Data Point of the Week is AR Insider’s dive into the latest spatial computing figures. It includes data points, along with narrative insights and takeaways. For an indexed collection of data and reports, subscribe to ARtillery Pro.

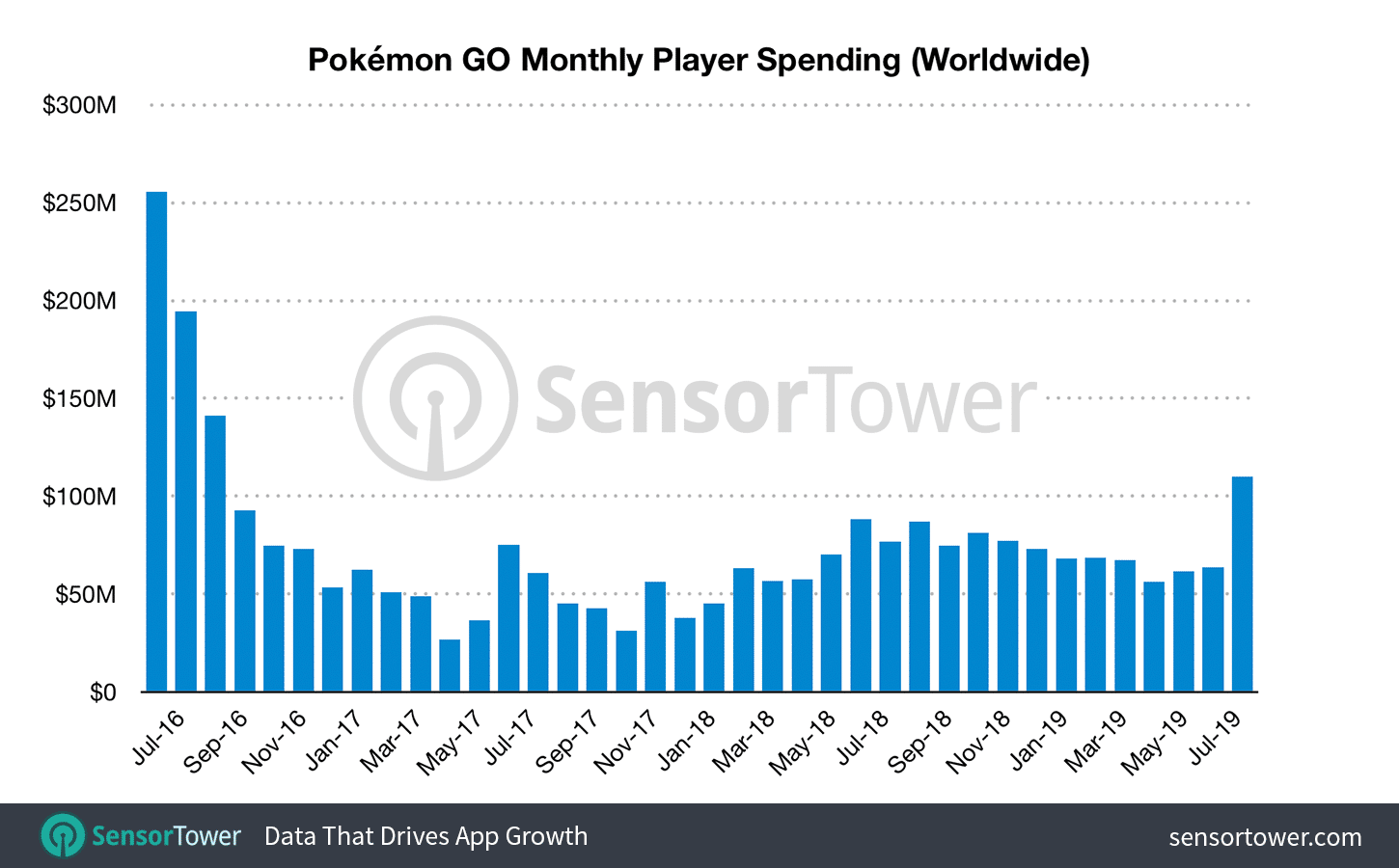

Despite falling from its Q3 2016 peak (an expected outcome) Pokemon Go has been on a tear in 2019. And it just had its biggest revenue month in three years and fourth-largest to date. Specifically, it brought in $110 million according to Sensor Tower estimates (chart below).

This is a 44 percent increase over August 2018’s $76 million (year-over-year); and a 76 percent increase over July 2019’s $63.5 million (month-over-month). It correlates to new user growth of 10 percent year-over-year versus August 2018’s user growth of 5.2 percent over the previous year.

Most revenue in August came from the U.S. (40 percent) followed by Japan (31 percent). Japan leads in all-time revenue with revenue per user (ARPU) of $45 compared with the U.S. ARPU of $10. This speaks to consumer spending patterns for in-app purchases (more on that in a bit).

Panning back to Pokemon Go’s standing on the global stage, its August monthly revenue total was fourth place behind Honor of Kings ($141 million), Fate/Grand Order ($159 million), and PUBG Mobile ($160 million). Niantic’s Harry Potter Wizards Unite (HPWU) is also showing strong signs.

As for what caused the August revenue surge, the likely source is the incorporation of franchise antagonists Team Rocket into the gameplay. This breathed new life into the game elements, which is the name of the game (excuse the pun) in maturing titles, as Niantic knows well.

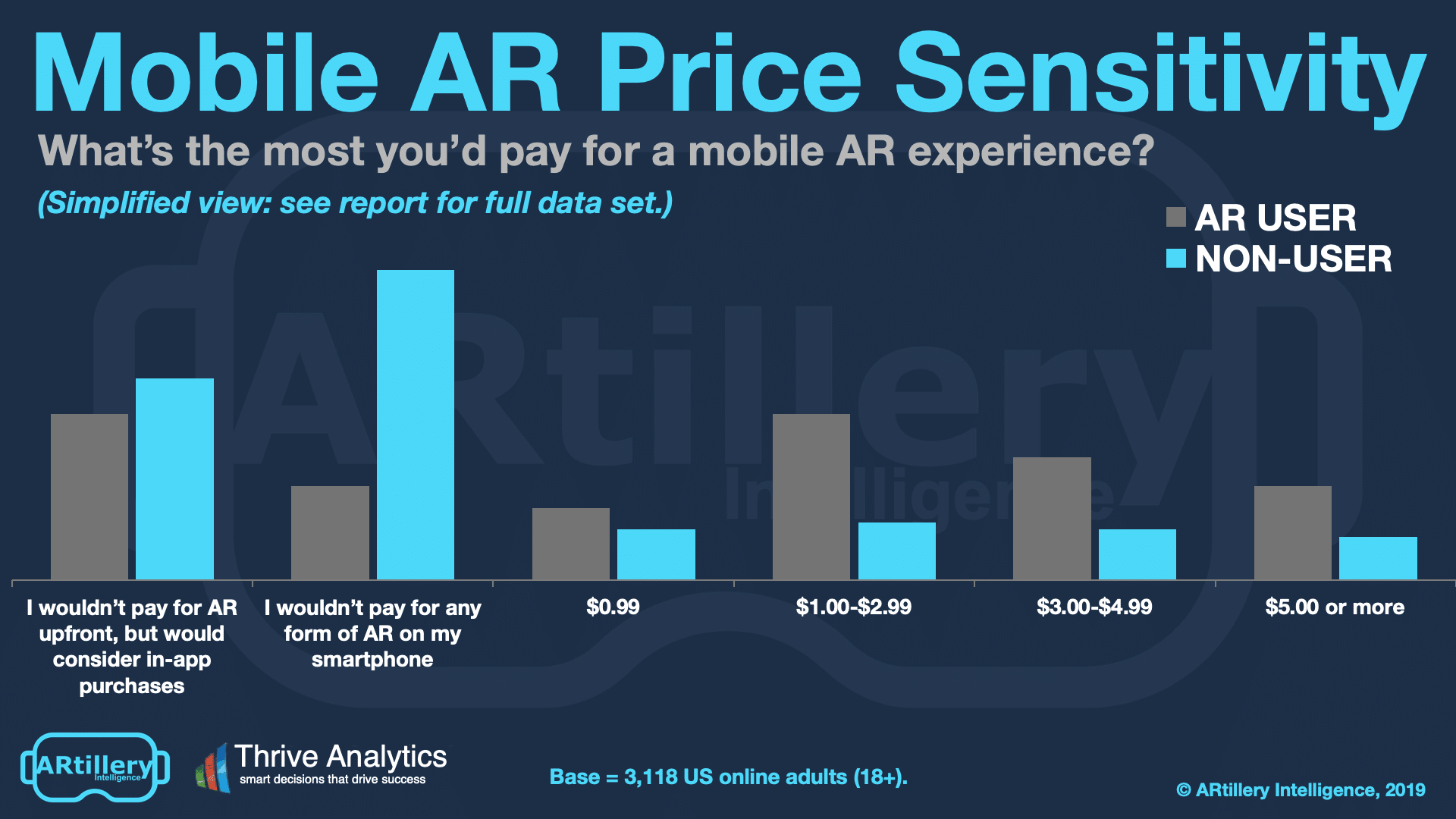

As for the revenue dynamics in Pokemon Go, it continues to be dominated by in-app-purchases (IAP). This is a strong signal for IAP as a revenue model in AR. As supported by consumer survey data from our research arm ARtillery Intelligence, IAP is a prudent model for AR gaming.

The rationale is that AR is too new and unproven to get consumers to pay upfront for premium apps. That plus acclimation/comfort levels consumers have developed for in-app purchases in non-AR games (Candy Crush, Fortnite, Clash of Kings, etc.) make it the go-to model.

Interestingly, in other popular areas of consumer AR such as social lenses, the revenue source is brand advertising. That’s mostly because it’s becoming an effective way for brands to engage consumers with immersive product try-ons. That “subsidy” if you will, makes it free for users.

But one of our predictions is that social lens players like Snapchat and Facebook will introduce consumer-pay options for lenses. The model there is what Snapchat did with Geofilters, where consumers can create and unlock a lens around a geofence and timeframe (think: birthday party).

Meanwhile, the clear delineations in revenue models are IAP for gaming and brand advertising for social AR lenses. These dynamics are top of mind as our research arm, ARtillery Intelligence, works on its October Intelligence Briefing on mobile AR strategies and business models.

We’ll have lots of findings and highlights from that report to share in a few weeks. Meanwhile, Pokemon Go’s revenue resurgence provides some good fodder for analysis and strategic implications. We’ll keep watching Niantic’s moves (including HPWU) and how the market reacts.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.