![]() This post is adapted from ARtillery Intelligence’s report, AR Advertising Deep Dive, Part I: The Landscape. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

This post is adapted from ARtillery Intelligence’s report, AR Advertising Deep Dive, Part I: The Landscape. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

AR continues to evolve and take shape as an industry. Prominent sectors include industrial AR, social, gaming, and shopping. But existing alongside all of them is AR advertising. This includes paid/sponsored AR lenses that let consumers visualize products on “spaces & faces.”

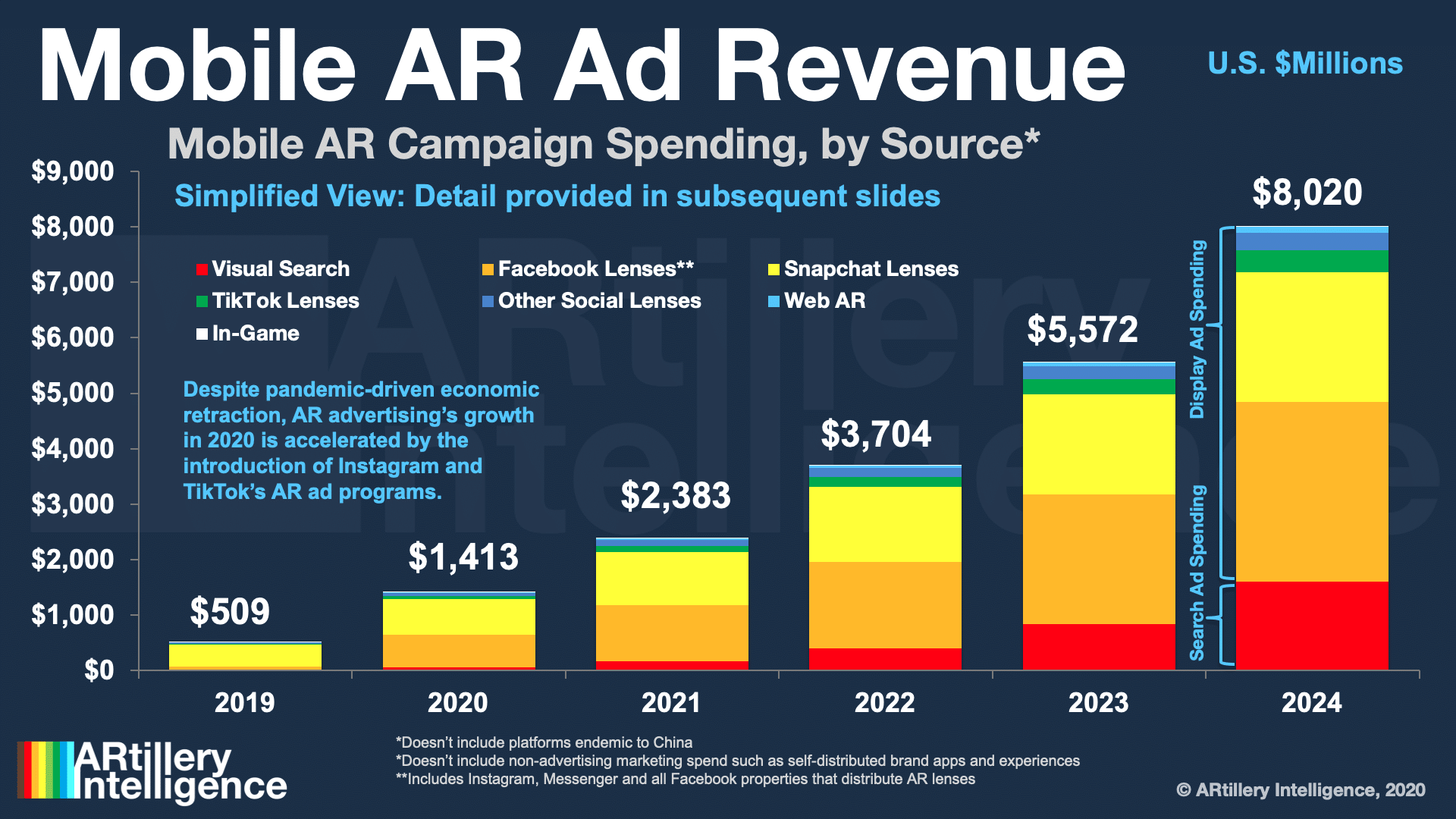

Advertising is one of the most lucrative AR subsectors, on pace to reach $1.41 billion this year and $8.02 billion by 2024. These figures measure the money spent on sponsored AR experiences with paid distribution on networks like Facebook and Snapchat.

As we’ve examined in past reports, the factors propelling this revenue growth include brand advertisers’ growing affinity for AR. Its ability to demonstrate products in immersive ways resonates with their creative sensibilities, transcending what’s possible in 2D formats.

Beyond that high-level appeal, there’s a real business case. AR ad campaigns continue to show strong performance metrics. This was the case in “normal” times and has accelerated during the COVID era, when retail lockdowns compel AR’s ability to visualize products remotely.

Platform Rundown

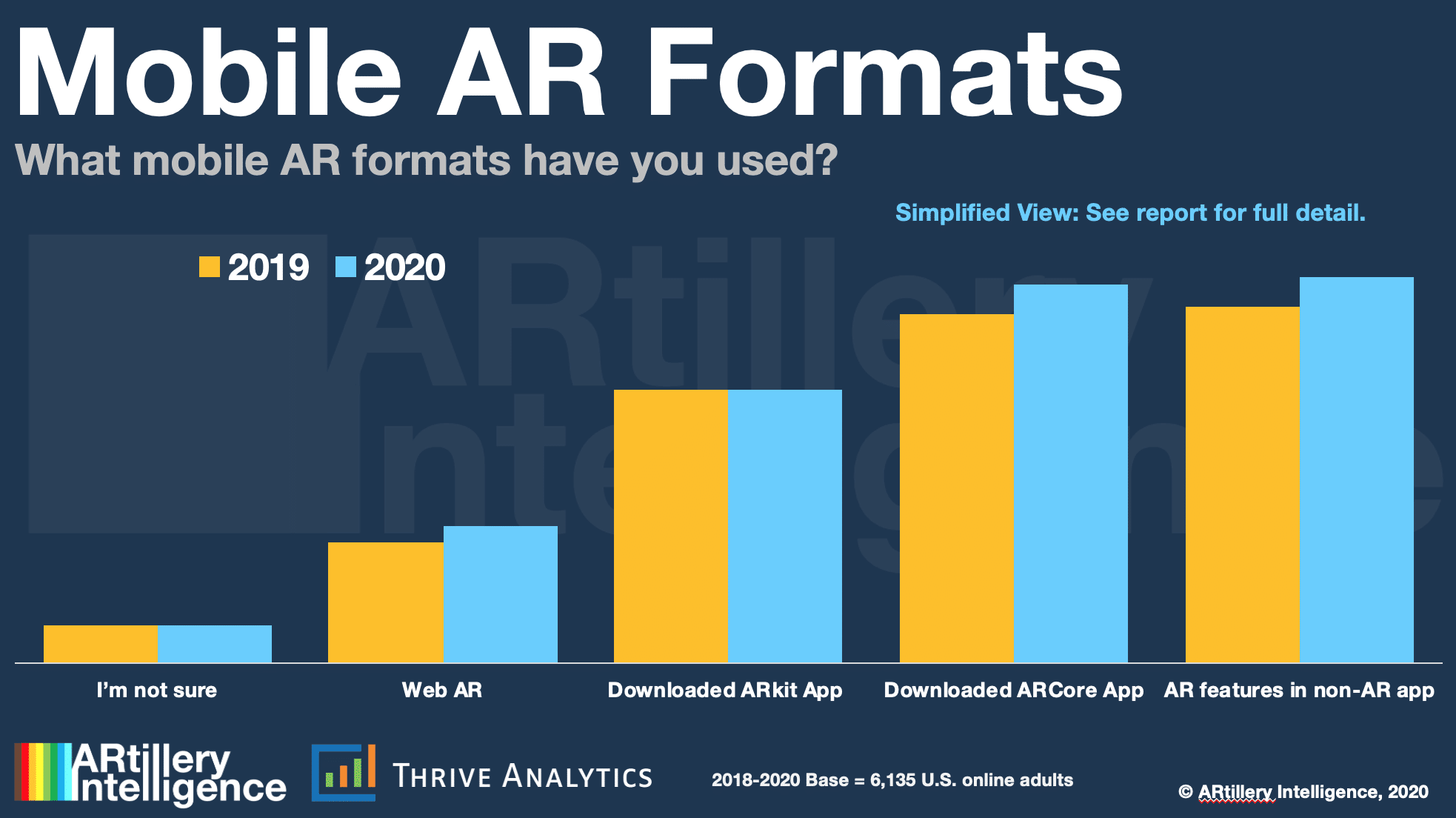

After profiling several AR ad platforms in this report, how do they stack up quantitatively and qualitatively? These include social apps that offer sponsored lens experiences, as well as web AR. Starting with quantitative analysis ARtillery’s recent survey findings can provide more color.

When asked what types of AR formats users have tried, the leading category was “AR as a feature.” To define that, it’s AR experiences that have been integrated into existing (non-AR) apps. That includes many of the social AR platforms in this report including Facebook and Snapchat.

Web AR meanwhile lingers at 18 percent of survey responses. That’s not surprising given its early stage of development. Though its current active use is lowest among platforms, its installed base is greatest — meaning it has the biggest shell to grow into (see data in the next section).

As for apps, they perform well in the survey, but we’ll set them aside for now. That’s because this report focuses on AR paid ad distribution. ARkit and ARCore apps are rather used as marketing channels for brands to invest in their own self-distributed experiences (e.g. BMW iVisualizer).

But for web AR and AR-as-a-feature (including lenses in social platforms), usage levels are telling of the potential these formats hold as advertising channels to distribute sponsored AR lenses.

Compare & Contrast

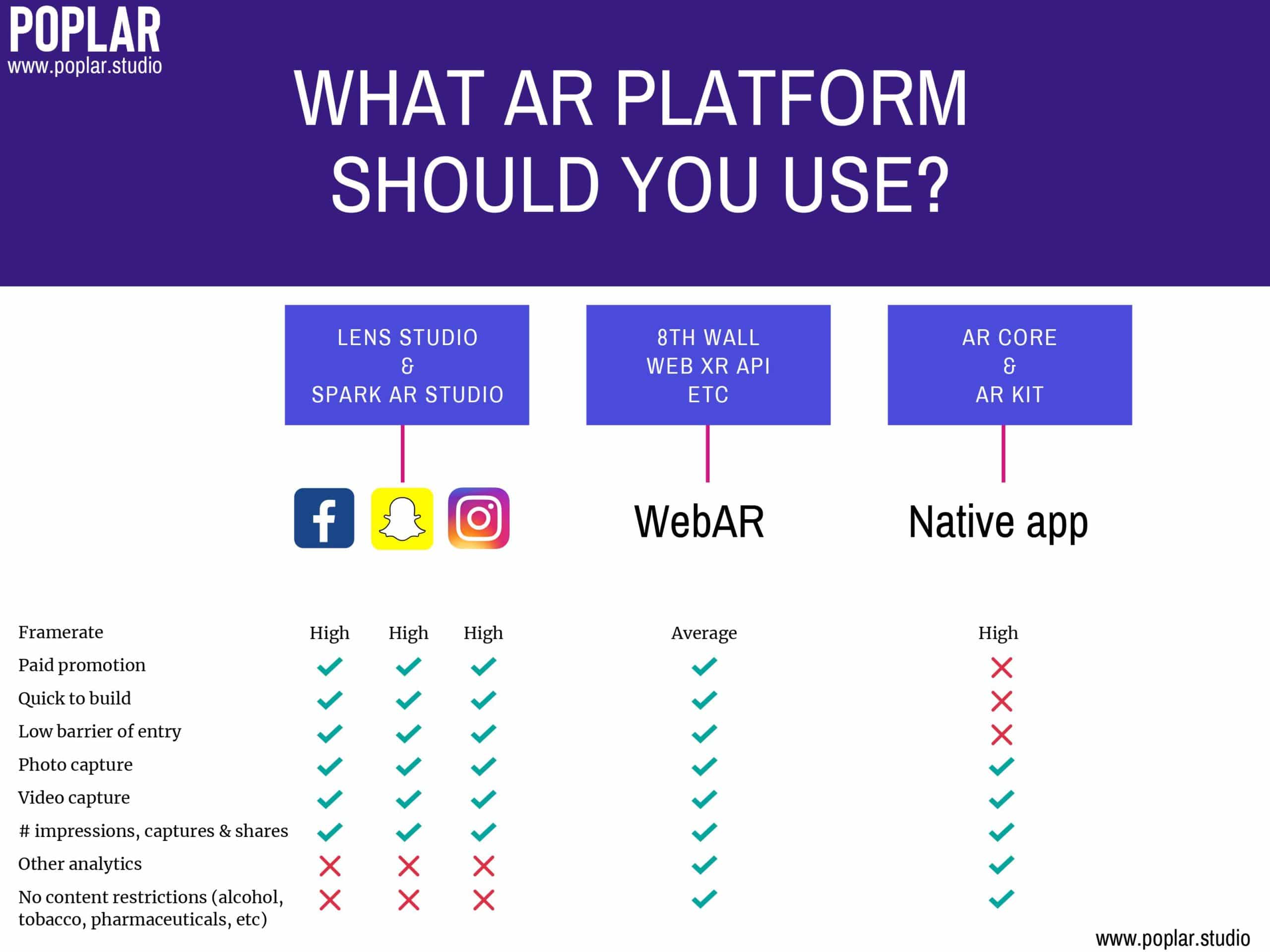

Moving on to qualitative analysis, mobile AR ad platforms’ pros and cons were outlined throughout this report in dedicated sections on the main players. But to boil that down, how do they stack up? AR ad agency Poplar put together a chart to answer this question (see below).

Specifically, when choosing an AR ad platform, considerations include capacity for organic discovery, paid promotion, developer skills required, and lens capabilities. At a high level, these factors stack up evenly among social AR platforms but deviate from web AR.

Specifically, social platforms excel in organic discovery. Built-in social graphs and media-sharing create that advantage. But they fall short in advanced campaign analytics when compared to web AR, where you can utilize tools like Google Analytics to track performance.

Social channels also fall short in being able to advertise certain products like alcohol. Indeed, web AR has become a go-to channel for AR campaigns for spirits brands, which we’ll cover in Part II of this report series that will do a dive deep on several AR advertising case studies.

Numbers Game

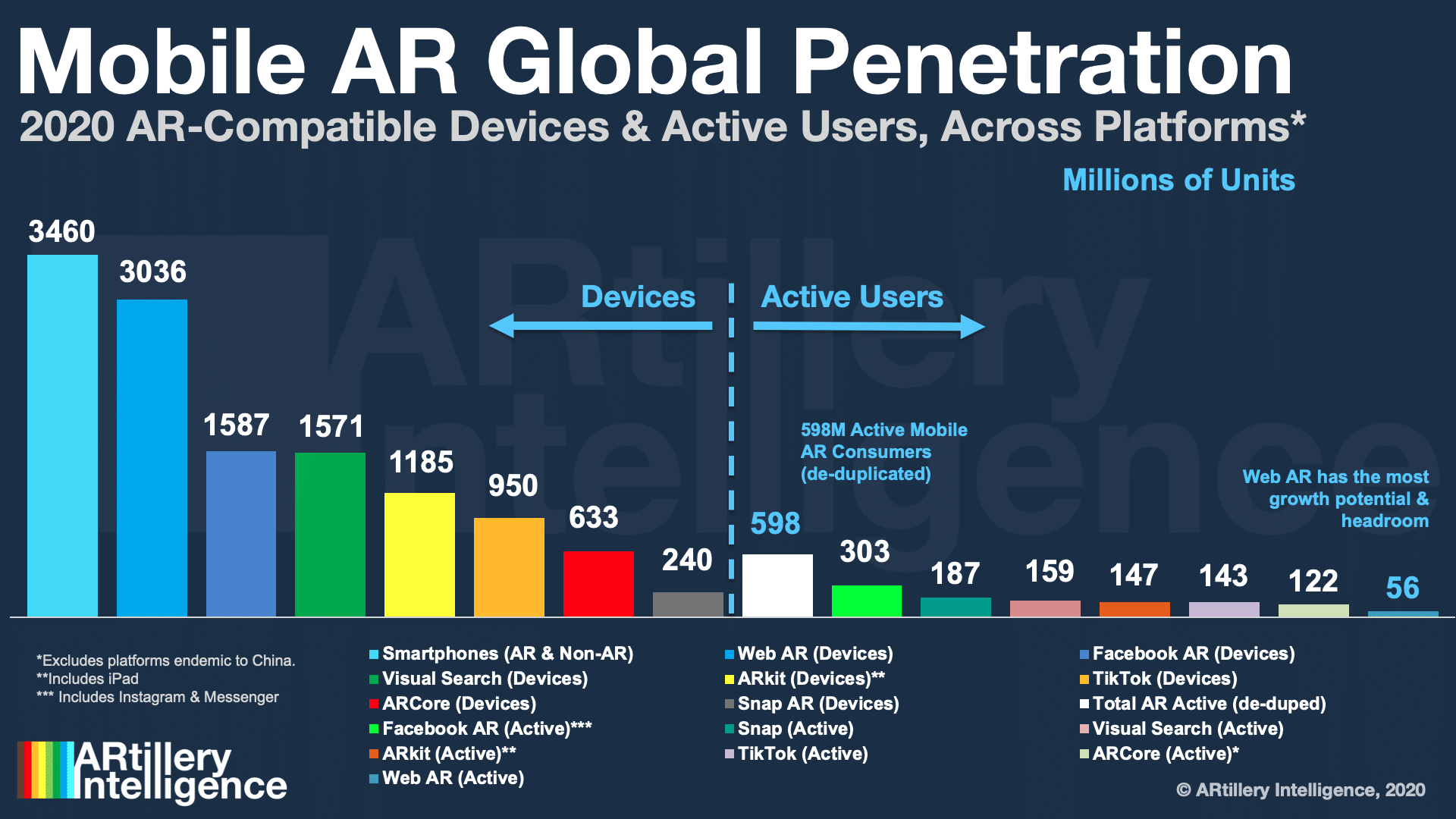

Web AR may have another advantage: platform reach. One way to compare AR platforms and their comparative advertising reach is to look at installed bases. ARtillery Intelligence recently performed this exercise including compatible hardware bases and active users (see below).

Among these platforms, web AR has the biggest growth capacity given that it has the greatest device compatibility. But it has the least active users. Along with web AR’s technical and practical benefits, this headroom – though active use is low today – could be a positive sign for its future.

Furthermore, this mobile AR market-sizing exercise reveals another factor: platform fragmentation. Compared to the mature smartphone market that has two platforms, AR (and VR for that matter) have several, which could compel web AR and its cross-platform advantages.

“Magic Leap is building a software ecosystem around its product. Microsoft is doing the same with Hololens. Oculus, HTC and Playstation are doing it in VR,” said 8th Wall’s Erik Murphy-Chutorian. “But it may be that if there is no dedicated winner, the winner becomes something that works across all of them.”