“Behind the Numbers” is ARtillry’s series that examines strategic takeaways from its original data. Each post drills down on one topic or chart. Subscribe for access to the full library and other knowledge-building resources.

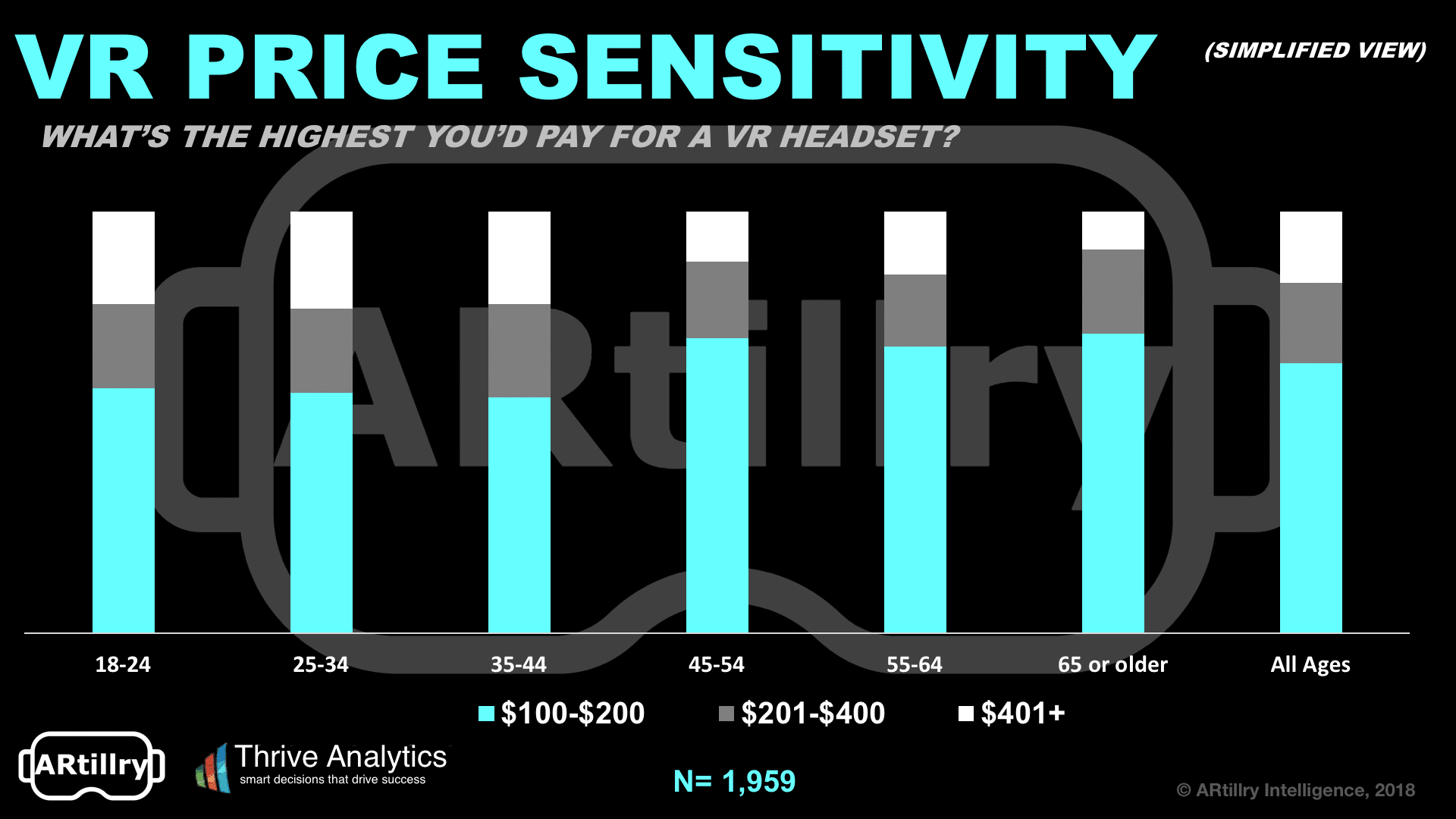

Price elasticity is a big factor for VR, given that it’s a new/ non-critical product that can be expensive. But what are the specific ways that price is a gating factor to VR adoption? And more importantly, what price points represent triggers for consumer interest – or disinterest?

To begin, the greatest interest in VR not surprisingly exists at lower price points ($100 – $200). And the least interest lies with more expensive purchases (greater than $400). Given that tier-1 headsets primarily exist at those higher price points, they are most susceptible to price sensitivity.

Broken down further, there’s a clear correlation between price sensitivity and age. Younger consumers are more willing to pay greater sums for VR headsets. This is due to the same reasons that make them more attracted to VR in general, as “digital natives.”

Loss Leader

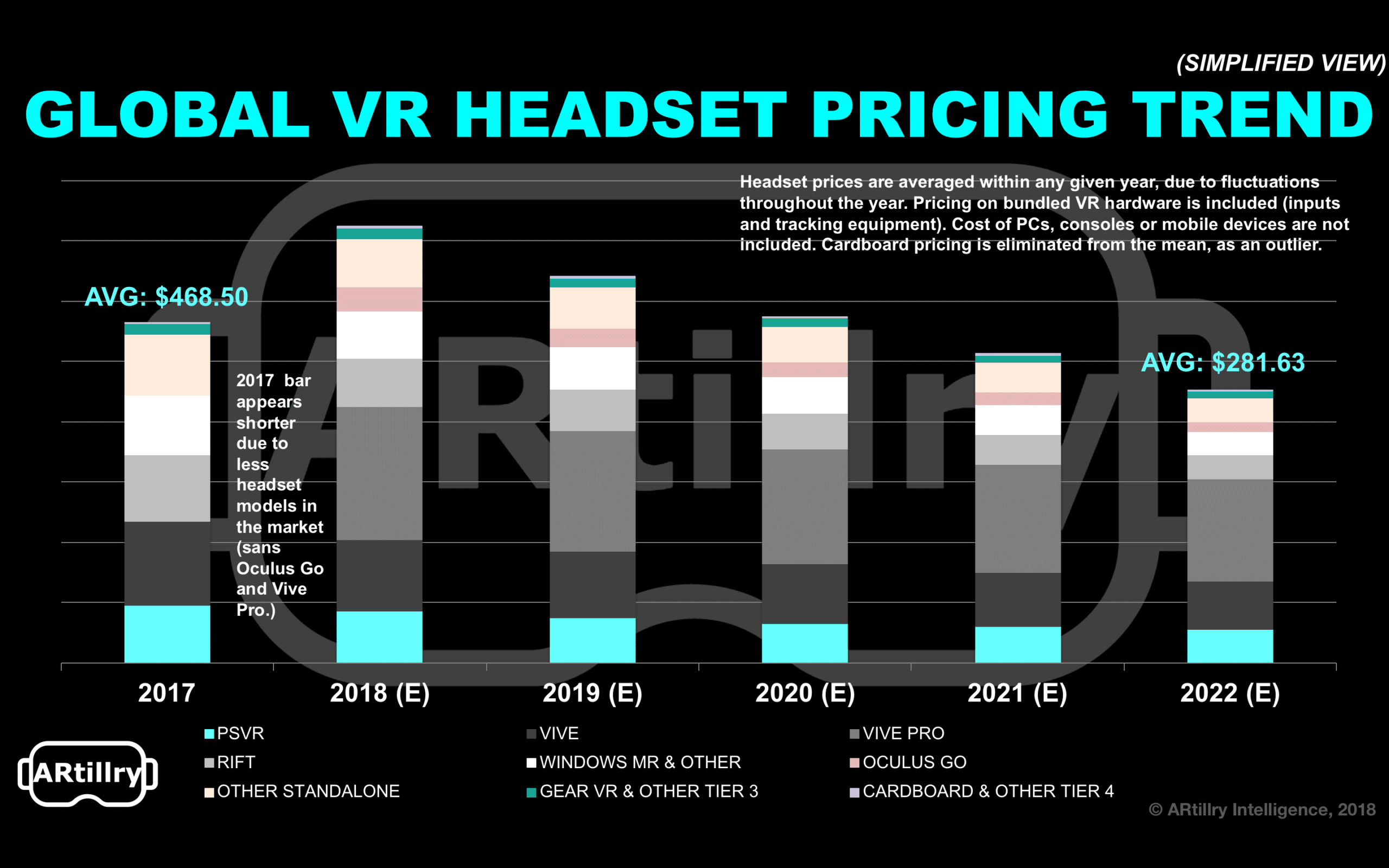

But the biggest takeaway is the pricing threshold under which adoption inflects: $200. This is consistent with Wave I findings and validates our analysis about the “magic price point” for consumer VR. It’s no mistake that it’s also the price of VR’s biggest projected mover: Oculus Go.

As we’ve examined, Oculus Go is priced at $199 to bring higher-end VR to a greater swath of the mainstream public, and to better seed a VR marketplace. Oculus has the luxury (Facebook) of treating VR hardware as a loss leader to build market share and a longer-term platform strategy.

This is something Facebook missed by not launching a smartphone as a direct consumer touch point. It instead has to reach consumers through apps that operate on devices that Google and Apple control. It therefore lacks vertical integration and the ability to optimize and tune hardware.

Given Mark Zuckerberg’s vision of a VR future, that’s not a barrier he wants to face again. Though smartphones are highly conducive to social engagement and connectivity, Facebook sees VR as an even greater bedfellow for the future of digital social interaction (though it could take a while).

But that long-term approach comes at a cost: to sacrifice margins for market share. That’s due to the fact that platform wars are won through momentum set in early days to attract users. Then there’s a domino effect of developer interest, incentive, content creation… and then more users.

Seeding a Market

Put another way, it’s all about attracting users by any means to seed a marketplace and establish an installed base. That economically attracts developers who create content, which attracts more users. Those users in turn attract more developers… and the virtuous cycle commences.

Meanwhile, consumers win by receiving a strong value on hardware from Oculus. But not everyone wins: companies reliant on short-term hardware margins (Samsung, HTC, etc.), will find it harder to compete. HTC Focus already delayed U.S. distribution plans for this reason.

Overall, it’s a lesson in loss-leader economics, and strategic positioning in early days of platform wars. We saw the same thing in the smartphone OS wars. And like we saw then, consumers benefit most. Prices should continue to drop, along with an arms race for VR quality.

Along those lines, one looming question is if these competitive pricing dynamics will move into Tier-1 VR. Given that Oculus is aggressive with Rift pricing too, could it impact HTC Vive and others? That could already be happening per the headset share shifts we’ve seen lately.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.