asked to put on their face, as Google Glass taught us.

This concern goes away in enterprise contexts (the topic of another report) but is a sizeable barrier in consumer markets. And we’re a few years from marketable formats. The good news is that the stepping stone — or gateway drug as we like to call it — is mobile AR. And there’s a lot happening.

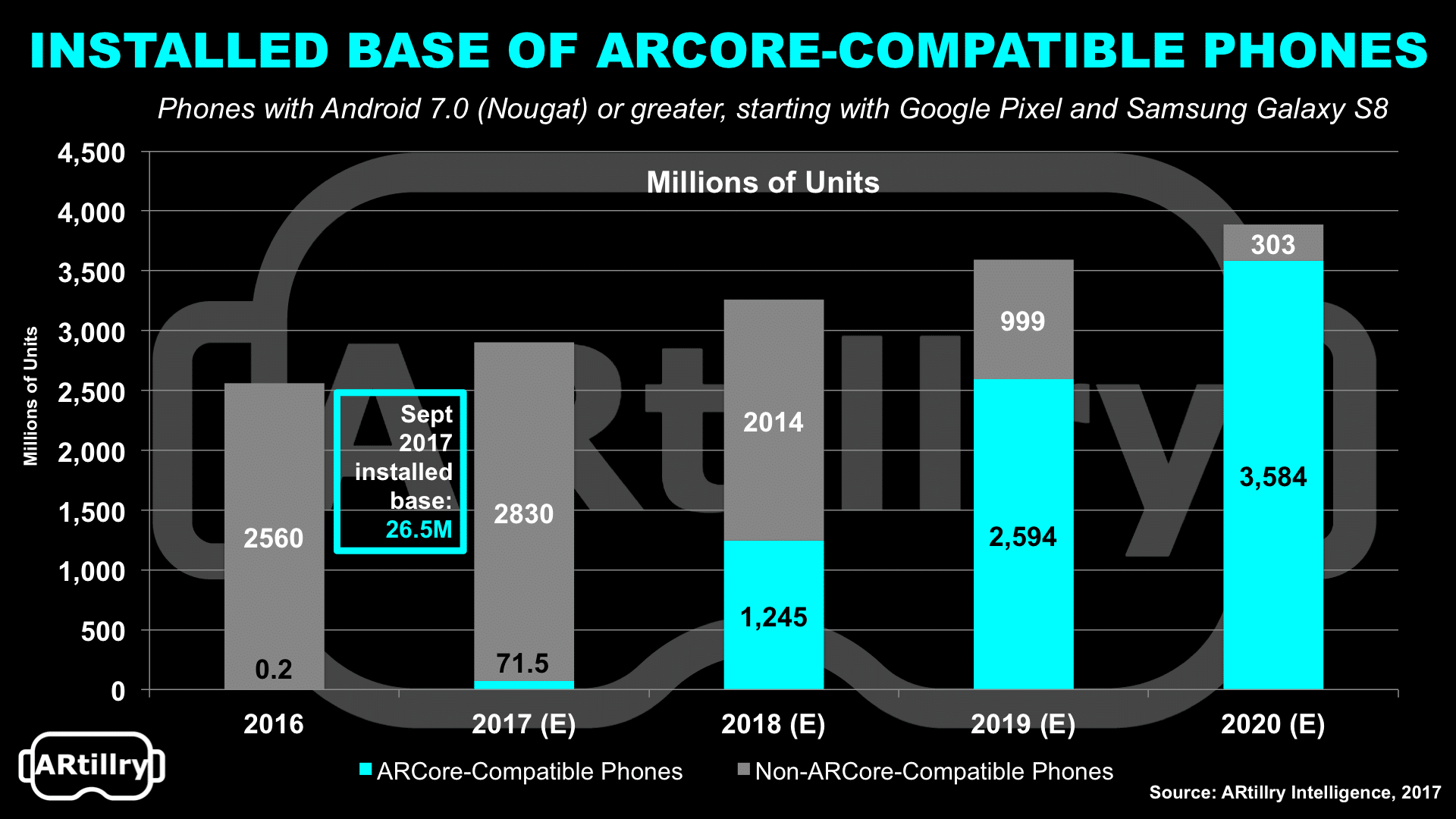

Going by the numbers, mobile AR’s addressable market isn’t the low-millions of headsets: it’s the 3.2 billion global smartphones today and 4.6 billion by 2020. Those aren’t all AR compatible in terms of optical and processing components, but most will be over the next replacement cycle (2.5 years).

Google’s AR development kit ARCore will become compatible with 3.6 billion global android devices during this time frame, and Apple’s ARkit will reach 673 million iPhones. Both achieve AR through software, utilizing the standard smartphone RGB camera, thus lowering the barrier to “true AR.”

Compared to graphics that simply overlay a scene, true AR infuses graphics that interact with physical objects in dimensionally accurate ways. ARCore and ARKit apply simultaneous localization and mapping (SLAM) through a surface detection approach that doesn’t require advanced optics.

The result is an overall democratization of advanced AR capability. This starts with the massive installed base mentioned above, which in turn incentivizes developers with a larger addressable market. Then the content they create entices more users to engage, enacting a virtuous cycle.

Looking forward, we can expect several AR apps as ARCore and ARKit gain footing. But more impactful will be years of third-party innovation with both SDKs. That could rival in creativity and advancement, the app economy itself, which kicked-off ten years ago with the first iOS SDK.

But several questions remain: How quickly will this happen? What are the pros and cons of each AR toolkit? What will be best practices in building, distributing and marketing AR apps? And what does it all mean from where you sit? These questions are tackled throughout this report.

See our market-sizing and forecasting credentials here.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.