Venture funding can be one health indicator in any sector. AR and VR are no exception. After a frothy period of VC action in the 2017-2018 hype cycle, a moderate correction led to industry shakeout and a corresponding decline in venture appetite for all things spatial.

Now, in a gradual rebuilding period (following typical post-hype cycle patterns), things appear to be progressing at measured paces. That can be seen in spatial computing subsegments like AR marketing and consumer VR. Both are seeing real traction and year-over-year gains.

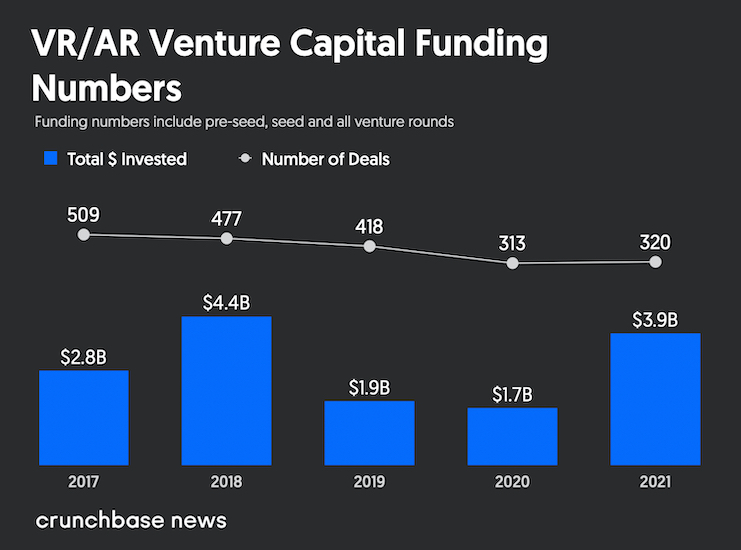

Back to investing indicators, venture funding seems to be reacting to these rebounds. Specifically, Crunchbase reports that aggregate AR and VR sector investing was up 229 percent year-over-year in 2021 to $3.9 billion. $1.9 billion of that came in Q4, setting a new sector record.

Some of that growth may be due to sober AR and VR confidence levels re-emerging. But another common investment driver is competition for startup equity due to FOMO (fear of missing out). And we’re seeing that in overdrive due to one prevailing factor: metaverse mania.

Data Dive

Synthesizing all of the above macro factors (and more explored below), what’s the real impact on venture funding in AR and VR? And what are the biggest deals that drove 2021’s venture inflection? We’re breaking down Crunchbase’s latest figures for this week’s Data Dive.

As noted, XR startup funding in 2021 was $3.9 billion. This makes it the second-best year on record following 2018’s $4.4 billion. The latter was largely due to a few mega-rounds for companies like Magic Leap and SenseTime. 2021 was a bit more distributed, but only slightly.

Speaking of which, a monster Q4 buoyed 2021’s VC spending total as noted above. To break that down, seven of the top 10 rounds happened in the fourth quarter. Those include a few large deals that boosted the total….not unlike 2018. Another similarity to 2018 was Magic Leap.

Here are a few Q4 highlights, followed by the broader trendline:

- Magic Leap raised $500 million in October.

- Niantic closed a $300 million Series D in November.

- Avatar application developer NAVER Z raised a $188.2 million Series B in November.

Down to Earth

Back to VC macro factors, there’s been a longstanding seller’s market for startup equity (but not for long). More sources of capital in private markets have given startups optionality and negotiating leverage. That caused valuation multiples to ratchet up over the past few years.

Those factors likely drove some of 2021’s venture spending growth in AR & VR. And if that’s the case, we may see that growth rate decline in 2022 as several broader counterveiling factors bring recurring revenue multiples (a common valuation metric) back down to earth.

Keep this in mind if we see 2021’s momentum in AR & VR funding slow. Though venture funding is an indicator (sometimes lagging) of sector health, the sheer dollars being spent is steered by several other economic factors. So quantity of deals may be a more fitting health check.

Either way, the gradual rebound and sober revenue growth for several AR and VR sub-sectors will likely continue in 2022 regardless of venture funding indicators. That will involve several signals and symptoms, including metaverse FOMO, that we’ll continue tracking in 2022.