Most people think of AR as smart glasses that overlay graphics and information in one’s immediate field of view, a la Google Glass. And that’s certainly a form factor being deployed in enterprise environments, as examined in January’s ARtillry Intelligence Briefing.

But it’s also a form factor with long-term consumer potential. Intel projects consumer smart glasses to inflect around 2027 with 50 million annual unit sales, growing to 200 million by 2031. The thought is smart glasses’ consumer utility could eventually parallel that of today’s smartphone.

But until then, AR glasses don’t pass stylistic requirements for consumer markets (size, weight, cost etc.). So consumer AR’s near-term form factor is all about smartphones. You probably know the format: graphical overlays that interact with the world seen through your phone’s camera.

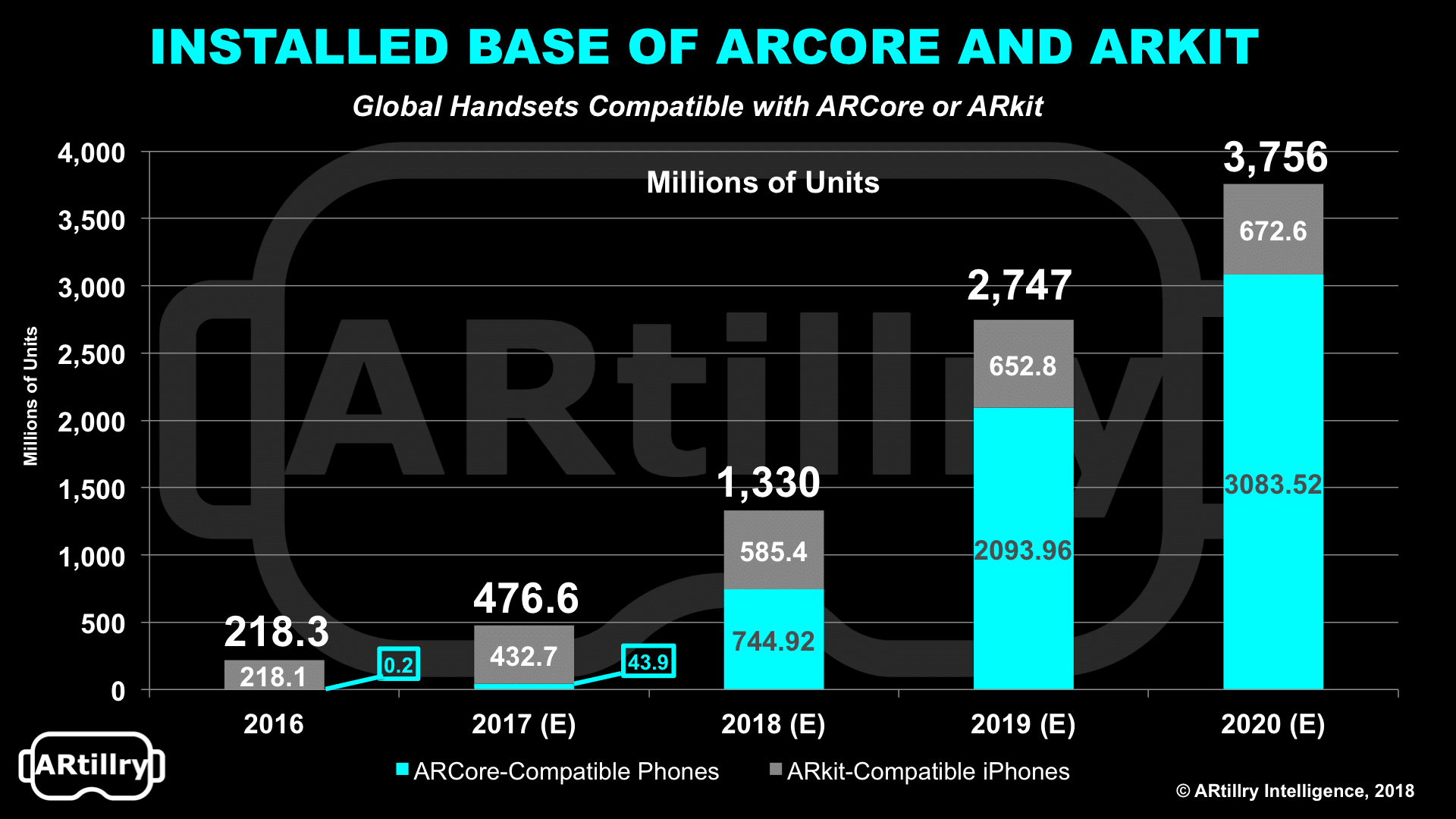

Further positioning the smartphone as a vessel for AR is its ubiquity and permanence as a fixture in our lives. There are 3.5 billion of them. But how many are AR-compatible? There are 476 million today, growing to 1.3 billion by year-end, and 3.8 billion by 2021 – a meaningful installed base.

This volume is mostly due to ARKit and ARCore, which apply software to make AR possible on previously un-compatible hardware (such as standard RGB cameras). Between the two, ARCore has a minority share, but will eclipse ARkit, due to Android’s larger installed base.

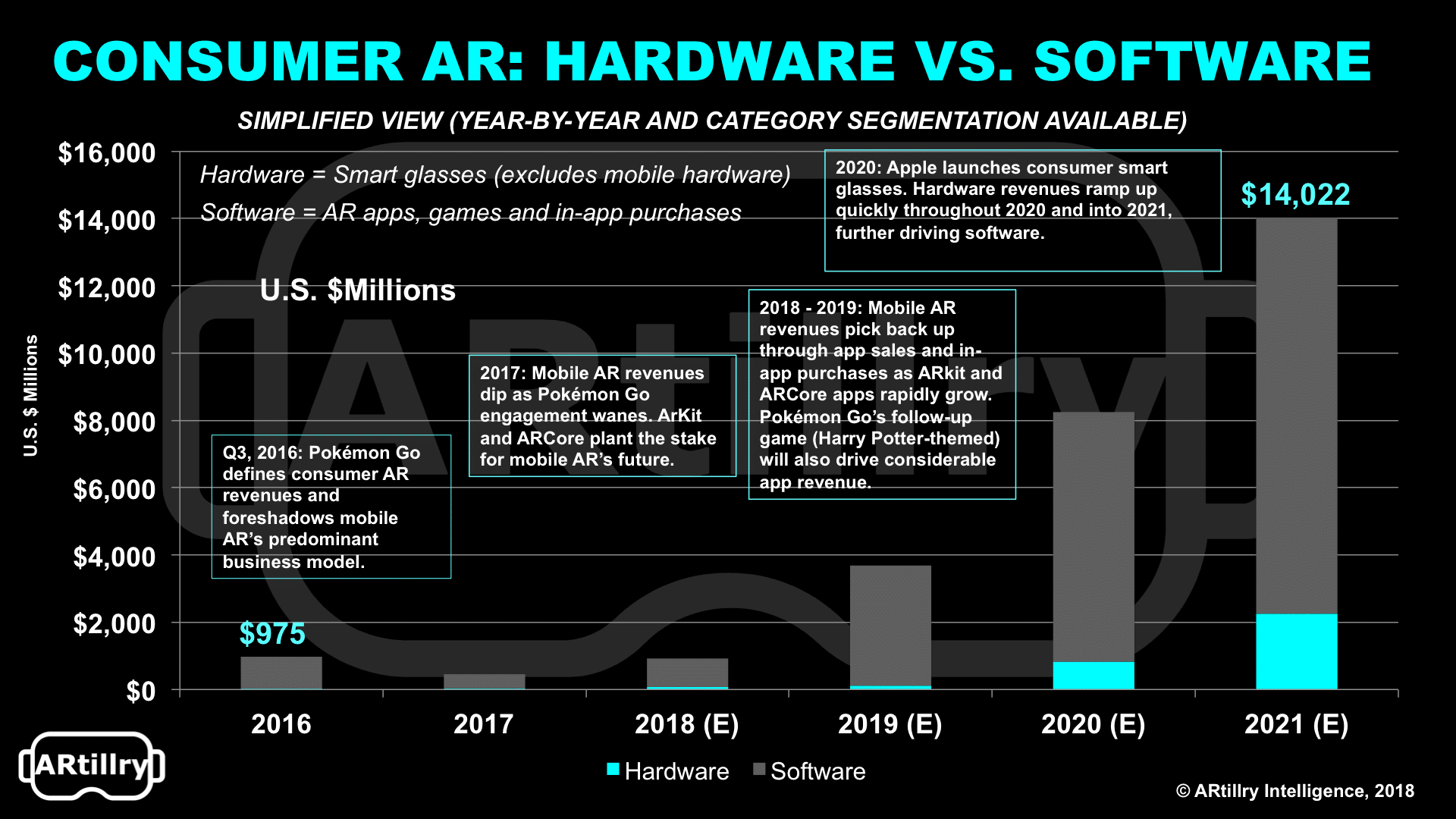

Beyond unit penetration, how does consumer AR stack up in dollars? We project it to grow from $975 million in 2016 to $14.02 billion in 2021. These figures include smart glasses, though it’s important to note that mobile dominates near-term revenue, for reasons explored earlier.

Segmenting mobile’s share, it’s represented by the software portion of our consumer AR projections (see breakdown below). This is because smartphone hardware (e.g. iPhone sales) isn’t counted in our forecast because it’s an already-existing and ubiquitous consumer purchase.

Therefore, near term opportunity for mobile AR is in software. That broad designation includes several things, including premium app sales, in-app purchases, micro-transactions, and others things. These are broken down further in last month’s Intelligence Briefing, and the video below.

Zeroing in on just that software portion of consumer AR revenues, it will grow from 950 million in 2016 to 11.8 billion in 2021. After 2020, AR hardware will start to grow in share, as smart glasses become more viable for consumer markets including cost, style, battery life and other specs

This could include Apple’s rumored smart glasses in the 2021 time frame. It will also include AR glasses in niche or enthusiast areas like cycling, skiing and other sports/recreational areas. Notice that these are areas where glasses or goggles are already worn, forcing less of a behavioral shift.

But until then, the consumer AR sector will be dominated by mobile, with most of the strategy and differentiation happening in software, rather than hardware. But it also faces some challenges and is off to a slow start. In fact mobile AR today resembles iPhone apps ten years ago.

In other words, the sector is underdeveloped in capability, standards, consumer demand and other factors. But that also provides lots of headroom for growth. We’ll continue to see experimentation in the coming month’s as XR players compete for AR’s first true killer app, and that $14 billion.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.

Header image credit: BMW