Like many analyst firms, market sizing is one of the ongoing practices of AR Insider’s research arm ARtillery Intelligence. A few times per year, it goes into isolation and buries itself deep in financial modeling. One such exercise zeroes in on headworn AR revenues.

This is one of the main subdivisions of spatial computing – others include mobile AR and VR. They’re all related and share technological underpinnings, but are driven by separate market forces such as their respective hardware bases (see methodology and inclusions).

So what did the headworn AR forecast uncover? At a high level, global headworn AR revenue is projected to grow from $2.61 billion in 2024 to $14.02 billion in 2029, a 39.96 percent CAGR. This sum consists of consumer and enterprise spending and their revenue subsegments.

Drilling down, our latest Behind the Numbers installment looks at the hardware unit sales that are driving the above figures. How many pairs of AR glasses are expected to sell? What’s driving growth and momentum? And which device classes are seeing the most traction?

Headworn AR Global Revenue Forecast: 2024-2029

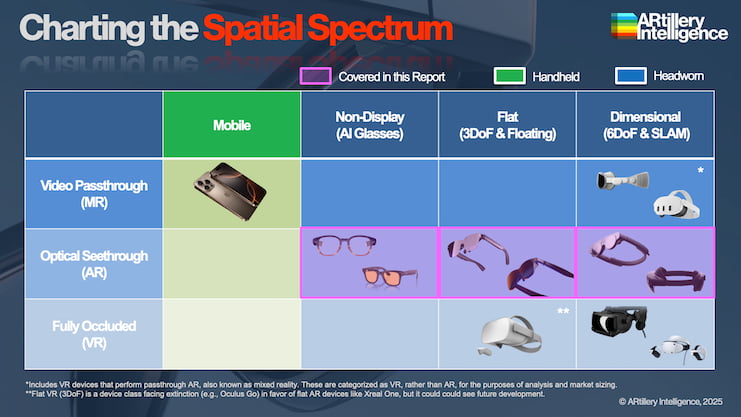

Spatial Spectrum

Starting at the top, AR headsets are projected to grow in unit sales from 1.88 million in 2024 to 12.36 million in 2029. That translates to an installed base of 34.13 million units by 2029, driven largely by an expected 2027 inflection – the first full year of sales for several anticipated devices.

For example, we’re seeing the culmination of hardware road maps from tech giants that are investing heavily in AR glasses. Those include Apple’s rumored smart glasses development, as it shifts its primary attention from Vision Pro (tracked separately in our VR forecast) to glasses.

We’ll also see Meta’s continued moves and generational updates for Ray-Ban Meta Smartglasses (RBMS), Meta Ray Band Display Glasses (MRBD), and its evolutionary path towards the holy grail: Orion. Meanwhile, Snap will enter the market for consumer AR glasses in 2026.

Android XR will also be a key player that could do for AR what Android did for smartphones over the past 15 years. This includes lowering barriers for hardware makers by offering a stable and established operating system while they maintain focus on the sheer gadgetry.

All these devices map to different AR device categories, including Tier-1 (dimensional AR), Tier-2 (flat AR), and Tier-3 (non-display AI glasses). The latter sees the greatest traction today due to a lighter and style-first form factor that appeals to mainstream consumers (more on that in a bit).

Moreover, this AR landscape demonstrates a trend towards several tracks and purpose-built devices. Qualcomm meanwhile propels this trend with a range of chips that power specific points on the spatial spectrum, including its new AR1+ Gen1 that powers AI-powered smart glasses.

Reality Check

Back to the movement towards lighter form factors, a new breed of slimmed-down and AI-fueled consumer smart glasses is seeing the greatest growth. These deviate from the do-everything bulk and overly ambitious UX targets that defined the previous generation of AR hardware.

For example, RBMS has taught the AR industry that optics – and their many design challenges – aren’t needed for a worthwhile UX. AI can replace graphics as an AR glasses selling point – including messaging, notifications, visual search, etc. — thus enabling lighter form factors.

A similar but different ‘lite-AR’ principle is demonstrated by display glasses such as VITURE. These eschew dimensional AR for a simpler and more focused proposition: massive virtual screens for 2D gaming & entertainment – a use case validated by our consumer survey data.

Furthermore, until fully-immersive AR (a la Meta Orion) is viable in consumer-friendly form factors, these simpler experiences will define AR. This realization has caused a refocusing and reality check for the AR sector to stop trying to necessarily go to market with full-blown (SLAM) AR.

That said, dimensional AR (tier-1) can work in today’s market if done right. Again, there are several purpose-built tracks developing. Snap will be first to market next year with a consumer-focused tier-1 device, and that will be a telling moment for market demand and receptiveness.

Lastly, back to ‘reality checks,’ we’ll conclude by saying that the 34 million projected installed base noted earlier for 2029 is dwarfed by the global smartphone installed base by 108 to 1. So though AR glasses could grow fast, they have quite a way to go to reach any semblance of ubiquity.

We’ll pause there and circle back in the next Behind the Numbers installment with more numbers & narratives. Meanwhile, check out the full report.