This post is an excerpt from the ARtillry Intelligence Briefing, Smart Money: Insights from AR & VR Investors. It pulls from the section of the report that examines areas where nearer term opportunity and scale exist… namely mobile and enterprise.

Size Matters

In addition to focusing on the enabling technology needs of today, AR and VR investing is about gauging the market size of tomorrow. Key investment metrics often involve unit economics, recurring revenue, acquisition cost, customer lifetime value, and total addressable market (TAM).

The latter is a particularly important metric in AR and VR because it’s a function of hardware sales. And with consumer VR especially, hardware sales (headsets) have been slower than expected. The industry’s excitement levels – though recently cooling – haven’t been proportionate to sales levels.

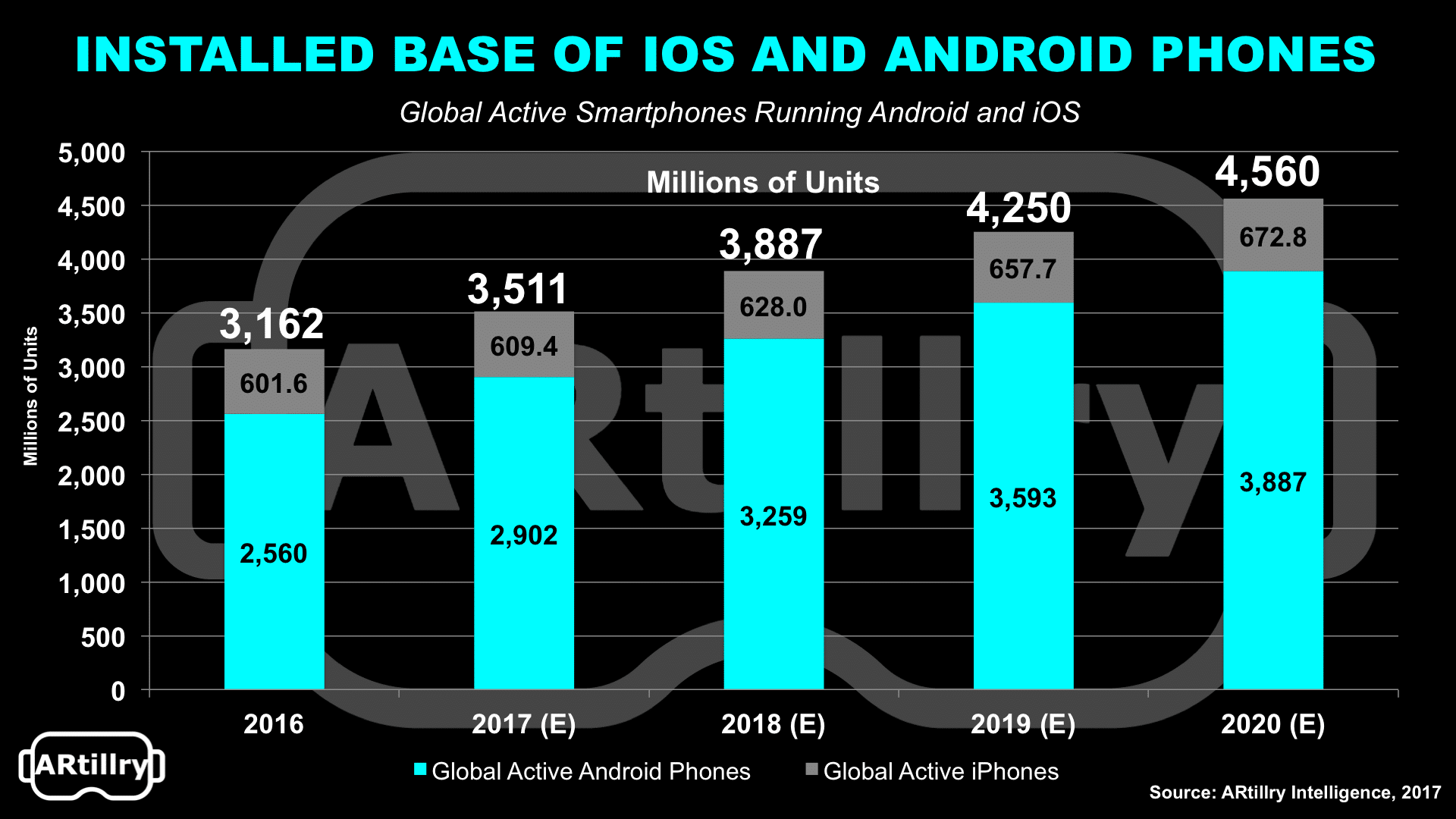

Specifically, ARtillry has done the math, indicating that there are roughly 17 million headsets sold so far globally at all device tiers. To put that into perspective, the current predominant consumer tech product – smartphones – have reached a global installed base of roughly 3.2 billion units.

This indicates that VR headsets have a long way to go. ARtillry believes the magic number is 100 million units. That’s the size of the installed base that will be a key milestone and turning point for VR. It’s the number that attracts content creators and supporting functions, and engenders network effect.

This is precisely what we saw with smartphones. Once 100 million units were sold globally, the mobile industry accelerated and could support an app economy and several other moving parts. This is due to the larger incentive for content creators and supporting tech vendors to enter.

This happens through a sort of snowball effect. The gravitational pull of 100 million units attracts new entrants who accelerate the industry’s advancement and output. That further boosts unit sales, which in turn attracts more entrants. So the march to 200 million or 2 billion happens at a faster pace.

The lesson is that until high-end consumer VR reaches that point of ubiquity, there are other points along the immersive computing spectrum that represent nearer-term scale and opportunity. These most notably include mobile AR and VR (building on an existing installed base) and enterprise.

The Mobile Base

Mobile is especially opportune because its installed base already sits at 3.2 billion units — roughly half the population of the earth. Though it doesn’t represent the fully-realized vision of VR, it’s good enough for a minimum viable product, given ubiquity, baseline processing and graphical capacity.

“VR rides on the mobile ecosystem for hardware, compute processing and app store dynamics,” said Comcast Ventures’ Yang. Across Realities’ Lukas agrees: “When we first saw Oculus Rift, we identified that the future of computing is AR and VR, and the future of AR and VR is mobile.”

Mobile VR

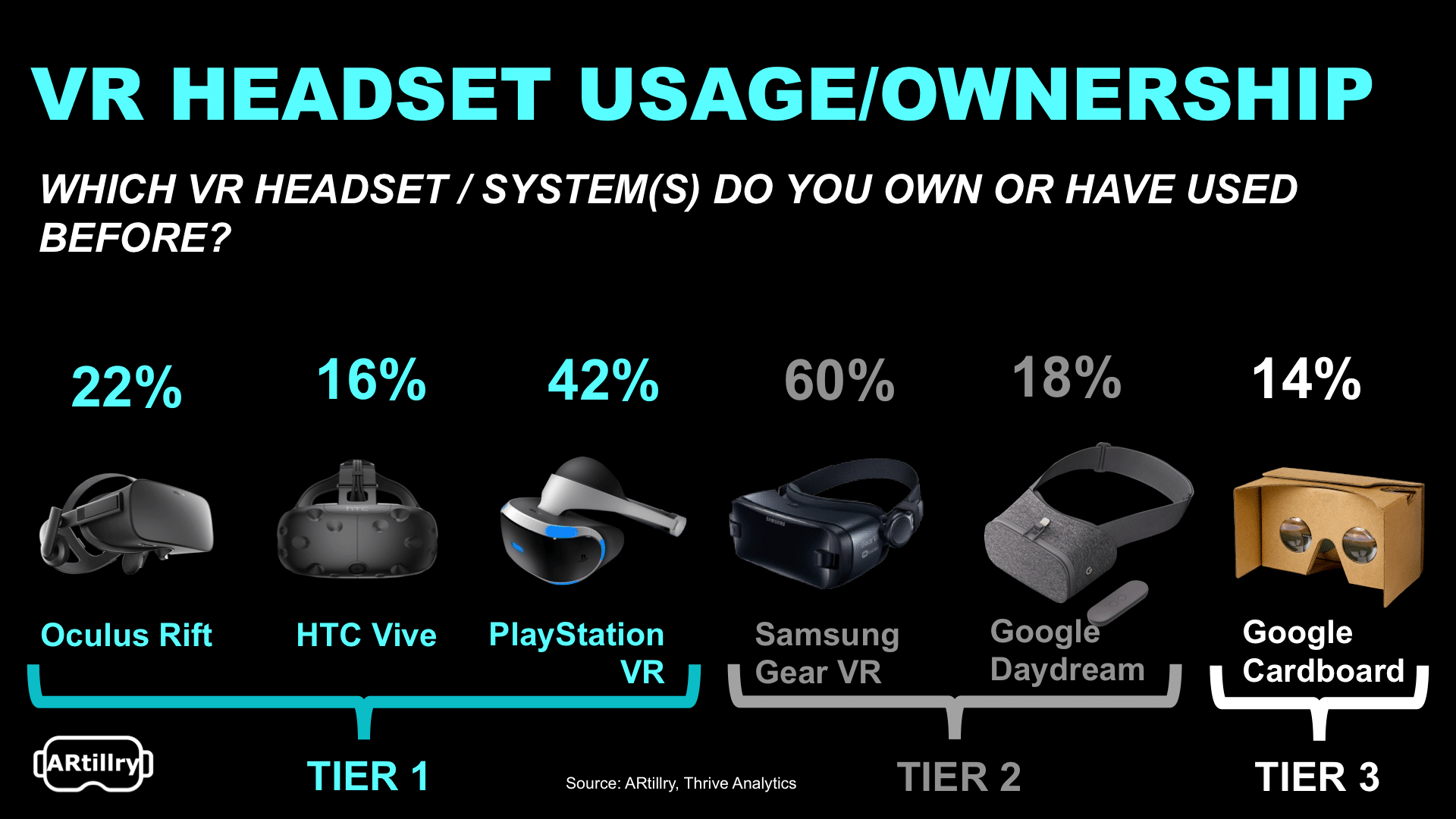

VR headsets segment into three tiers. Tier 1 is high-end tethered VR including Oculus Rift and HTC Vive. Tier 2 includes mobile VR such as Daydream View. Tier 3 is Google Cardboard. A fourth tier is emerging – between tiers 2 and 3 – with Windows Mixed Reality headsets from Asus and others.

Mobile is opportune because it represents VR’s short and long-term opportunity. Near term, mobile devices scale better, used in Tier-2 and 3 headsets. Long-term, mobile processing and optics will be good enough to run higher-end (and untethered) VR experiences approaching today’s tier-1 quality.

Presence Capital Partner Amitt Mahajan agrees with this notion, telling ARtillry that mobile VR will likely catch up to high-end VR in capability, before high-end VR comes down to mobile VR in price. We’re already seeing steps in this direction through “standalone” VR headsets such as Oculus Go.

“I think it’s the equivalent of enterprise-level desktop,” Mahajan said of Tier-1 VR headsets. “PCs were a big thing but the number of people running high-end workstations were pretty small. If high-end VR has a use case that’s mass market, it will be a B2B use case. I think it’s too cumbersome.”

With mobile VR conversely, the opportunities cover a spectrum of supporting technologies. Venture firms like Orange Silicon Valley for example view opportunities through the lens of a global telecom carrier, given the heavy bandwidth requirements for mobile VR that will drive 5G network rollouts.

“Between 2015 and 2018 [Orange has] committed €15 billion to get this infrastructure out,” Orange Silicon Valley’s Kristie Cu told ARtillry. “So there’s a lot of money behind 5G, and VR is one of the driving factors in having the bandwidth.”

Mobile AR

In AR, the story is slightly different. The mobile AR opportunity is greater than mobile VR because smartphones are more conducive to AR. Whereas mobile VR (tiers 2 and 3) carry stark quality differences from tier-1 systems, mobile AR can accomplish closer renditions to top-tier AR systems.

This is mostly due to smartphones’ inherent qualities – portability, GPS, optics – that make them capable of a broad range of AR activities. That capability was further unlocked with the “democratization,” of advanced AR through Apple’s ARkit and Google’s ARCore.

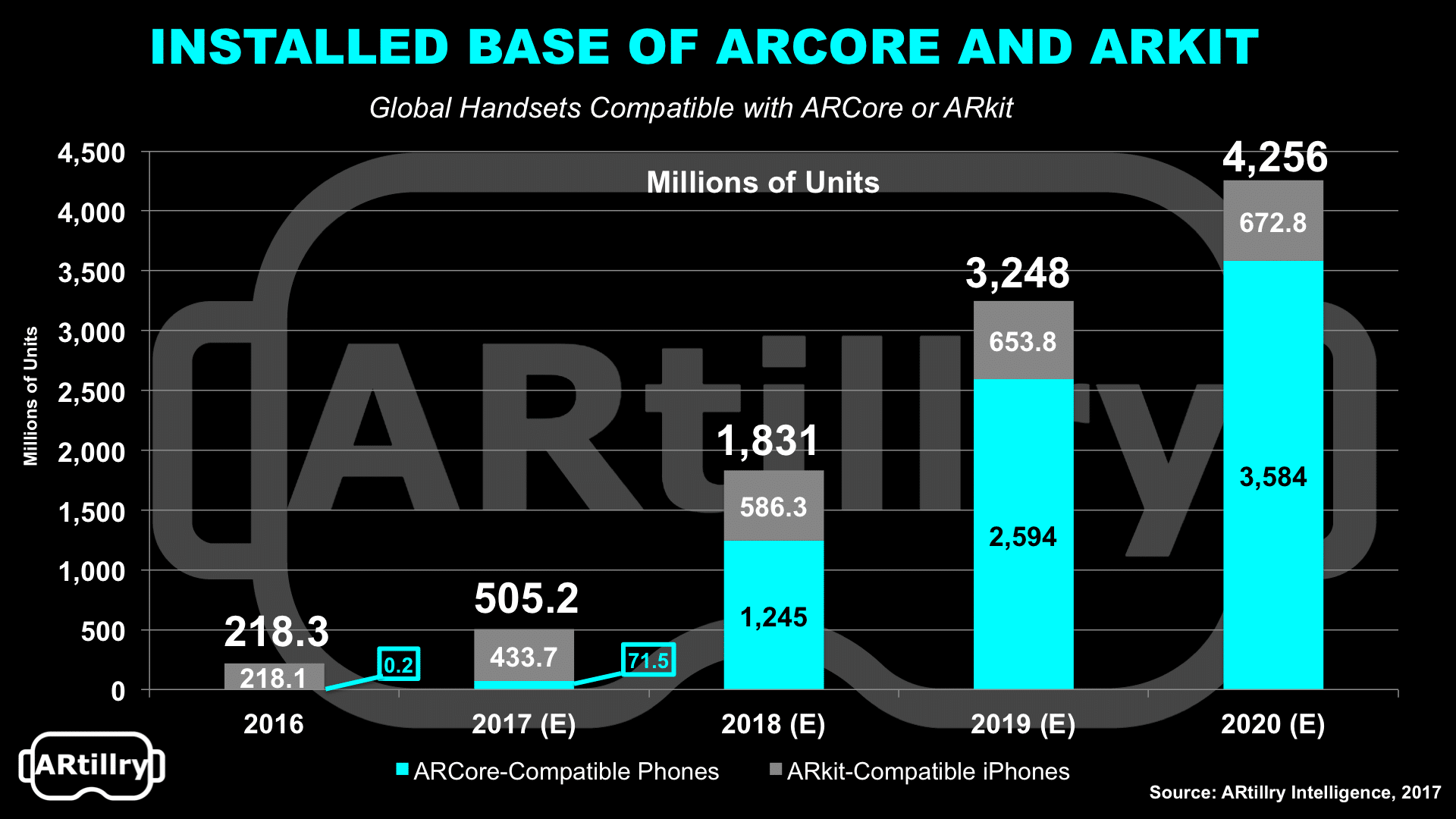

Back to the question of scale, mobile AR hits and exceeds the 100 million mark right out of the gate. ARkit and ARCore create a half-billion AR-compatible smartphones today, increasing to 4.3 billion by 2020 according to ARtillry data. This lowers the barrier for developers, and venture-backed startups.

“We are going to see AR apps become available for ~500 million iPhones in the next 12 months and at least triple that in the following 12 months, as we can now include the numbers of ARCore-supporting devices from Google,” Super Ventures partner Matt Miesnieks wrote recently.

Mobile AR’s benefits also branch from what we call “addressable media time.” Given that our phones are with us all day, mobile AR is eligible for a greater share of our time spent with media (versus television, radio, web, or even VR). Founders Fund partner Cyan Bannister is thinking in these terms.

“I don’t foresee people jacking into VR for eight, nine hours a day,” she said on a TechCrunch podcast. “I’m very bullish on AR and very bearish on VR for that reason… We have these phones in our pockets. Mobile-first AR is going to be massive.”

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.