AR continues to evolve and take shape. Like other tech sectors, it has spawned several sub-sectors that comprise an ecosystem. These include industrial AR, consumer VR, and AR shopping. Existing alongside all of them – and overlapping to some degree – is AR marketing.

Among other things, AR marketing includes sponsored AR lenses that let consumers visualize products in their space. This field – including AR creation tools and ad placement – could grow from $2.78 billion last year to $9.85 billion by 2026 according to ARtillery Intelligence.

Factors propelling this growth include brand advertisers’ escalating affinity for, and recognition of, AR’s potential. More practically speaking, there’s a real business case. AR marketing campaigns continue to show strong performance metrics when compared with 2D benchmarks.

But how is this coming together? And what are best practices? These questions were tackled in a recent report by ARtillery Intelligence, containing narrative analysis, revenue projections, and campaign case studies. It joins our report excerpt series, with the latest below.

The Landscape

Picking up where we left off in last week’s report excerpt, who are the biggest players in AR marketing? Snap holds a leading position given its focus and ethos as a “camera company.” Meta is also formidable given the global scale of increasingly AR-infused apps like Instagram.

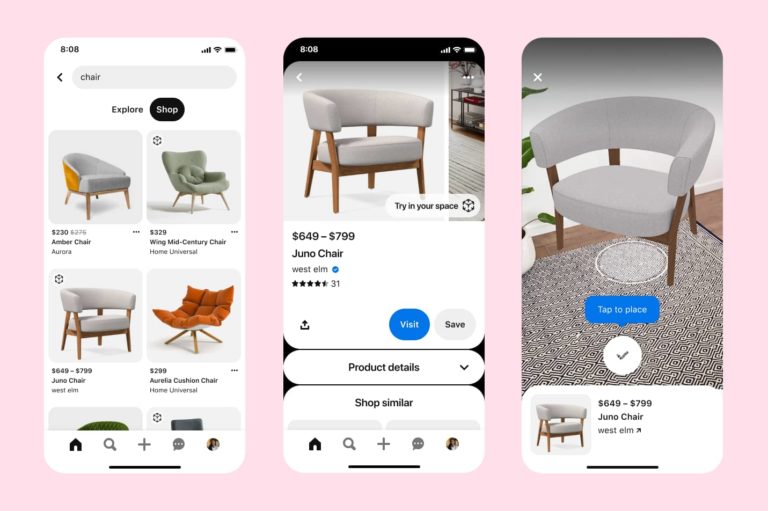

Instagram could actually be AR’s sleeping giant. Not only has it incorporated AR by opening it up to Meta’s Spark AR lens developer platform, but it’s natively aligned with visual shopping. Pre-dating AR, it has cultivated a use case for shopping and product discovery in fashion and food.

Instagram is also increasingly transactional with integrated buy buttons. With AR, that shopping use case is given more dimension through interactive try-ons. This is a powerful combination that continues to attract ad dollars to promote and amplify branded AR experiences.

Speaking of powerful combinations, AR recently collided with the world’s largest online commerce giant. We’re talking of course about Amazon, which has erstwhile slow-walked its AR integrations. But is its latest shoe-try-on feature a sign of a larger visual shopping blitz to come?

And let’s not forget TikTok, which may be the real AR sleeping giant. It has massive global scale but underdeveloped AR… until recently. Its new AR creator platform, Effect House, could let it scale in the same way that creator platforms caused Snap and Meta’s AR efforts to inflect.

History Repeats

Meanwhile, other players loom. Social lenses are the most prevalent form of AR today, but visual search could eventually be a more powerful AR modality. It lets consumers hold up their phones for descriptive overlays to contextualize (or buy) products they see in the real world.

Building from the high-intent qualities of web search, this could be a true utility as it develops from Google, Pinterest, Snap, and others. Google is particularly motivated to develop visual search apps like Google Lens to future-proof its core businesses through additional inputs.

So when you boil it down, the two main AR marketing tracks are AR visualization (placing a 3D product in your space), and visual search (using the camera to identify real-world objects). That makes AR map to the main divisions in the broader digital advertising world: display and search.

In fact, when looking AR marketing’s growth it could follow an evolutionary path similar to display and search ads online. Display was out of the gate first as an ad format (just like lenses lead today), before search developed as a more technically-nuanced and lucrative ad format.

Could AR marketing develop in similar ways? We’ll pick it up there in the next installment of this series…