GearVR and PSVR continue to show signs of leading market share among VR headsets. This has been evident in our past calculations and validated in the latest ARtillry Intelligence Briefing: VR Usage & Consumer Attitudes.

Working closely with Thrive Analytics, ARtillry authored questions to be fielded through its established survey engine. This first wave of Virtual Reality Monitor™ (VRM) taps a sample of 2000 adults to reveal consumer behavior patterns that are examined throughout the report.

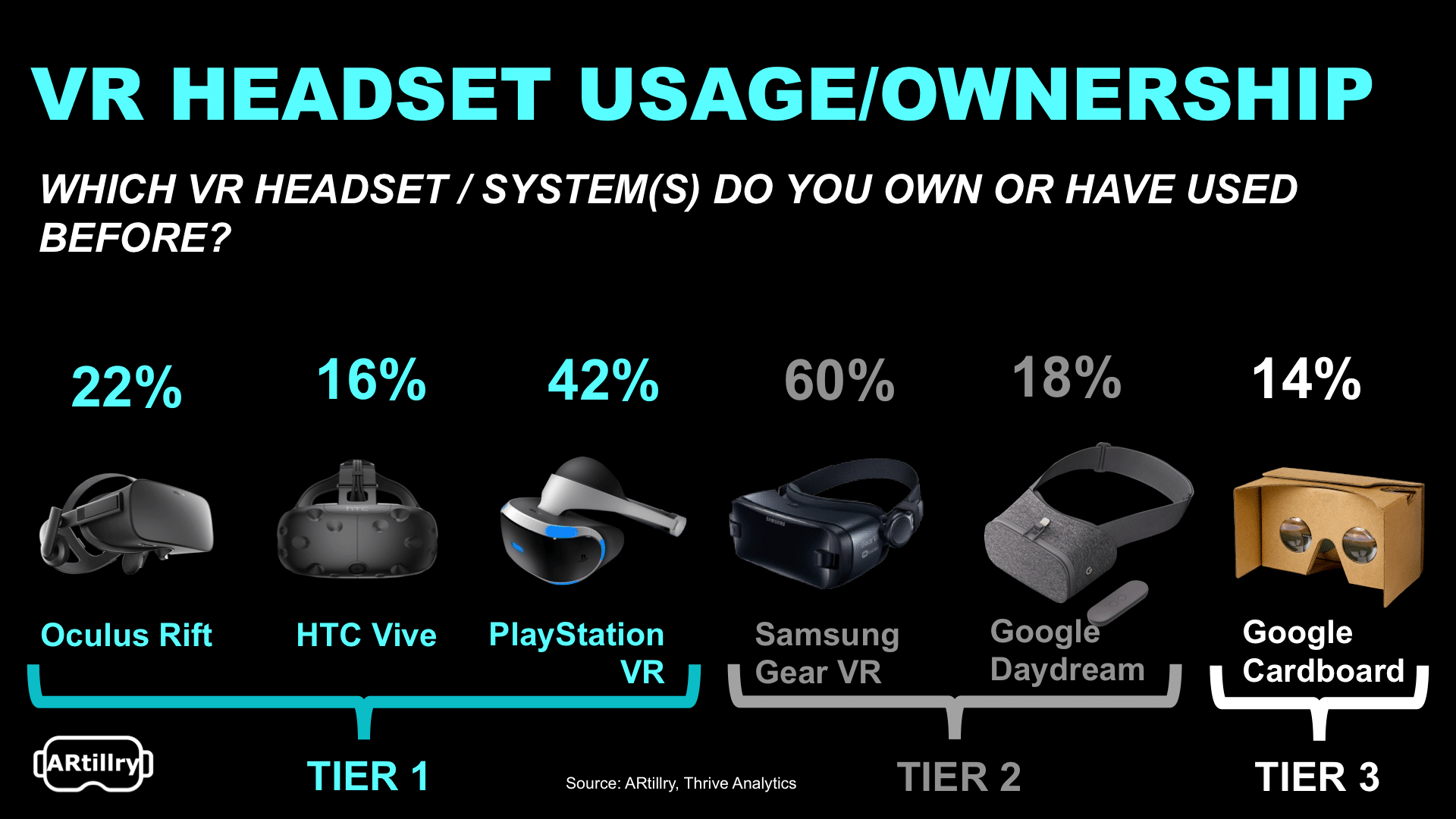

Part I. VR Ownership Sentiments

A good place to start examining VR usage is the breakdown of current ownership. The array of available devices and their relative adoption rates can be telling of features and attributes that resonate with consumers. That includes things like price, features and specifications.

With that backdrop, Samsung’s Gear VR headset showed the most prevalent ownership among Virtual Reality Monitor™ (VRM) respondents. This isn’t entirely surprising, due to its relatively low price ($129), and longer tenure in the marketplace relative to the comparable Google Daydream View.

Both devices are in Tier 2 of the VR headset spectrum, in terms of ARtillry’s market segmentation. The second highest ownership in VRM was Playstation VR (PSVR). This also comes as no surprise, given its compatibility with a large installed base (60 million) of PlayStation 4 (PS4) consoles.

PSVR sits in Tier 1, along with HTC Vive and Oculus Rift. The latter devices scored lower than PSVR for reported ownership, likely due to the need for a dedicated PC with high-end graphical processing. Though PSVR is inferior in specs like resolution, its “all-in” price is lower for existing PS4 owners.

Google Cardboard scored lowest in overall reported ownership, which does come as a surprise. The pricing barrier for the device is lowest of the pack, and in some cases non-existent due to promotional giveaways. Therefore, low reported ownership is likely due to a less compelling user experience or anomaly in the survey.

Altogether, one lesson is that VR owners are willing to pay for quality… but only to a point. Cardboard is cheapest, yet it has the lowest penetration. Meanwhile, PSVR’s higher-end Tier-1 experience is attractive, but also “good enough,” versus the more capable and expensive Rift and Vive.

Another conclusion is that marketplace standards and expectations for VR are optimized at the PSVR’s level. That’s the sweet spot in terms of price and features.

Up Next: Headset Satisfaction Levels.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.