Data Point of the Week is AR Insider’s dive into the latest spatial computing figures. It includes data points, along with narrative insights and takeaways. For an indexed collection of data and reports, subscribe to ARtillery Pro.

There’s lots of discussion about how spatial computing can support the “new normal.” That’s everything from working at home to virtual events. It also includes VR’s immersion and escapism (entertainment); and AR’s applications in workplace collaboration and home services (utility).

But counterbalancing those demand drivers may be supply constraints. Though spatial tech may get the chance to shine in challenging times, the practical reality of disrupted supply-chains may impede the ability to deliver — at least for headset-based experiences (currently a small share).

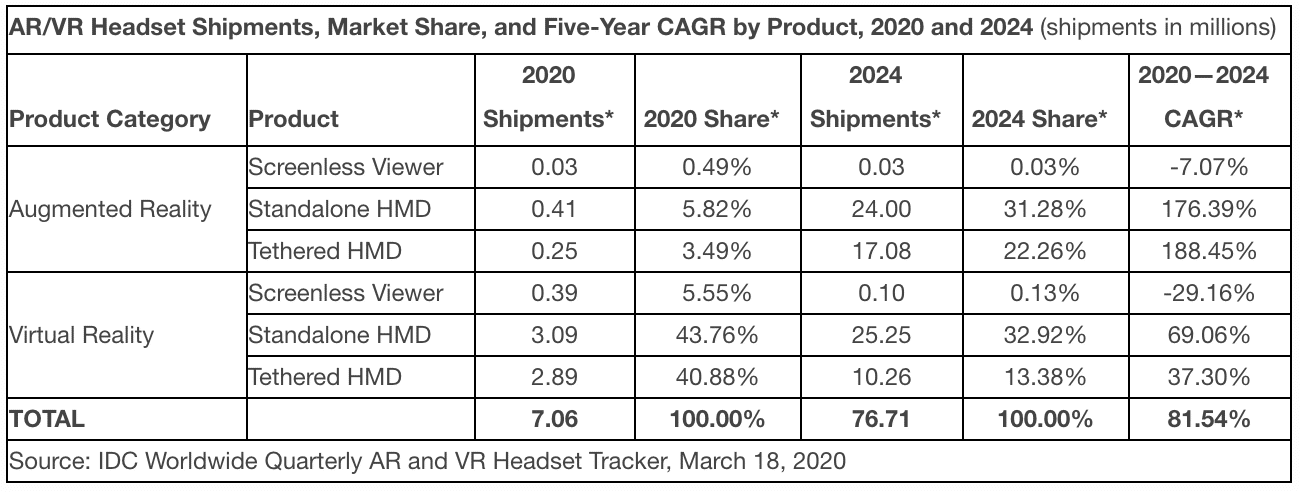

Specifically, IDC projects a year-over-year decline in shipments of 10.5 percent in Q1, followed by 24.1 percent in Q2. Assuming production ramps back up by early Q3, IDC projects a rebound which brings total 2020 shipments to 7.1 million units, up 23.6 percent from 2019.

Looking further out, the firm projects strong long-term growth, with headset shipments reaching 76.7 units by 2024, which is a compound annual growth rate of 81.5 percent. Of course “headsets” is a bit conflated, as subcategories (AR, VR, etc.) vary widely in demand curves.

Drilling Down

With that backdrop, how do things break down by headset class? The first delineation is AR versus VR, with device-subclasses branching from there (see above). The most growth in 2020 will be in VR, which isn’t surprising given that it’s more mature than AR in its product lifecycle.

Within VR, IDC projects the greatest growth for standalones like Oculus Quest and VIVE Focus. This is where the momentum lies today, especially Quest. But these numbers do raise eyebrows because dominant market share is still held by PSVR, which is in the tethered category.

Specifically, Sony announced 5 million cumulative units sold in January. Extrapolating from that known quantity, our research arm ARtillery Intelligence pegged PSVR’s 2020 unit sales at 2.83M. IDC total for all tethered headsets (2.89M) would mean retraction for PSVR, which is possible.

Back to standalones, IDC goes in the other direction with an optimistic 3.09M units for 2020. Oculus Quest — the fastest growing standalone — sold about 425,000 units in 2019 according to our calculations. To get from there to 3 million — including other standalones — is hopeful.

Augmented Outlook

As for AR, that’s where things get a bit iffier. 2020 projections seem mostly reasonable at 690,000. That’s led by standalone AR headsets which is presumably driven by Hololens 2. But question marks loom over its already-challenged supply chain, plus the latest pandemic constraints.

Based on those challenges and Hololens’ existing sales levels, ARtillery pegs its 2020 unit sales at 120,000. That would seem to clash with IDC’s 690,000 for the standalone AR category. Microsoft committed 100,000 units to the U.S. Army, but that’s amortized over several years.

As for other AR device classes, IDC projects tethered headsets to reach 250,000. This category includes Magic, Leap One and Nreal Light. Given Magic Leap’s rumored 6K unit sales and Nreal’s late-year launch, 250,000 units in 2020 would have to rely on hefty enterprise HMDs sales.

More optimism comes in later years, where IDC projects AR headsets shipments to exceed 41.1 million units by 2024. That’s led by standalone headsets. But given AR headsets in total are now selling well under 1 million units, this is impressive growth — a CAGR approaching 190 percent.

Vantage Points

31 million also deviates widely from ARtillery figures which peg 2023 AR headsets 2.89 million units (see above). The latter assumes Apple’s market entrance in 2022 which itself is even a wild card. Of course, differing projection models is perfectly okay, as long as they’re defensible.

There’s less deviation in VR’s outer year projections. IDC forecasts 35.5M units in 2024, compared to ARtillery’s 21.6M in 2023. Both firms believe that standalones will have a commanding share. They’ll be required to drive mainstream adoption where things start to scale.

But back to the near term, the next few quarters will see an impact from global supply chain constraints due to Covid-19. The AR industry can hope that this will cause pent-up demand that drives late-year surges. That could be exacerbated by demand spikes for remote productivity.

In all of the above figures — and deviation between different firms’ projections — we must state our bias in affiliation with the ARtillery Intelligence cited figures. When it comes to outer year figures, there are lots of educated assumptions so the right answer is probably somewhere in the middle.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.