Data Point of the Week is AR Insider’s dive into the latest spatial computing figures. It includes data points, along with narrative insights and takeaways. For an indexed collection of data and reports, subscribe to ARtillery Pro.

One of the many ways to get a temperature of industry health is to survey its executives on adoption and spending levels. This can have some “aspirational” results, but if taken directionally and with a grain of salt, executive surveys can provide real insight.

With that backdrop, VR Intelligence launched its latest survey to prime the pump for its December VRX conference. This follows our recent analysis of XRDC’s similar industry survey, and the two can be used together for more data points and to triangulate trends.

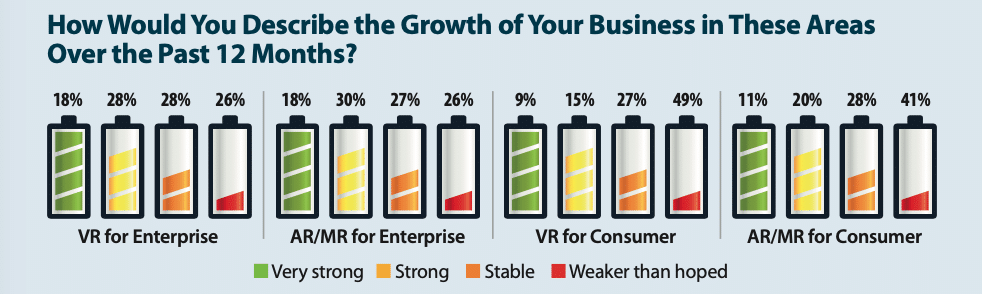

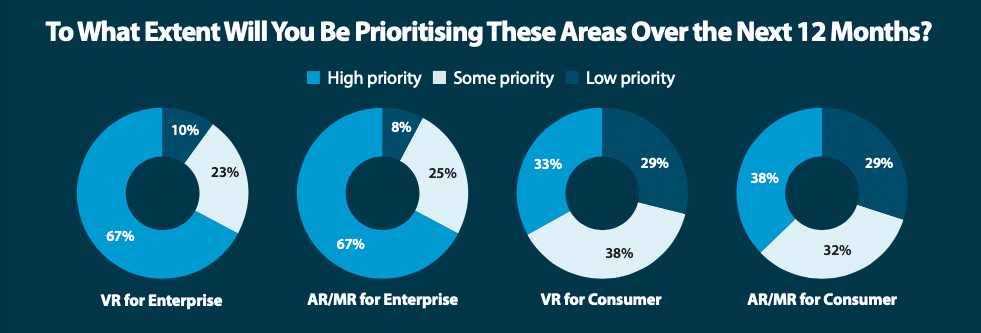

Among the results, one macro trend that emerged was the confidence execs have in enterprise AR and VR relative to consumer products. This isn’t surprising given enterprise’s well-documented early lead in XR (especially AR), compared to consumer adoption as a whole.

It also should be noted that the survey sample skewed towards companies that are themselves building and focusing on enterprise AR and VR products (see infographic below). Nonetheless, the bullish attitude towards enterprise versus consumer is notable and somewhat expected.

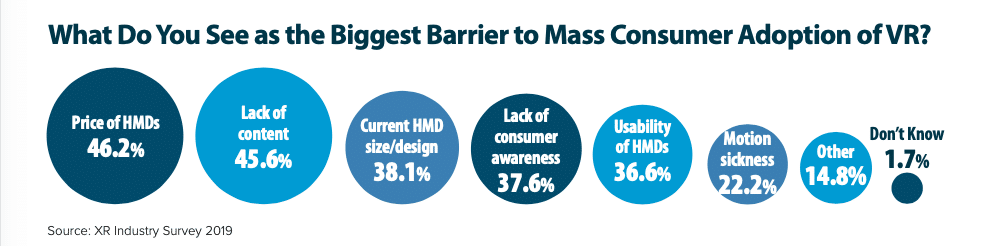

Going deeper, price, content and hardware bulk were seen as the biggest barriers to consumer adoption of VR headsets. This notably aligns with the consumer survey data from our research arm ARtillery Intelligence, showing that these executives surveyed are in tune with consumers.

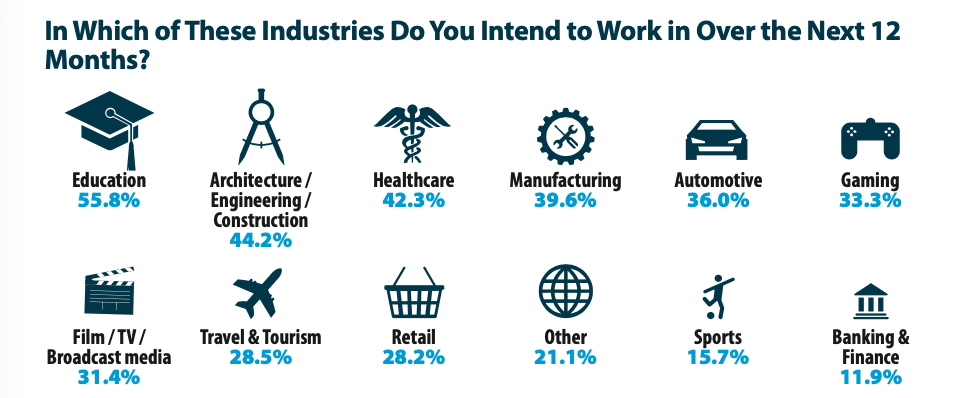

As for the verticals that hold the most promise, respondents (again, potentially biased towards their product) chose education, followed by AEC, healthcare, manufacturing, automotive and gaming. These align somewhat with our past analysis of adoption patterns across XR verticals.

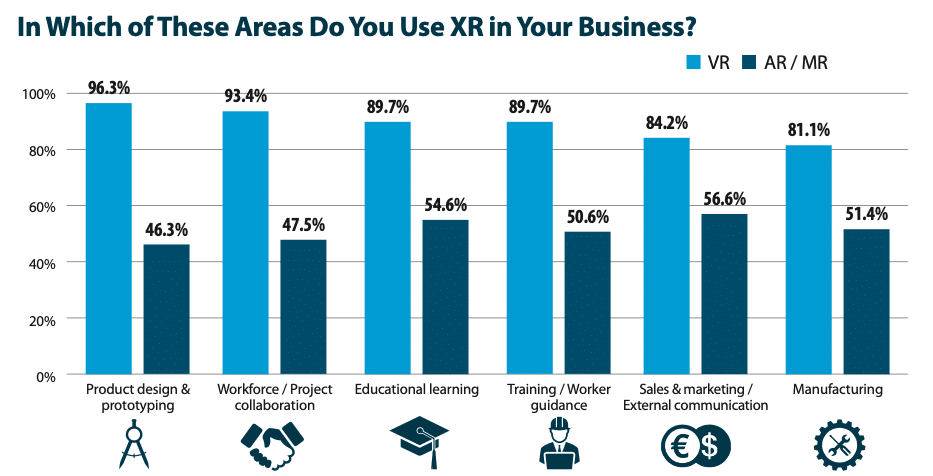

Drilling down on the functions for AR and VR’s intended use, product prototyping, workforce collaboration, educational learning and training unsurprisingly got the highest marks for VR. Meanwhile, sales & marketing, educational learning and manufacturing scored highest for AR.

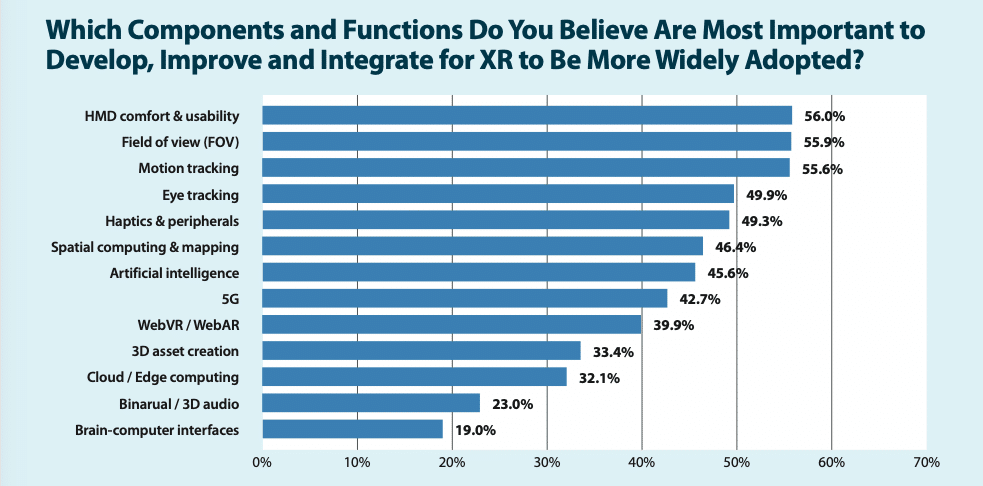

For product attributes and functionality that execs and their companies are prioritizing, headset comfort, field of view and motion tracking scored highest. These make sense as “table stakes” attributes that need to be solved in order to penetrate mainstream markets.

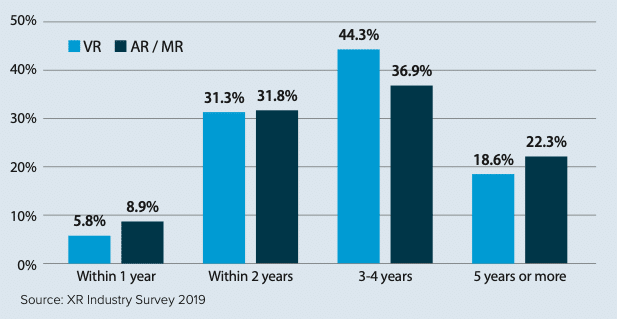

As for timing to wide-scale consumer XR adoption, respondents predominantly chose 3-4 years. The adoption dynamics and technology life stages of course vary for AR and VR but these answers are still telling about XR execs (though inherently biased) optimism for time-to-market.

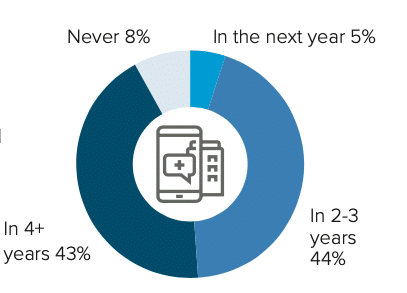

Related to the matter of timing is a question of when adoption trend lines between mobile AR and smart glasses will intersect. 44 percent believe it’s in 2-3 years and 43 percent think 4+ years. A minority (5 percent) think within one year and 8 percent think it will never happen.

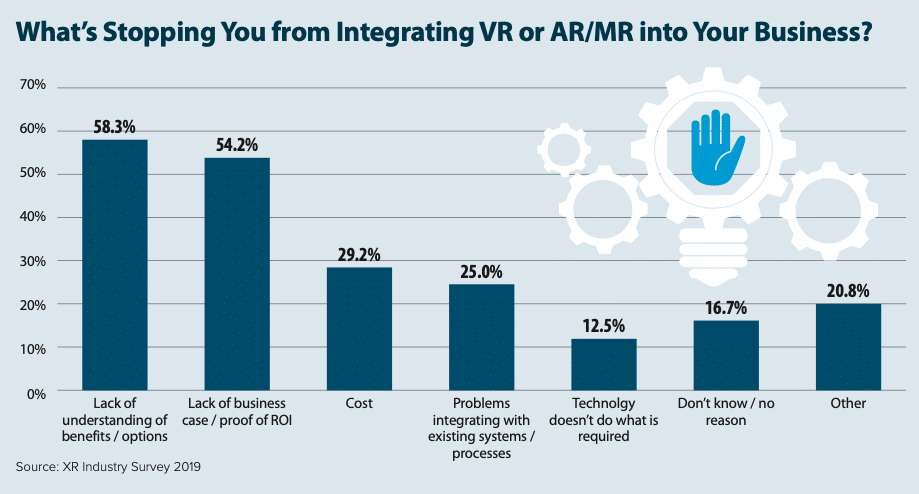

For enterprises not sold on AR and VR, a key question is “why not?” Top answers to that question were lack of understanding of benefits, and lack of ROI proof. AR has overwhelming proof of enterprise ROI gains, so these answers signal the need for more enterprise education.

The infographic which summarizes the report highlights can be seen below, and you can download the full report (free with registration) here. We’ll tack this up with the broader mosaic of XR industry data to continue triangulating top trends and their strategic implications.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.

Header Image Credit: Varjo