VR traction over the past several years has been slower than many had anticipated. But it’s still finding small wins and is growing at a fairly healthy pace. So the question is how well it’s landing with consumers today, and are those sentiments trending in the right direction?

So we set out for answers. Working closely with Thrive Analytics, ARtillery Intelligence authored questions to be fielded through its established survey engine to more than 50,000 U.S. adults. The result is Wave 9 of the research, and a narrative report we published to unpack the results.

Known as VR Usage & Consumer Attitudes, Wave 9, it follows similar reports over the last few years. Nine waves of research now bring new insights and trend data to light. And all nine waves represent a collective six-digit sum of U.S. adults for robust longitudinal analysis.

Among the topics tackled: How is VR resonating with everyday consumers? How often are they using it? How satisfied are they? What types of experiences do they want most? How much are they willing to pay for it? And for those who aren’t interested in VR… why not?

Functional Factors

After last week’s look at the top areas of improvement that VR users want to see in the technology, we switch gears to non-users. Specifically, how big is this cohort in the survey sample, and what are their feelings about VR… starting with whether or not they’ll try it anytime soon?

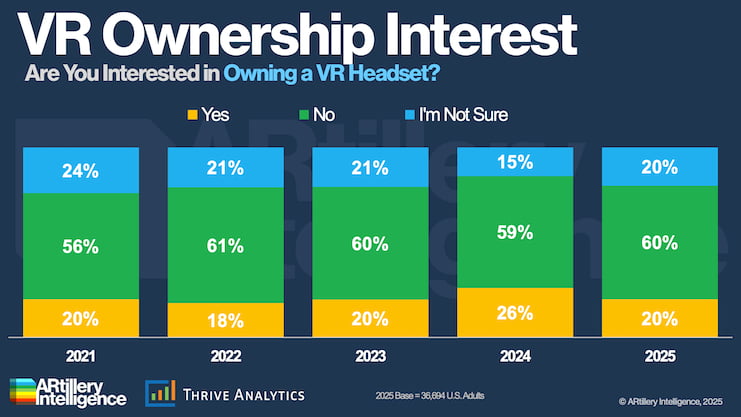

Starting at the top, how do VR non-users stack up to users? The former’s share of the survey sample currently stands at 73 percent. That makes VR users correspondingly represent 27 percent of U.S. adults (tried at least once, not necessarily active), as noted earlier in this report.

Back to non-users, how many of those 73 percent are interested in trying VR? 20 percent report interest, while 60 percent aren’t interested, and 20 percent aren’t sure. As for year-over-year trending, 20 percent interest is down from 26 percent in the previous survey wave.

That last part is a discouraging finding for VR proponents. However, the dip in interest among non-users is aligned with historical sentiments in past waves of this survey. In other words, the 26 percent in the previous wave was a jump in interest that deviated from the historical trendline.

Halo Effect

Sticking with that Wave 8 surge in interest, it could mean many things, including the “halo effect” from Apple Vision Pro’s launch at the time. In any case, Wave 9’s 20 percent figure doesn’t look as bad when eliminating the Wave 8 outlier and panning back to the broader trendline.

Regardless of the long view, 20 percent interest among non-users is a strong result. Though aspirational – as opposed to firm financial commitment – 20 percent interest from VR non-users shows a degree of affinity for the technology, and signals hope for its near-term future.

In practical terms, some portion of those interested non-users will convert to VR users in the next year… Indeed, that’s precisely how this data point has translated to a steady but small uptick in VR users in the year-to-year progression of this survey series. So we’ll watch for that.

We’ll pause there and pick things up in the next installment. Meanwhile, check out the full report for more.