The mobile OS wars between iOS and Android have occupied much of the past ten years. They reached varying levels of intensity in early days of competition over market share, but have matured a bit over the past few years.

Now a component of those operating systems could reignite the competition: their respective AR development kits. More importantly, ARkit and ARCore carry their parents’ DNA and their positioning in the smartphone era. For Apple, it’s all about apps. For Google, the web.

But the question is which AR platform is positioned better for growth and market share? It won’t be a winner take all market, just as iOS and Android have coexisted for years. And there is evidence that they’ll have some compatibility, or at least portability of graphical assets.

But they’ll still compete on many levels, and there are signals that indicate competitive differentiation on both sides. Google has greater scale and a technical lead from years invested in Tango. But Apple has more control over the hardware in its classic vertical integration.

Putting aside a technical analysis of each platform for now, how are these two mobile platforms and their AR toolkits positioned, and how do they stack up on strategic levels?

Google’s DNA (web) vs. apple’s DNA (apps) is mirrored in ARCore vs. ARkit. @mattmiesnieks @shelisrael @AppleARWorld https://t.co/03nyQPgCRE

— AR Insider (@ArInsider) August 30, 2017

App Fatigue

Starting with the Google, it has spent 15 years as the world’s search engine, including building a knowledge graph and search index. This will play into an AR strategy through “WebAR” in which users don’t have to download apps, but rather visit mobile websites to summon AR experiences.

This of course contrasts with Apple’s content architecture that’s rooted in apps. There is some evidence that an app-centric approach to AR could be disadvantaged, due to user friction. Indeed, we’ve hit peak app-fatigue in general, given that most consumers’ monthly install rate is… zero.

“You effectively have all the same problems that a mobile app has,” Presence Capital partner Amitt Mahajan told ARtillry recently. “You have to convince someone to download it, convince them to come back every day. All of the friction to get to that experience is still pretty high.”

Beyond friction for users, apps are disadvantaged by their lack of interoperability compared to the link-structured web. This has always been the case in the app era, leading to movements like deep linking, but it could really handicap AR functionality by forcing it into non-linked silos.

As for where ARkit could be advantaged, it has a head start in developers’ invested time, as well as some technical differentiation. But the lifespan of AR will eventually negate Apple’s three-month head start. Greater developer attraction will ultimately come from platform reach.

The Web has a chance to crack open the App Store duopoly as we move to AR & VR. "Apps" don't make sense in AR, but linking "things" does.. https://t.co/Nk3fuq0O1U

— Matt Miesnieks (@mattmiesnieks) August 29, 2017

By the Numbers

Though Apple has a near-term advantage in the installed base of ARkit-compatible iPhones (380 million), one hardware replacement cycle (2.5 years) will give most smartphones AR-compatible optics and processing. And the overall Android universe exceeds iOS by 2 billion global units.

On the other hand, Apple is advantaged by a unified product line. There are fewer devices, most of which run current or fairly recent iOS versions. That compares to the Android world, fragmented into several phones that rarely run the latest OS. That could create some compatibility hiccups.

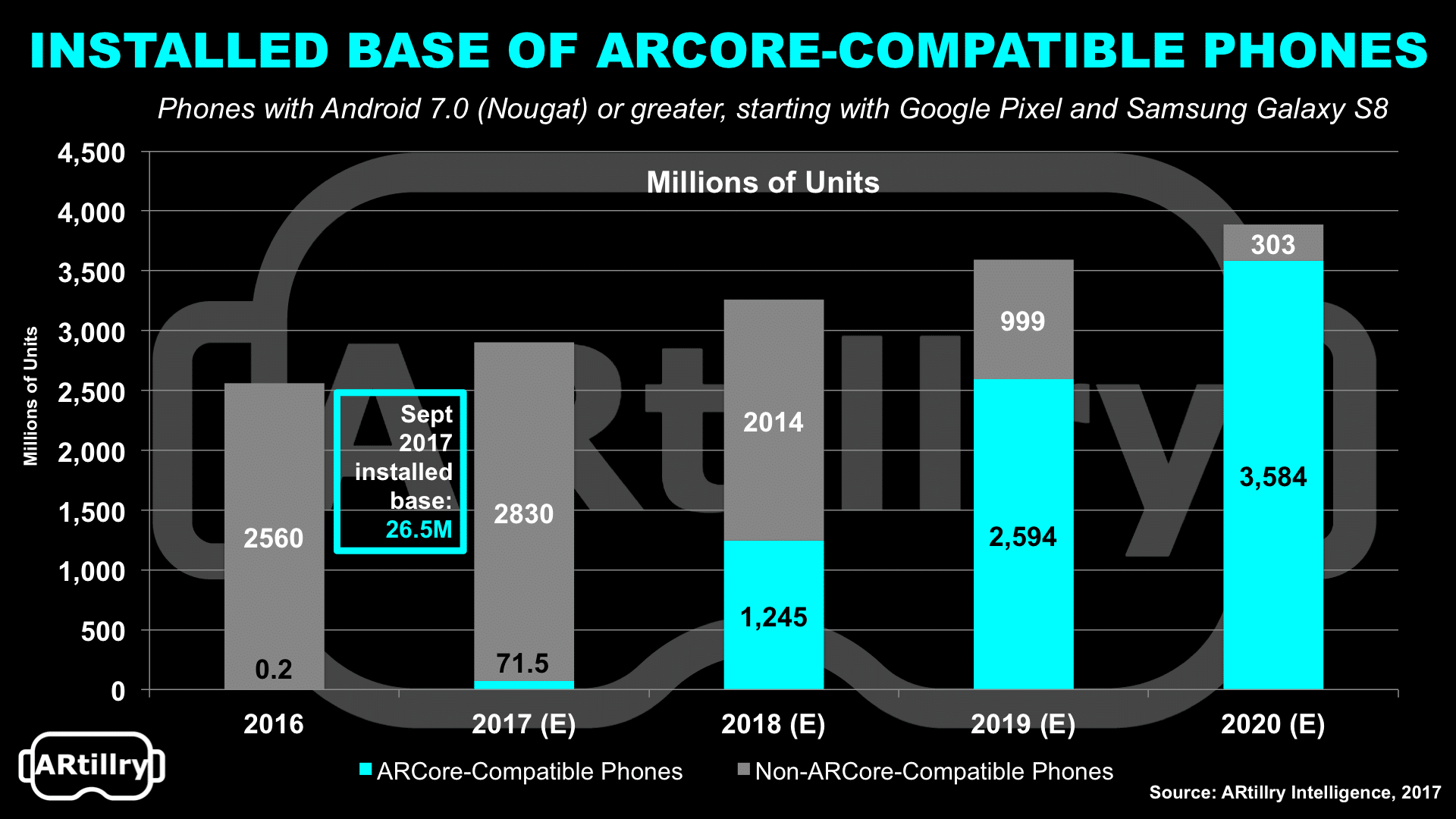

But ultimately, ARCore will pull ahead in sheer volume of its installed base. As we examined last week, it will reach 3.6 billion Android devices by 2020. This compatibility will start slow but grow fast, as newer hardware cycles into the Android universe.

As for ARkit’s head start in developer interest and early apps, though technically superior it could be challenged by ARCore’s flexibility and openness. Importing graphical assets will be easier including those created in Unity (also works with ARkit), Unreal, Tilt Brush and Google Blocks.

This provides another theoretical benefit to Google. The immersive computing assets it has assembled are more extensive and tenured than Apple. AR chops flow from Tango, while Google Lens will assist in object recognition and Tilt Brush & Blocks could democratize AR app creation.

Virtuous Cycle

As for next steps, Google is lining up OEM partners like Huawei, Asus and LG. That should help it reach it’s 100-million device goal ARCore launches. It hasn’t disclosed a launch date but we’re predicting sometime in Q1 2018, which is baked into our ARCore projections above.

Regardless of platform, we see the escalating hundreds of millions of devices that are compatible with ARkit and ARcore as a big incentive for developers to build AR apps. Many of them will be lured from the less-expansive VR gaming world, bringing transferrable skills such as Unity.

It could play out like this: the installed base of devices attracts developers who are incentivized by a larger addressable market. That drives the content available on a given platform and thus its ongoing attractiveness to consumers who in turn boost the installed base: A virtuous cycle.

There is of course a lot more to these competitive dynamics and addressable market sizes, and we’re in the process of dissecting them for ARtillry’s next Intelligence Briefing. It will publish next week with a deeper dive on ARCore and ARkit, and their strategic implications.

See our market-sizing and forecasting credentials here.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.