Several signals validate that AR can bring considerable value to consumer-facing brands. That includes demonstrating products more dimensionally and creating advertising that’s more interactive and engaging. And the numbers speak for themselves in campaign results.

But such results and case studies come from a vocal minority of brand marketers. There’s still ample growth and penetration to come for the rest of the pack. Meanwhile, barriers to adoption loom large, including natural resistance to change among habit-bound brand marketers.

To gauge AR’s potential in making it through these organizational hurdles, it’s often a matter of taking the temperature of any given organization. That can often reveal signals that help determine if AR will or won’t “stick the landing” at a given company, and in the aggregate.

With that backdrop, Perkins Coie has been running its XR Industry Insider surveys for the past few years to get this temperature reading. Its latest edition was fielded in July to 164 enterprises across industries about AR sentiments, and is the focus of this week’s Data Dive.

Highlight Reel

Diving right into the data, here’s our highlight reel from the report.

– 83 percent of enterprise respondents say that investment in immersive technology will increase this year, up from 68 percent who expressed the same sentiment in 2020.

– 65 percent said that user experience has the most influence on consumer engagement with AR and VR, followed by content breadth/quality (53 percent) and cost (27 percent).

— Given that most mobile AR experiences are free (e.g. social lenses), cost concerns presumably lie with VR adoption (requisite hardware, etc.).

– 64 percent said that consumers don’t understand AR, or are unaware of where to find it. 54 percent said that developers don’t fully understand how to create compelling consumer experiences.

– Bridging this consumer/developer gap will be a critical AR success factor in the coming years, and more education, research and insights are needed on both ends.

– When asked about top factors that will boost AR brand adoption, 50 percent believe that more accessible software is needed accross the enterprise. 44 percent believe more infrastructure is needed to use and collaborate with AR.

– In all cases, the above sentiment speaks to the need for AR creation and distribution tools that can be used by non-technical folks such as marketing departments.

– 34 percent believe that – outside of gaming and entertainment – healthcare has seen the most adoption of immersive tech during the pandemic, followed by marketing and advertising (31 percent).

– Marketing and advertising saw the greatest year-over-year growth on this particular meeasure, growing from 16 percent in 2020.

– Looking forward to the post-Covid era, 45 percent believe that education will fare best in terms of immersive tech adoption, followed by automotive (42 percent) and retail/eCommerce (35 percent).

– 89 percent believe that fashion and retail are prime verticals for immersive tech.

– 73 percent of those respondents believe that the most valuable use case is virtual merchandise tryons, followed by product customization (63 percent) and advertising (42 percent).

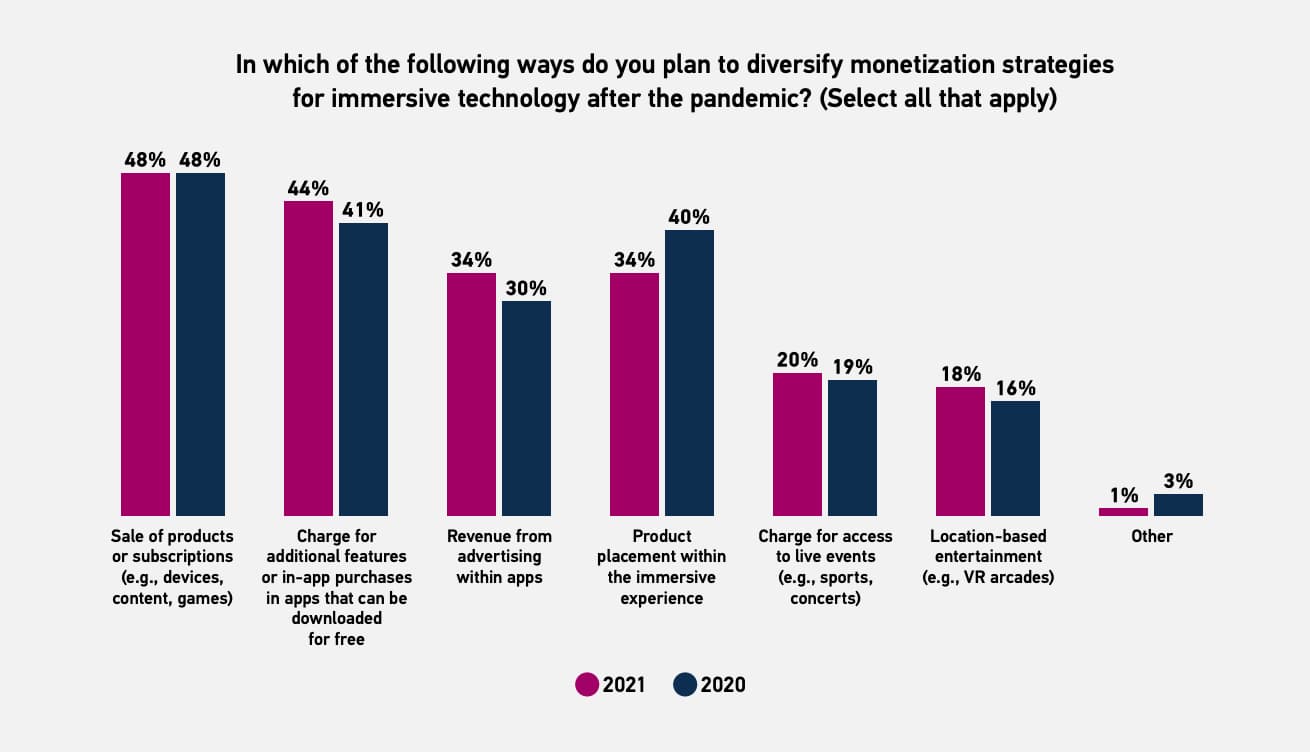

– As for post-Covid AR monetization strategies, 48 percent favor premium software/content sales and subscriptions, followed by in-app purchases (44 percent), and ad revenue (34 percent).

Open Question

Speaking of monetization, revenue models are still an open question. More accurately, it depends on the AR or VR modality in question. For example, in-app purchases rule mobile AR gaming while advertising rules social AR lenses, and premium/paid content rules VR.

Breaking each of these down, in-app purchases (IAP) have been validated by Pokémon Go (and our data). IAP is fitting to the game as it inherits consumer habits from the broader mobile gaming world. And it lets AR’s non-proven status ease its way to users’ wallets.

As for advertising, it’s fitting to social lenses for similar reasons – AR is too early and unproven to get users to pay for it. Moreover, AR lenses fall with the category of entertainment and social media, which have a concrete precedent set – among users and brands – for ad support.

Finally, VR likewise inherits the business models of the media categories from which it stems. That includes console gaming, where the prevailing business model is premium purchases. However, that could change, as free/ad-supported content could help VR scale to the masses.

All of the above will continue to evolve as these formats grow into their own skin. But if there’s one discernable pattern in the previous few paragraphs, it’s that immersive tech will gain the most traction where and when it inherits comfort levels and payment structures of its forbears.