Data Point of the Week is ARtillry’s weekly dive into data from around the XR universe. Spanning usage and market-sizing data, it’s meant to draw insights for XR players, or would-be entrants. To see an indexed archive of data briefs and slide bank, subscribe to ARtillry Pro.

Where do executives in the trenches of the AR and VR sectors believe that the industry is headed? At a high level it’s best described as cautiously optimistic when looking at VRX’s latest survey (n= 595) of XR insiders. The survey was fielded in anticipation for VRX 2018.

Before diving into the data, we should level set on the sample. Unlike the XRDC developer survey we examined last week or our own consumer surveys, this sample is XR providers of various stripes, who are indicating where their near term investments and priorities lie.

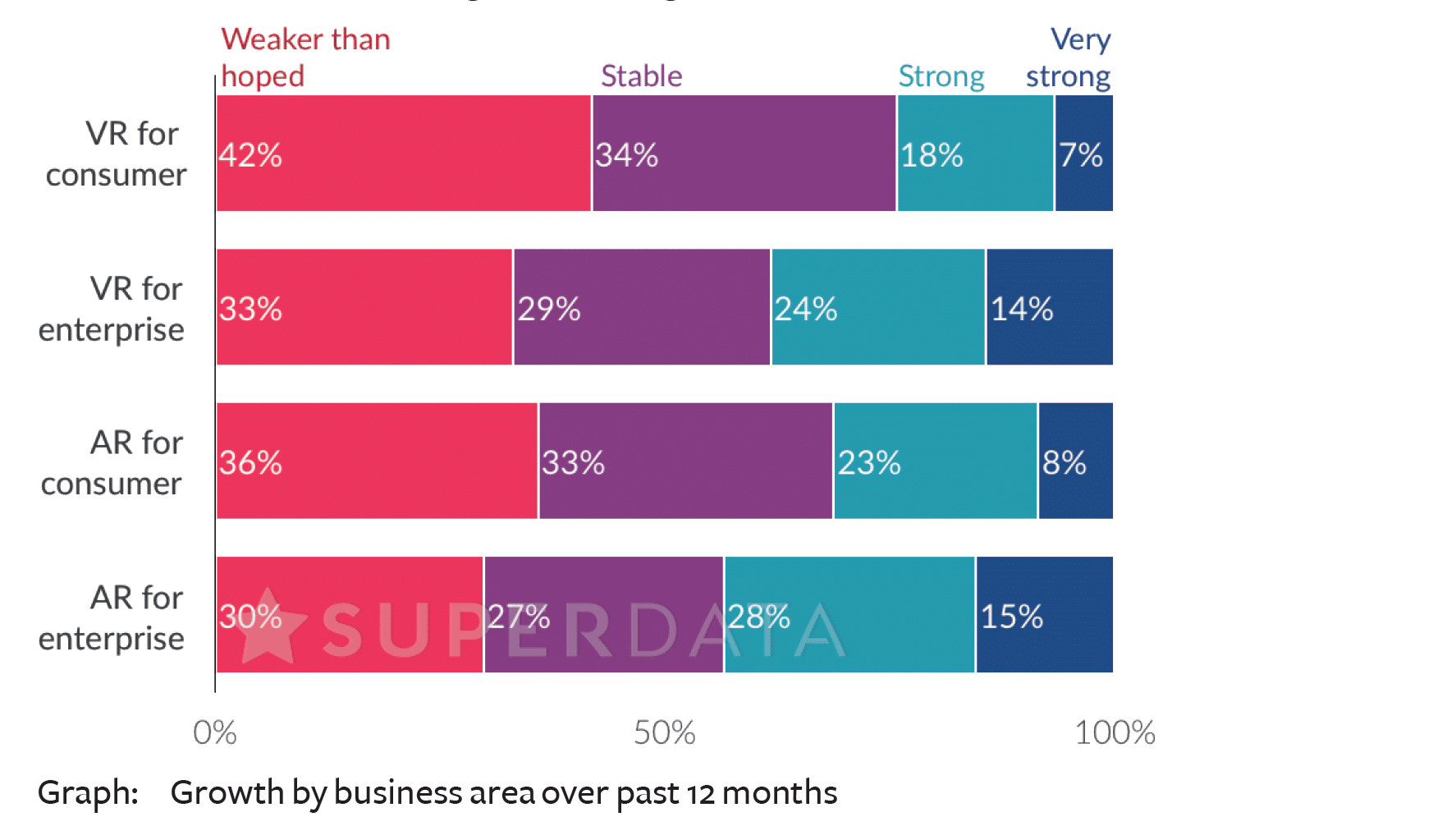

Overall, the cautious optimism comes in when looking at their viewpoint on XR’s trailing 12-month growth per sub-sector. Consumer VR had the least amount of positive associations, while enterprise AR had the most. This aligns with the conclusions of our latest forecast.

As for where survey respondents are placing their chips, that unsurprisingly mapped to their sentiments on recent growth. Again, enterprise AR scored highest while consumer VR scored low on this measure. Consumer AR scored lowest, despite its near-term scalability.

(click to expand)

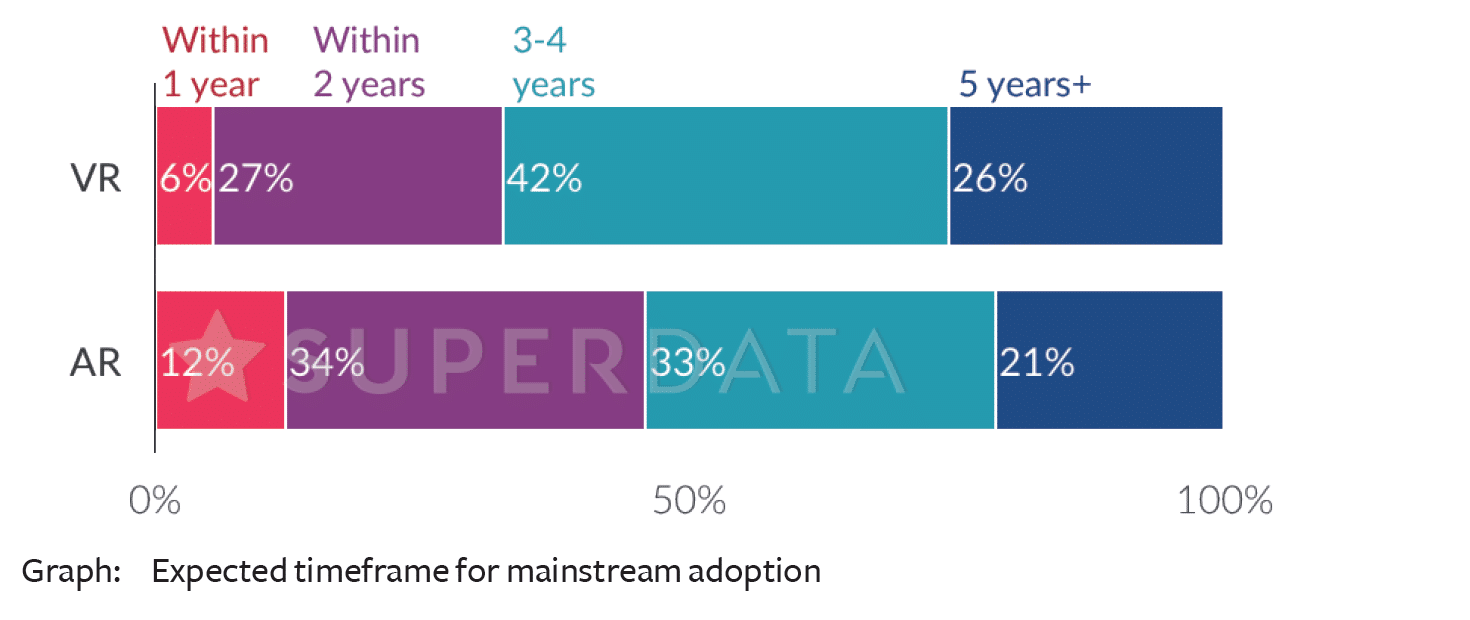

In terms of timeline to mainstream adoption, 46 percent believe AR’s window is within two years. That compares with 33 percent who believe VR’s window is within that same period. 26 percent believe VR is 5 or more years away compared with AR’s 21 percent.

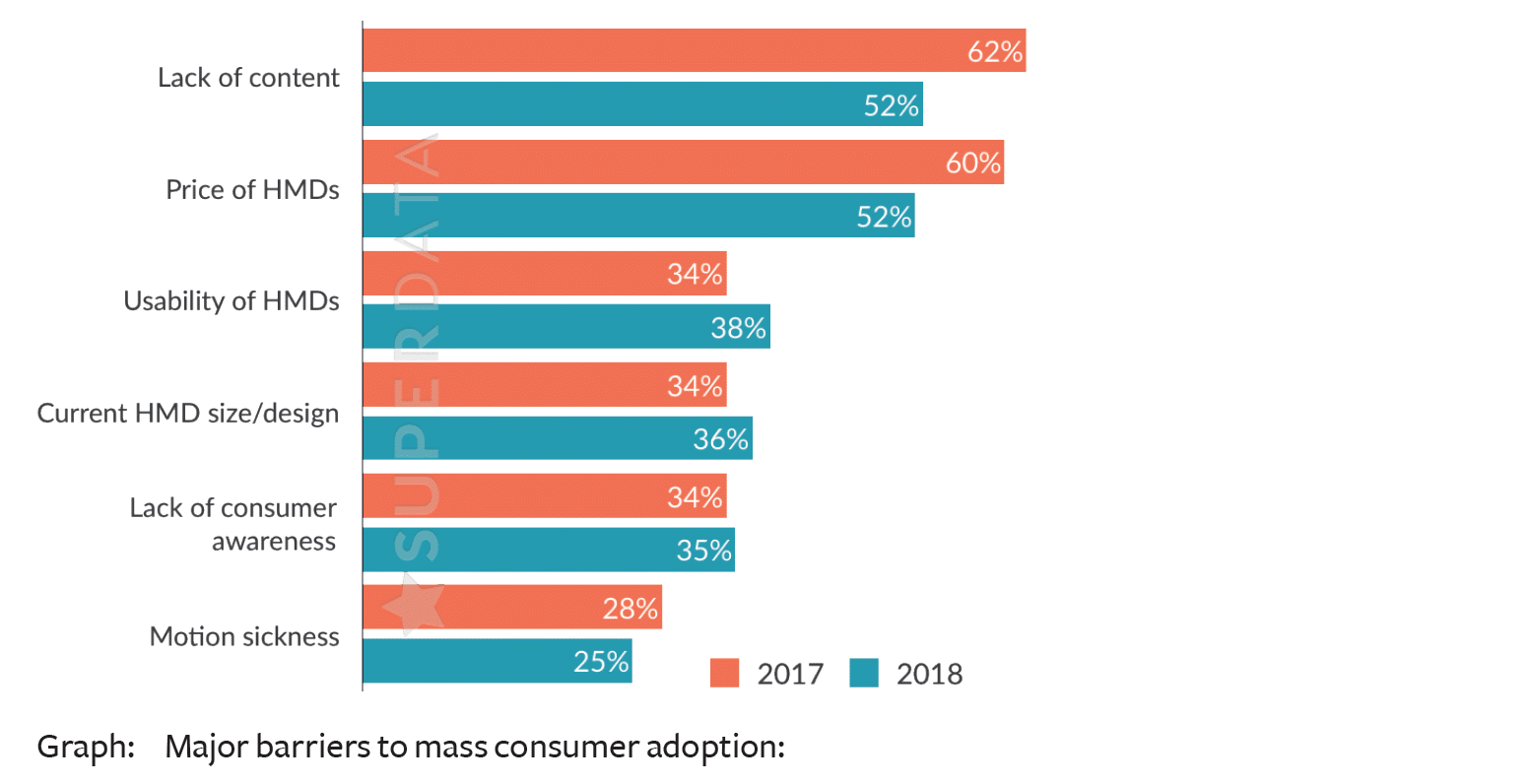

More importantly, the reasons for lack of adoption are telling of where product improvements are needed. And there we see similar sentiments from this “supply-side” survey as our “buy-side” consumer survey. Specifically, price and content are the biggest gating factors.

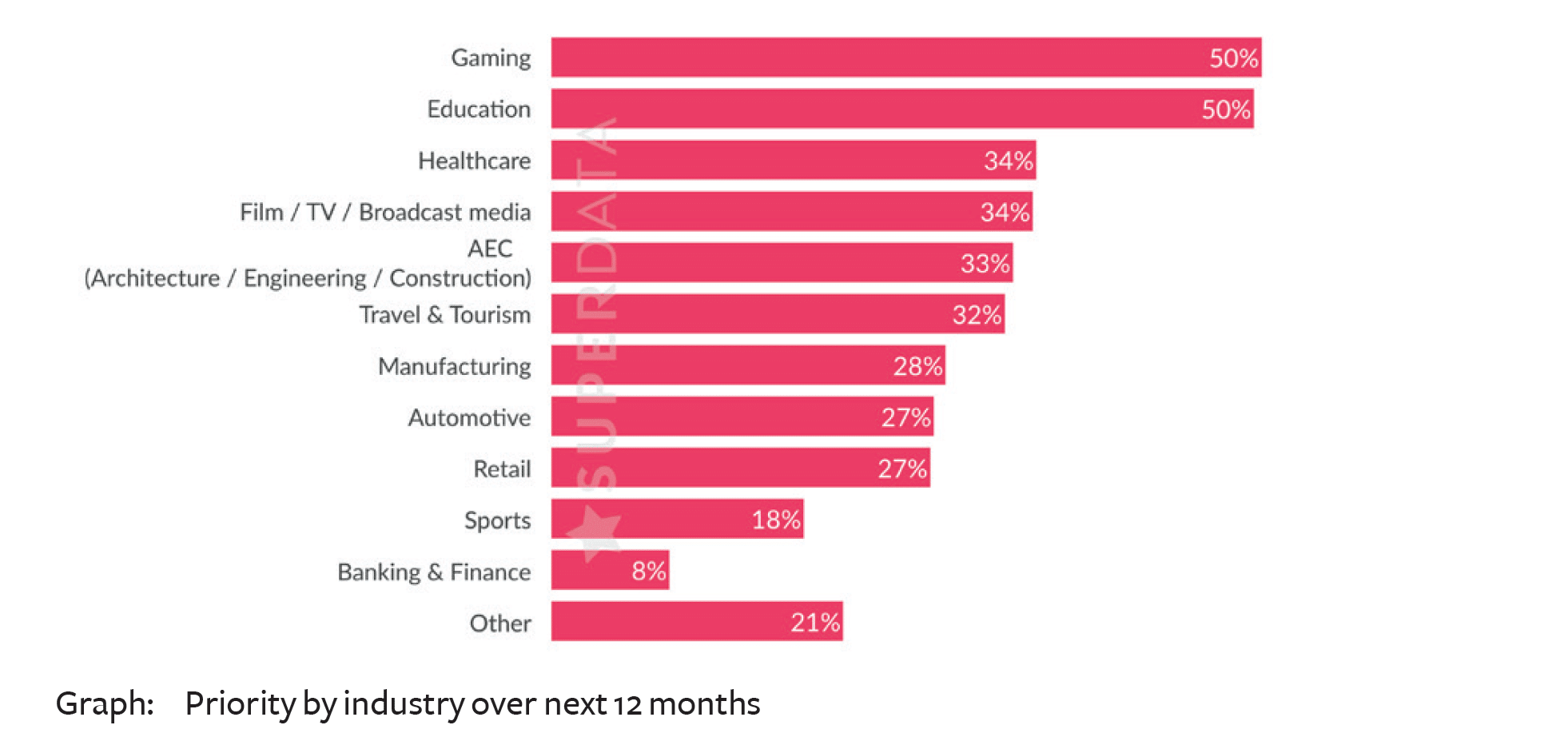

As for target markets, survey respondents are aiming for a mix of consumer and enterprise verticals. Gaming unsurprisingly scored highest (50%) tied with education. The latter is a double-edged sword, having a large addressable market but questionable spending power.

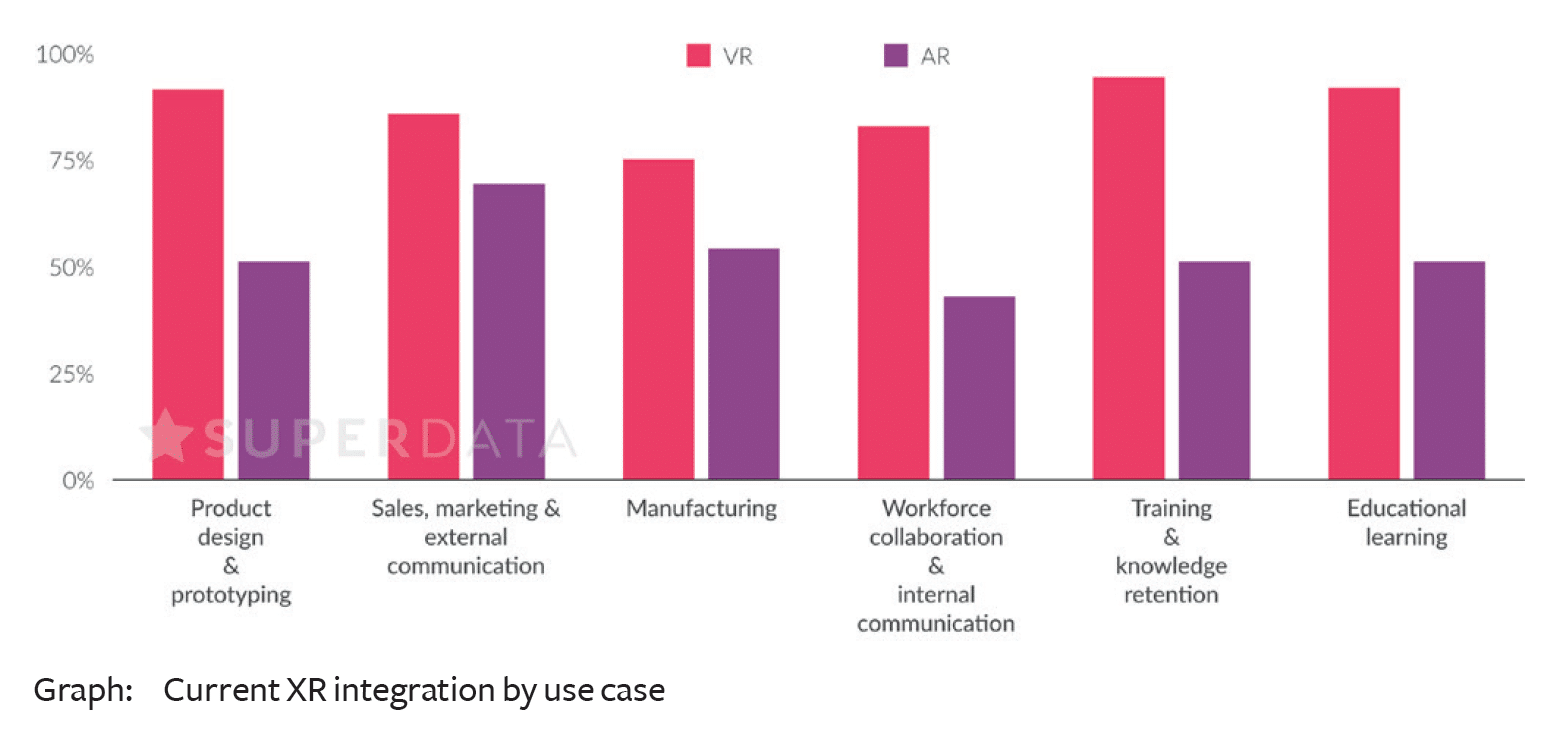

Drilling down from industry to business function, the most current usage for AR is in manufacturing and sales & marketing. VR is not-suprisingly most prevalent in educational learning, training and product design — functions conducive to VR’s full immersion.

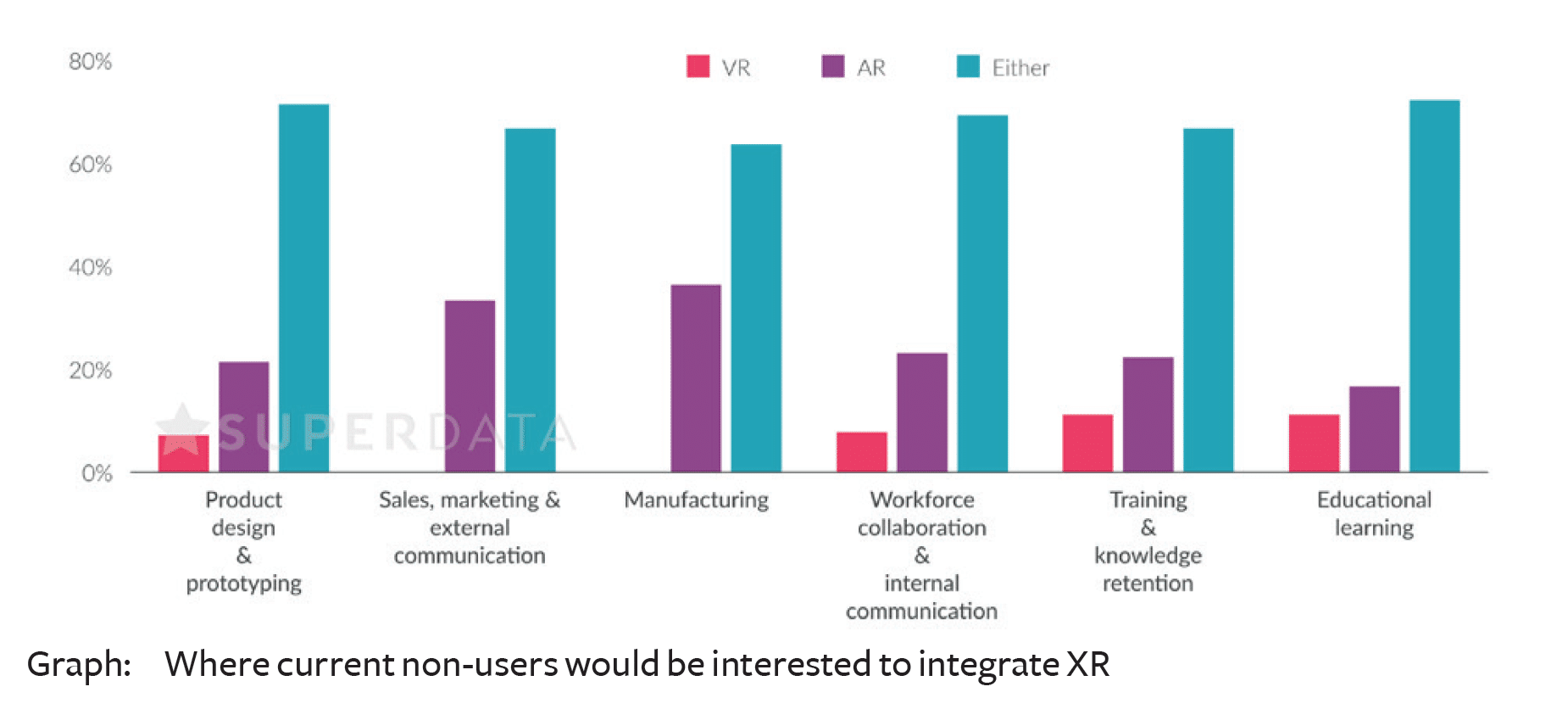

But just like we do in our consumer surveys, sometimes more strategically valuable signals come from non-users. In XR’s early days, non-users outnumber users so it’s a key target market to appeal to. And that requires knowing what they want (and don’t want).

For those non-users, the view is that they’re interested in AR for manufacturing and sales & marketing. Like current users (above), they’re interested in VR for training & knowledge retention and educational learning. One surprise was VR’s absence from sales & marketing.

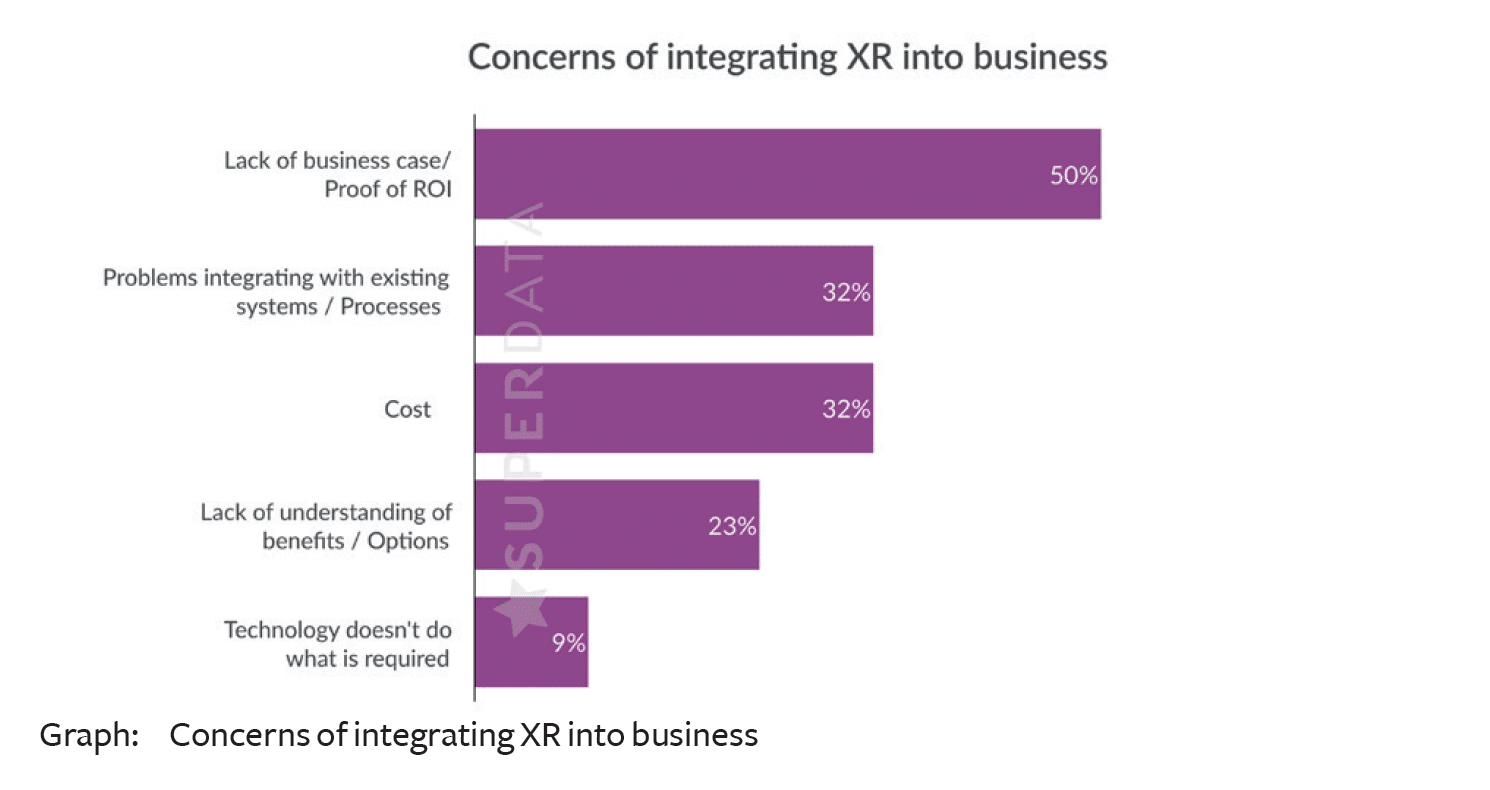

Lastly, speaking of non-users, what are the reasons they aren’t adopting? The biggest reason by far (50 percent) was lack of clear ROI. This signals us that education is needed because that ROI has been validated… enterprise buyers just aren’t seeing that yet.

You can see more about the survey sample, methodology and full results set by downloading the full report. And stay tuned for lots more data analysis here, including our own. For access to our entire intelligence vault, subscribe to ARtillry PRO.

For deeper XR data and intelligence, join ARtillry PRO and subscribe to the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.

Header image credit: Microsoft