This post was contributed by Kristie Cu, business strategist and VR/AR lead at Orange Silicon Valley.

Where AR and VR Stand in 2017 After a Dizzying Wave of Hype

By Kristie Cu

Virtual reality headsets are not hard to find in 2017. Just take a look at the next big conference you attend; you’ll likely find some type of Oculus or Vive demo. Visiting a newsstand? You’ll likely be able to find a free Cardboard in a magazine, covered with someone’s promotional branding. Visiting a sports stadium? You’ll probably find VR demos there as well.

You’ve probably tried one or more of these VR or augmented reality demos. Why? Because we saw how much smartphones changed the world, and the future of tech seems even more promising. But now you’ve tried it — were you blown away? Do you immediately want to buy a high-end headset? Desktop hardware? More games? Controllers?

Using technology as a shiny promotional tool can work when it’s nascent; everyone wants a taste. But, when someone gets a mediocre-at-best first taste, it can be hard to convince that user to return. VR and AR can be used as gimmicks, but they can also be so much more. That’s why VR/AR still needs a successful and robust market introduction to fully deliver on the platforms’ promise.

While we haven’t seen shockingly wide-spread adoption, there is still reason to be optimistic — about AR, VR, and the evolution of both industries as we see new applications unfold.

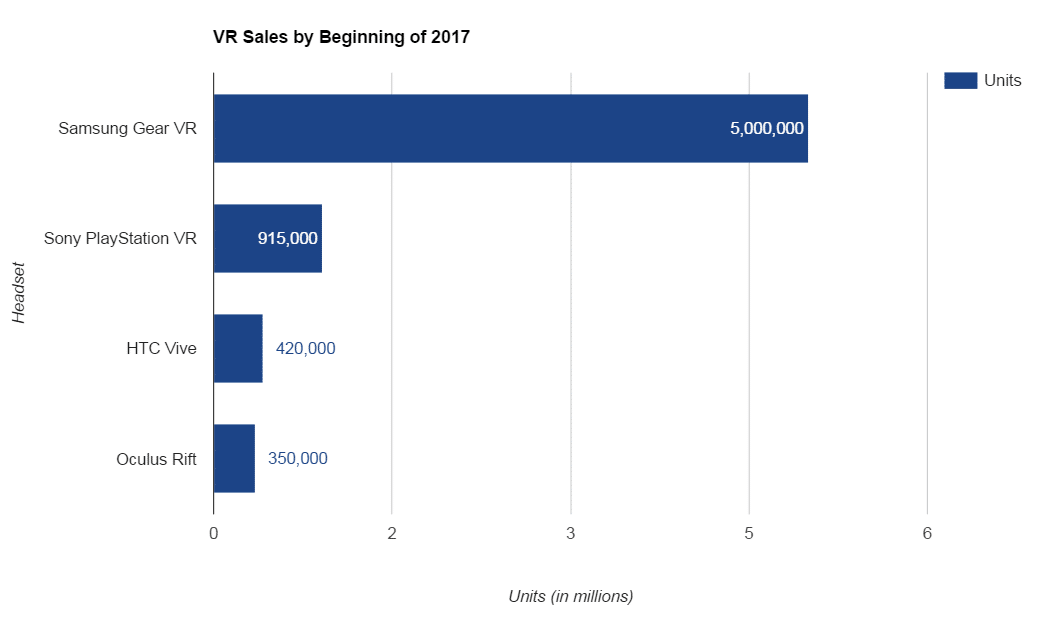

Here are some positive highlights: Early statistics show strong potential for VR/AR market size. The few numbers that we have point to a growing, promising industry — to date, approximately 5 million Samsung Gear VR’s, 915K Playstation VR units, 420K HTC Vive headesets, and 350K Oculus Riftshave been sold. Meanwhile, a reported $2.3 billion in venture capital has been deployed into AR/VR. We also know global smartphone is at all-time highs, which could be viewed as additional addressable market, a whopping 2 billion+ people who could be using mobile VR — which will of course depend upon successful mobile hardware and software.

Sources: Samsung, Sony, SuperData Research

What’s to come has constantly been the story of the slower, but larger market of AR within the enterprise. A topic perhaps less visible to consumers, but extremely powerful and potentially enabled by some of the VR technologies that exist today. Beyond the fact that the forecasted addressable market is large, few AR headsets are available, and early signs point to a need to attract more developers and wait. Larger corporations are just getting started, with many focusing on illustrating ROI through proof of concepts.

Corporations, VCs and angels alike are investing in the opportunity to see new means of productivity and entertainment to come of both AR and VR. A surge in the number of VR/AR focused funds indicates high interest and enthusiasm in the market, including funds like Virtual Reality Venture Capital Alliance (VRVCA), Presence Capital, The Venture Reality Fund, Colopl and corporate groups like HTC, Comcast Ventures, Qualcomm Ventures, Intel Capital, and Google Ventures.

So far, some early investments results have been mixed, but some positive signals have emerged in early 2017. Corporations continue to indicate strong interest in the AR/VR markets, and I have compiled a timeline of the most noteworthy moves this quarter.

While market signals are still waiting to mature, corporations continue to push forward. Samsung will push forward with a $150 million fund that will in part target young VR startups. HTC announced its own new push in the mobile VR arena, and its Vive headsets will feature prominently in IMAX’s new VR theater in Los Angeles. HTC appears to be confronting challenges shared by Facebook’s Oculus division, rolling out new financing plans to make its Vives accessible to a wider audience. That move echoed the Mar. 1 Oculus announcement that its headset prices would be cut from $499 to $399.

What’s clear is that the value from this emerging technology is indeed promising, but that the precise value is still being determined — puzzle pieces are constantly in flux: from the hardware itself, to business models and pricing, to content and strategic partnerships. Thus, as all players seek to establish themselves as first-market-movers, their decisions should be fueled not only by short-term value, but also by long-term customer value as well.

Kristie Cu is a business strategist focused on corporate strategy, virtual reality, augmented reality, deal sourcing, and partnerships at Orange Silicon Valley.

Kristie Cu is a business strategist focused on corporate strategy, virtual reality, augmented reality, deal sourcing, and partnerships at Orange Silicon Valley.