Data Point of the Week is AR Insider’s dive into the latest spatial computing figures. It includes data points, along with narrative insights and takeaways. For an indexed collection of data and reports, subscribe to ARtillery Pro.

One leading indicator for products in any sector is what developers are working on now. In that spirit, XRDC is out with its perennial innovation report for developers’ reported XR activity. As with past reports, this survey is done as a primer for the upcoming XRDC Conference.

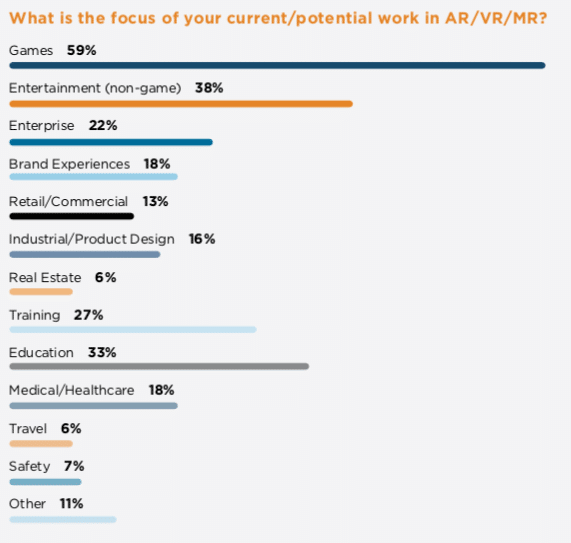

So what are the latest results? Starting at the top, most developers are working on games (59 percent) followed by non-gaming entertainment (38 percent) followed by education (33 percent), enterprise (22 percent) and brand experiences (18 percent). The rest is in the chart below.

These results are logical and align somewhat with the revenue shares of these respective categories (see revenue share breakdowns from our research arm, ARtillery Intelligence). But that’s ambiguated to some degree by the fact that AR and VR aren’t segmented.

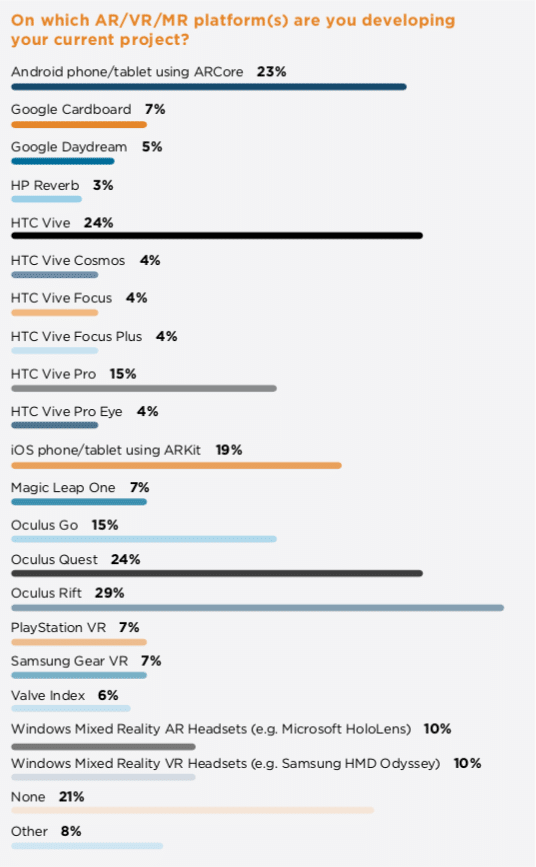

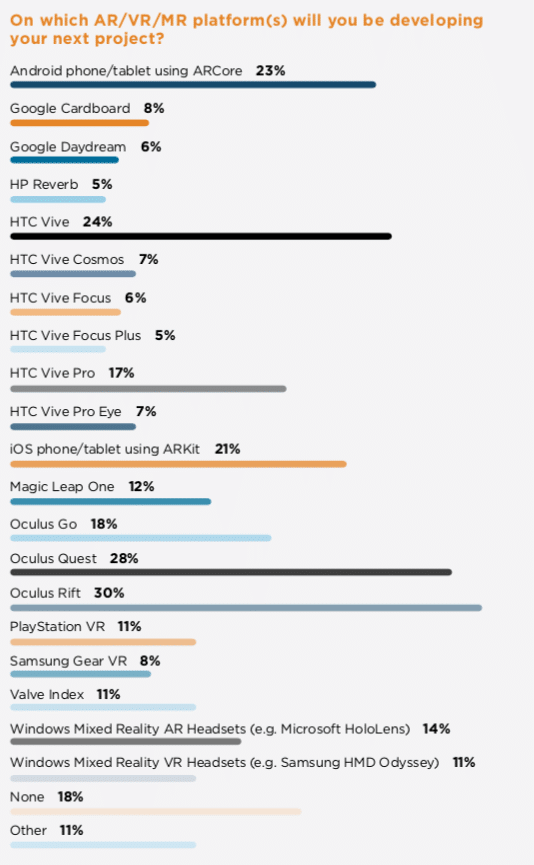

As for specific platforms developers are working with, that’s where things start to segment into AR and VR. Starting with AR, ARCore has the greatest mobile platform activity with 23 percent, but ARCore is catching up to it, and growing at a faster pace from reported past projects.

For headset based AR, Windows Mixed Reality (Hololens) is in the lead by 10 percent of current projects. But more notably, that jumps to 14 percent for reported future projects. Magic Leap isn’t far behind, growing from 7 percent of current projects to 12 percent of future interest.

Shifting to VR, HTC Vive was once the developer favorite in past XRDC surveys. Now it’s eclipsed by Rift with 29 percent of current activity and 30 percent of future interest. Oculus Quest is the biggest mover, not surprisingly, going from 12 to 24 to 28 in the past/present/future split.

As with all survey-based studies (including that of our research arm ARtillery Intelligence) aspirational or future-looking data should be taken with its appropriate salt tonnage. Either way, these results are valuable in their directional indications and demand signals.

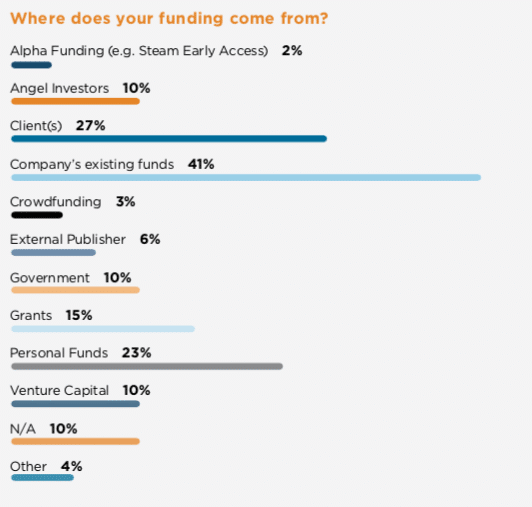

Lastly, in terms of business metrics, most companies’ funding sources (41 percent) come from the somewhat ambiguous “existing funds.” The second-biggest category is “clients,” indicating measured bootstrapping activity and real revenue. This is a good sign for immersive computing.

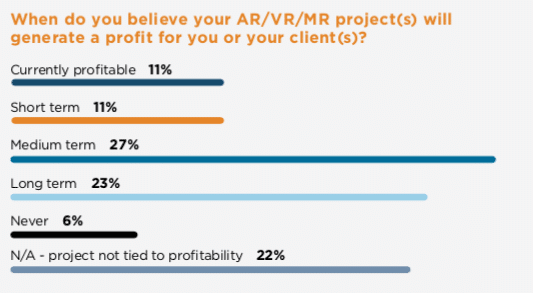

Estimating when projects will generate profit for companies or their clients, most responded with the medium term (27 percent), followed by long term (23 percent). Though the above “aspirational” point remains, this shows some real honesty and awareness. Even 6 percent reported “never.”

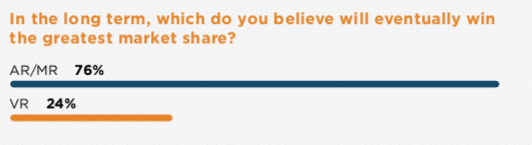

As for the overall split of AR and VR, the vast majority of respondents (76 percent) believe the former will have a greater market share. “Market share” is probably the wrong term, as they’re not competing in the same markets, but the point is taken that AR has greater monetization potential.

Overall, this is a valuable look at developers’ sentiments and real current activity for their projects. And most of the results stand up to reason and other data we’re tracking. We’ll keep watching all spatial computing sub-segments to see how their growth tracks to these leading indicators.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.

Header Image Credit: InformaTech