Like many analyst firms, market sizing is one of the ongoing practices of AR Insider’s research arm ARtillery Intelligence. A few times per year, it goes into isolation and buries itself deep in financial modeling. The latest such exercise zeroes in on mobile AR revenues.

This takes the insights and observations accumulated throughout the year and synthesizes them into hard numbers for spatial computing (see methodology and inclusions/exclusions). It’s all about an extensive forecast model coupled with rigor in assembling reliable inputs.

So what did the latest forecast uncover? At a high level, global mobile AR revenue is projected to grow from $12.45 billion in 2021 to $36.26 billion in 2026, a 23.8 percent CAGR. This sum consists of mobile AR consumer and enterprise spending and their revenue subsegments.

Drilling down, our latest Behind the Numbers installment looks specifically at the mobile AR hardware base. How many devices are AR-compatible? How many of those represent active AR users? And how does that lay the foundation for the above revenue growth?

Confidence Signal

One confidence signal for mobile AR is the sheer size of the smartphone installed base. Compared to the uphill battle that AR glasses face, mobile AR — though challenged in its own ways — has an easier climb due to “zero-cost” hardware (the device you already own).

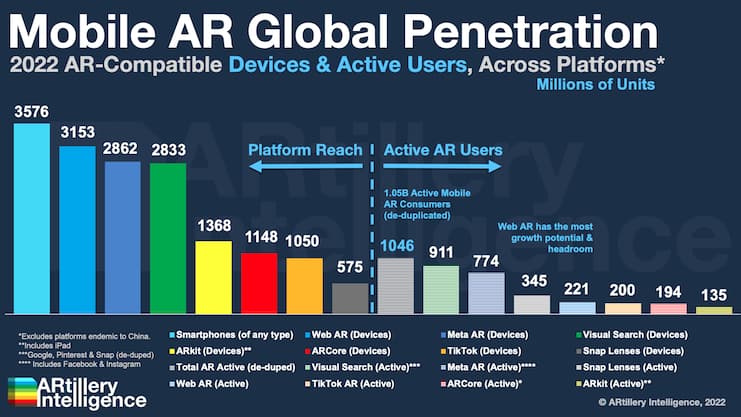

But more important than the overall smartphone base is the growing share of that universe that’s AR-compatible. Given platform fragmentation (see below), the size of that universe can best be framed by its biggest channel, web AR, which has 3.15 billion AR-compatible devices.

As for the other platforms on that list, Meta’s Spark AR is estimated to have 2.86 billion AR-compatible smartphones, followed by ARkit (1.37 billion), TikTok (1.05 billion), ARCore (1.15 billion), and Snap (575 million). Visual search (e.g., Google Lens) operates on 2.8 billion devices.

But more important than AR compatibility (a.k.a., installed base) is active use. There, the estimate is 1.05 billion by the end of this year growing to 1.67 billion by 2026. These figures count AR users who engage monthly or more and are de-duplicated, given several platforms.

Camera Native

One question that arises from the above is how AR active users have broken the one billion barrier. This is considerable, given that it’s roughly 1/7th of the world’s population. Anecdotal evidence or a “gut check” doesn’t necessarily support that much AR usage seen around us.

One reason for the usage volume is visual search. This includes tools such as Google Lens, Pinterest Lens and Snap Scan, which let users hold up their phones to identify real-world items. It’s a growing use case for both general-interest searches as well as (monetizable) shopping.

Supporting that are recent disclosures from Google that it’s now seeing 8 billion visual searches per month, which is 2.5x year-over-year growth. This informed estimates in ARtillery’s forecast that visual search users are 911 million globally – exceeding all other platforms above.

Generally speaking, visual search checks all the boxes for a potential killer app. It’s a utility with an inherently frequent use case (just like web search). It takes that familiar web search use case and makes it more visual, which resonates with camera-native Millennials and Gen-Z.

Compatibility & Correlation

Synthesizing the above two sections – AR compatibility and active use – it’s notable that there isn’t necessarily a correlation between the two. For example, web AR leads in compatibility but trails in active use. That gap is a mark of growth potential and ample headroom.

TikTok is in a similar boat with promising reach, but its AR play is just getting started. Snap Lenses conversely have the lowest compatibility among platforms (575 million) but the highest active monthly use (345 million). This gives it the greatest ratio of AR usage among platforms.

Facebook sits somewhere in the middle with a diversified AR approach (News Feed, Instagram, Messenger). Instagram could be the real ace up its sleeve given a cultural match with camera-forward users, and natural monetization with its product-discovery use case.

Lastly, back to visual search, its inclusion of Google Lens, Pinterest Lens, Snap Scan, and others gives it the leading position among active users. For the reasons explored above, it could be AR’s real sleeping giant in its potential traction and ability to unlock camera commerce.

We’ll pause there and circle back in the next Behind the Numbers installment with more findings from this forecast. Meanwhile, see the entire thing here.