“Behind the Numbers” is ARtillry’s series that examines strategic takeaways from its original data. Each post drills down on one topic or chart. Subscribe for access to the full library and other knowledge-building resources.

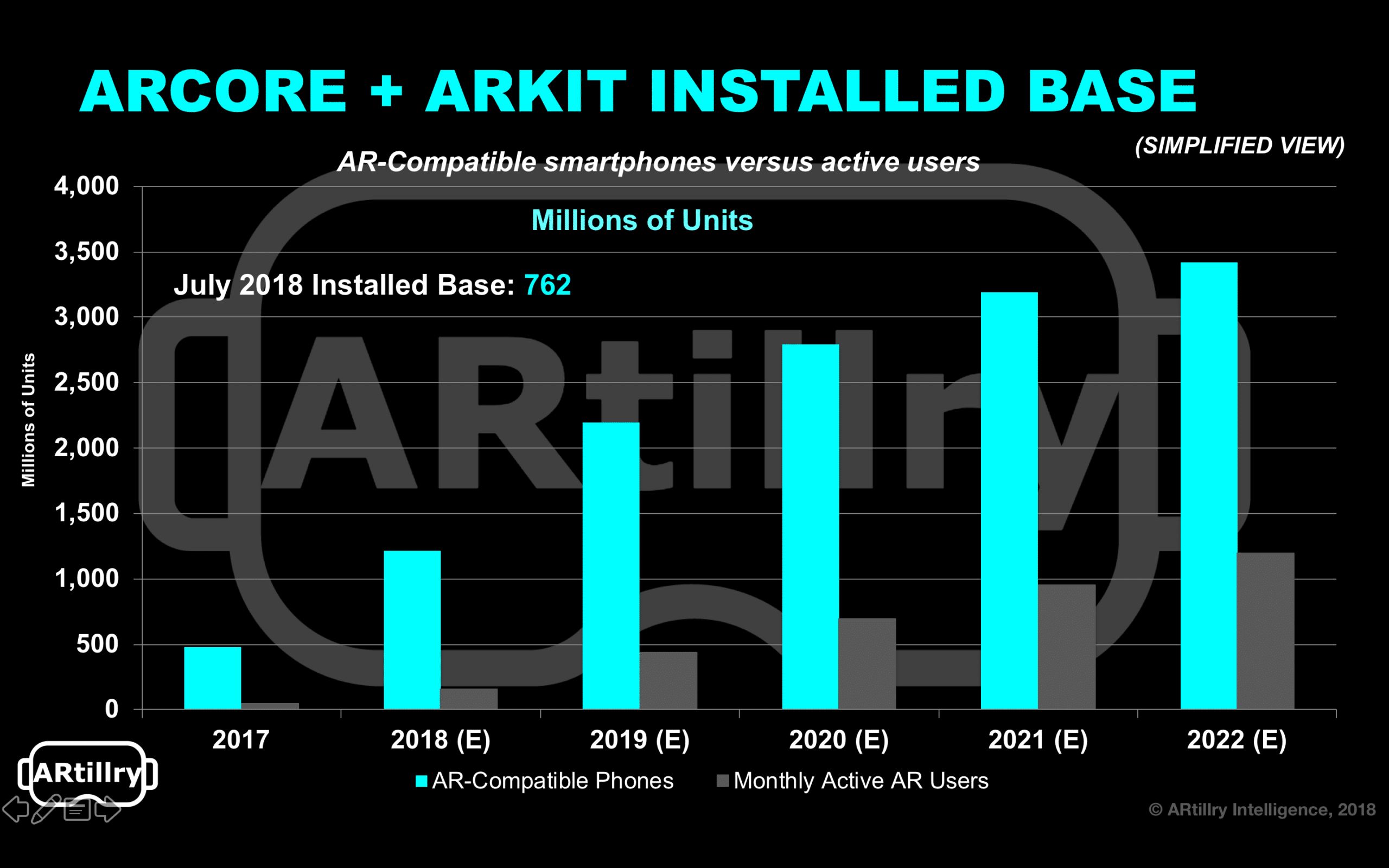

In the oral tradition of the XR sector’s early stages, common wisdom is that AR-compatible smartphones total half a billion. But cited-figures tend to lag behind current ones: our latest calculations have pegged the updated smartphone-AR compatibility figures at 762 million.

The previous half-billion figure — a common talking point at industry events and pitch decks –aligns with our figures from late last year. But figures like this are a moving target, especially when there’s rapid early-stage growth tied to hardware replacement cycles. Or as we wrote in March:

One question that arises from these figures is why are they growing so rapidly. They over-index for growth rates when compared to several growth-phase industries in the forecasting trade. For both ARCore and ARkit, they go from zero to billions over a five-year period.

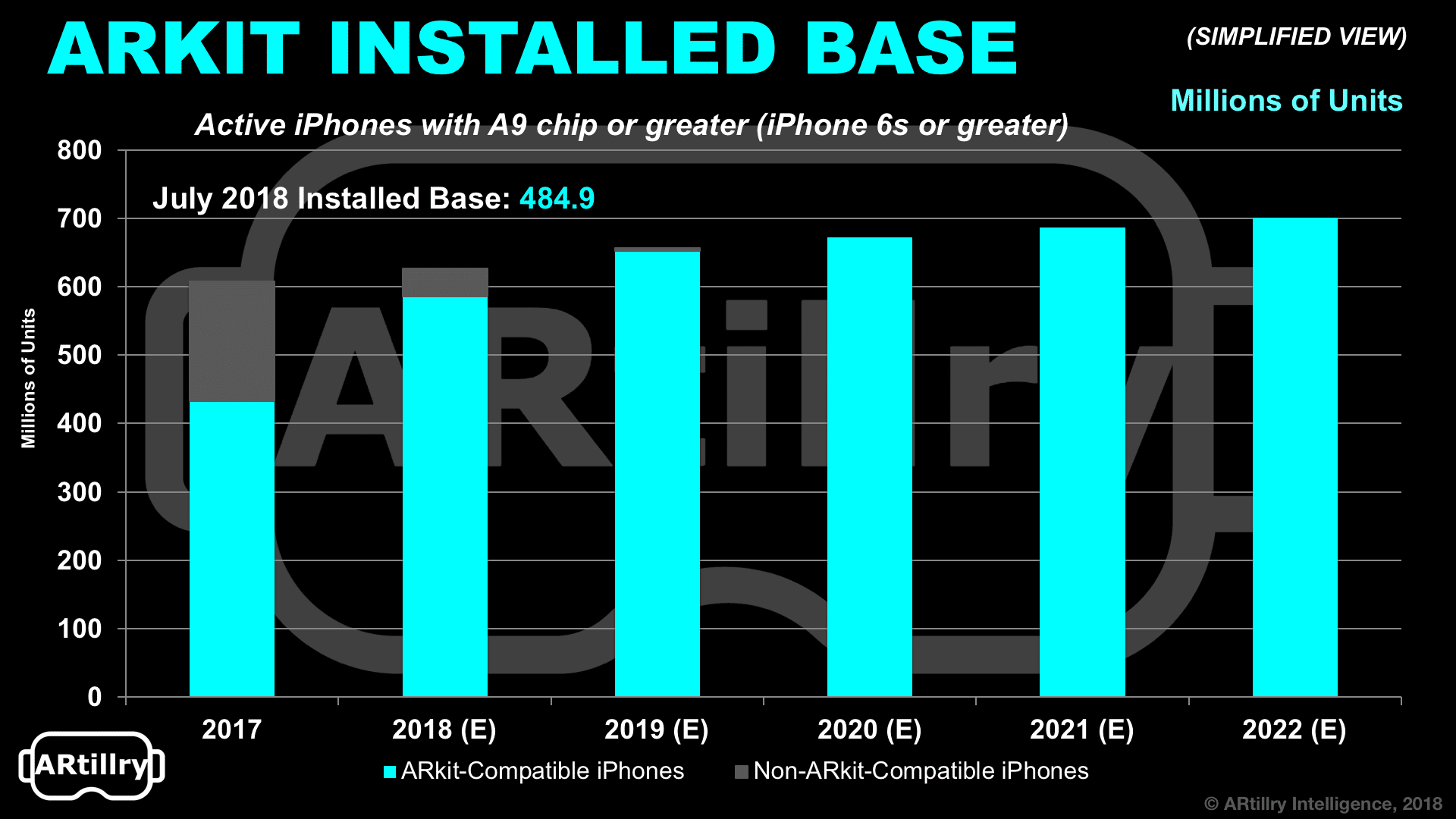

One reason is that the metric is unit-compatibility, not dollars. Another reason is average mobile hardware replacement cycles, which follow a set pace (currently 2.5 years). This will cause AR-compatibility – for example, A9 chips or greater in iOS devices – to cycle in rapidly.

Moving Target

So how do we come up with these figures? Some parts are simple and some aren’t. In total, there are several market signals and inputs including things like quarterly sales of AR-compatible smartphones. Those will cycle in as older units cycle out, given a 2.5 year replacement cycle.

That’s a bit easier for ARkit, given that all phones with A9 chips or greater check out. It’s further simplified by Apple’s vertical integration, which gives it more fine-tune control over sensor calibration and optics. And a unified hardware base facilitates widespread software updates.

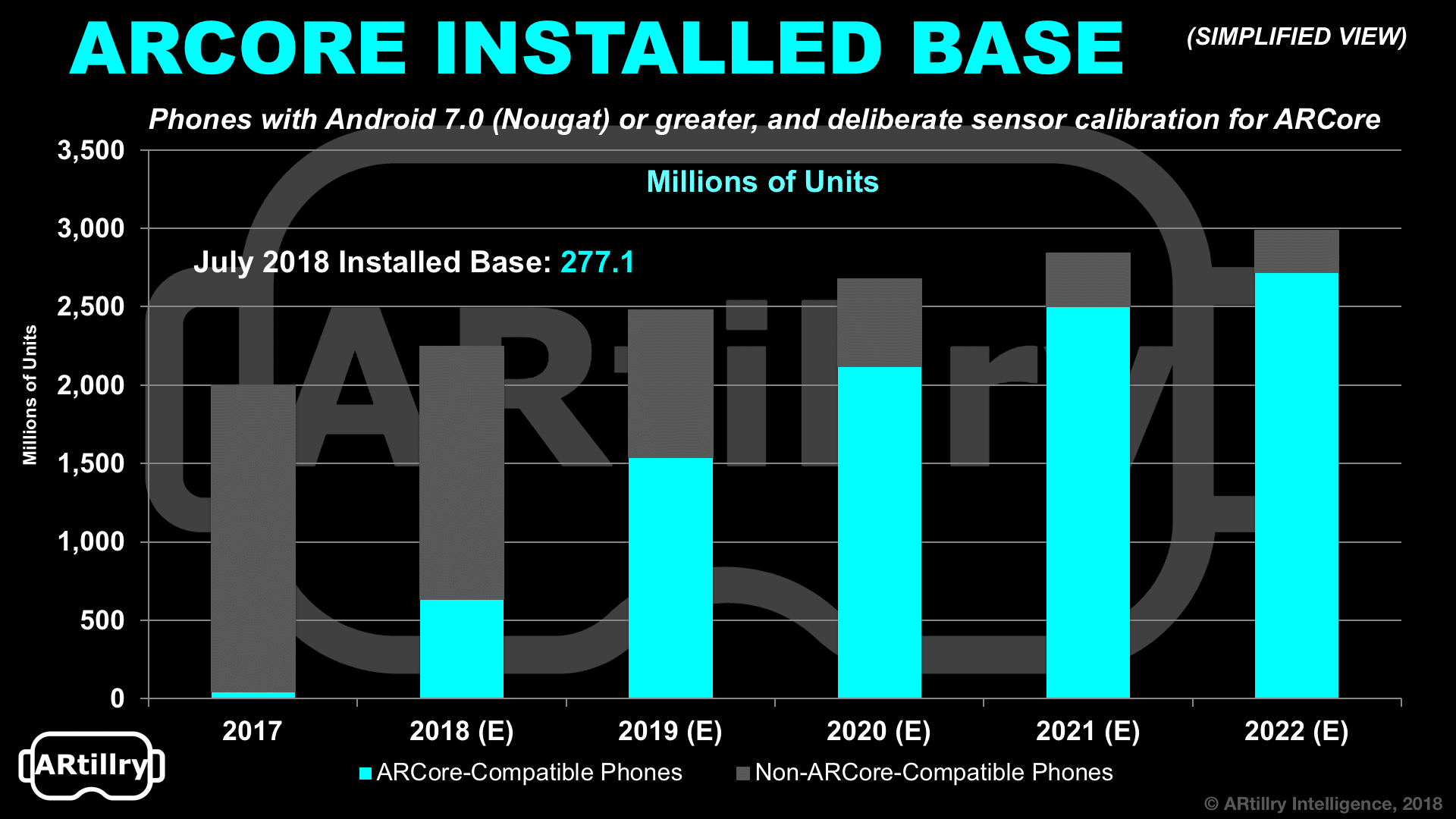

As explored further below, Android is more fragmented and laggard in firmware updates. But these are still decent market signals to model AR-compatible device penetration. The real wild card in the Android equation is China: Non-Google Play app marketplaces create some uncertainty.

Regardless, competition between Google and Apple — stemming from their battle positions in the smartphone era — will drive these figures up. Don’t forget Facebook Camera Effects, Snapchat Lens studio and other platforms. That competition is good but it fragments the market a bit.

The Long Game

Expanding on competitive positioning, Apple has the short-run reach advantage, due to a more unified hardware and software set that supports wider ARkit compatibility. But Google will have the longer-term scale as ARCore compatibility cycles into the larger Android universe.

That will take longer for ARCore, given a fragmented base of Android devices which makes it difficult for Google to herd OEM cats and push software updates comprehensively. For example, about 16 percent of Android devices run OS versions released in the previous year.

ARCore specifically requires Android 8.0 or greater, and Google Play access (an issue in China). Beyond OS are hardware specs such as optics and sensor calibration, which are difficult to mandate across several OEMs. But despite challenges, ARCore devices will expand rapidly.

ARkit and ARCore also carry their parents’ DNA. For Apple, it’s all about apps; for Google, the web. For developers, that means ARCore could reach more users, but ARkit could be more monetizable though standard app revenue models (i.e. downloads, in-app purchases, etc.).

Key Ingredients

Speaking of business models, that’s another piece of mobile AR puzzle. We’re bullish on in-app purchases (IAP), given that it’s an established model in mobile gaming. It’s also been validated in AR by roughly $1.4 billion in Pokemon Go revenue, and our consumer AR survey data.

Another factor stemming from these figures is how mobile AR’s larger market attracts developers from VR. As we predicted, this is already happening due to “osmosis” of developer talent to sectors with greater financial incentive. Developer muscle will be key ingredient in AR growth.

Bottom line: mobile AR has a lot of potential scale. But “potential” is the key word: Installed base is an addressable market, not necessarily an actual one. A more relevant metric is the number of currently active users, which we’ve pegged at 158 million globally in our latest forecast.

The question is how that addressable market evolves to an actual one. It will be a volatile and opportunistic time, like early days of the smartphone revolution. And just like that period, it will reward developers that find their native footing, and hinge on the introduction of a killer app or two.

Stay tuned for more analysis and market sizing as we lock in and pan our sights to the moving target that is the XR market.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.