This post is adapted from ARtillry’s latest Intelligence briefing, XR: 2017 Lessons, 2018 Predictions, and specifically zeroes in on 2018 predictions. You can preview more of the report here, or subscribe to access it in full.

Weaker than expected AR & VR (XR) hardware sales defined 2017. As is often the case with emerging tech, hardware is a key leading indicator because it comes first and creates an installed base for software and overall market growth.

VR hardware’s softness in 2017 led to restrained excitement levels and readjusted market sizing. Attention shifted to mobile AR, given a greater installed hardware base, but even that has receded to some degree, given weak content thus far.

This all amounts to a bit of a shakeout, and a market correction from the XR exuberance that defined 2015 and 2016. The question is if it will continue into 2018. With that backdrop, here are some of our predictions and rationale for XR this year.

Enterprise AR Pulls Ahead

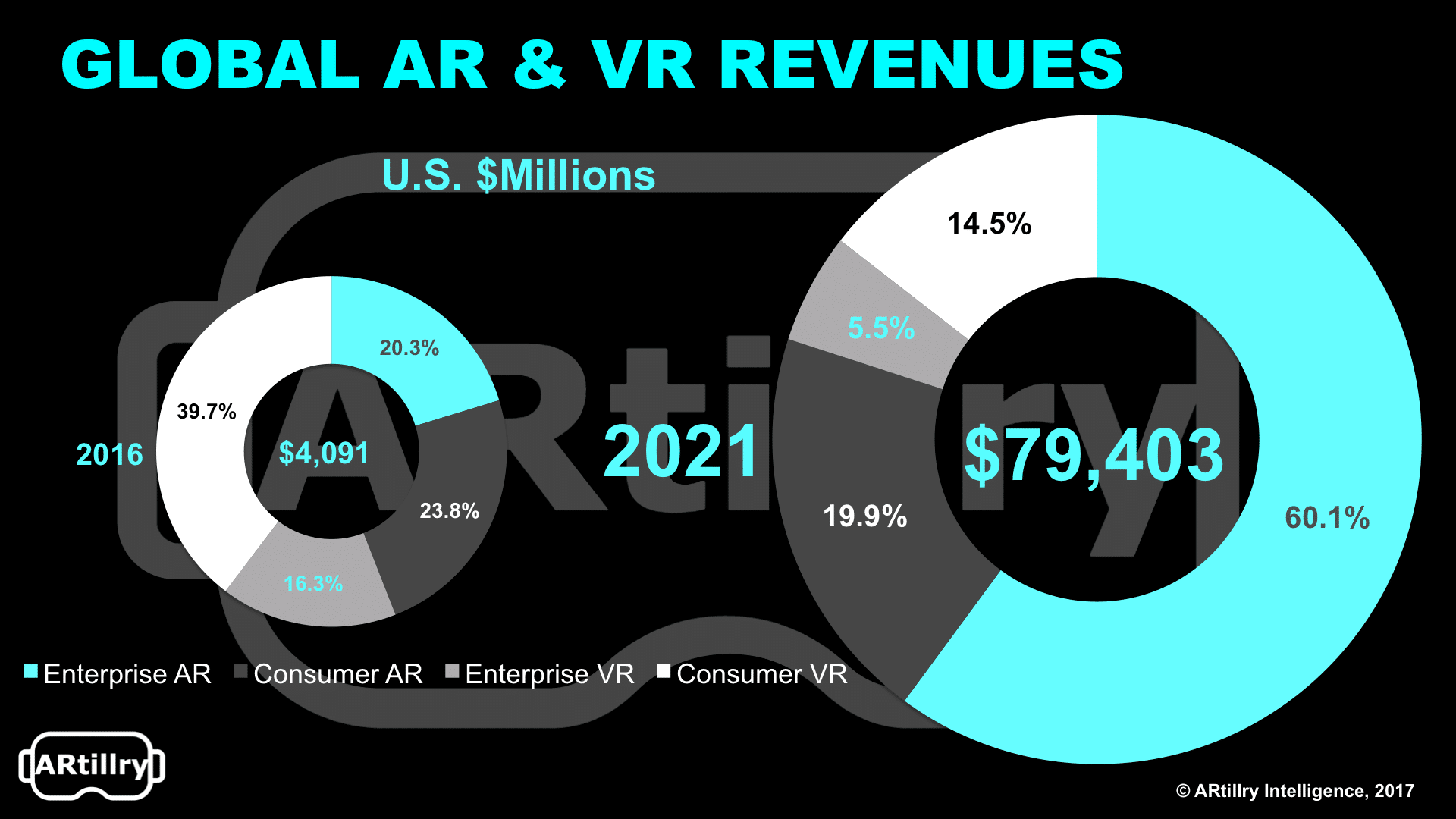

Enterprise AR will pull ahead of Consumer VR as the leading XR sub-sector, reaching revenue of $10 billion. The biggest adopters in 2018 will be manufacturing and assembly, which have the clearest ROI potential for enterprise AR.

The biggest challenge will be organizational red tape and sales cycles. So the name of the game will be quantifying ROI, demonstrating bottom line impact and having domain knowledge in enterprise verticals (in addition to immersive tech competency).

Those who can hit those marks will be most successful in tapping into enterprise AR’s $48 billion opportunity by 2021.

Mobile AR Rebounds

After surging in 2016 due to Pokémon Go, then dipping in 2017, mobile AR revenues will rebound in 2018, exceeding $1 billion. This will mostly come from app revenue, including Niantic’s Harry Potter game that inherits Pokémon Go’s architecture and game mechanics.

The predominant mobile AR business model in 2018 will follow Pokémon Go’s in-app purchase model. We’ll see experimentation with ad support or sponsorship that are tied to location-based discovery and commerce (i.e. retail store visits, navigation, product info).

Mobile AR Standards Develop

After disappointing mobile AR app libraries in 2017 (in both quantity and quality), 2018 will continue to see many misfires and unsuccessful apps. A small minority will break out and begin to define the category and seed user demand.

They will apply native thinking, “AR-first or “AR-Only” approaches, but these success stories will be very limited in quantity – likely fewer than ten. At least one of these apps will break out in 2018 as mobile AR’s first truly native and category-defining “killer app.”

That app will be location-based gaming, social, or commerce oriented, and will apply best practices in driving stickiness and repeat/active usage.

Consumer VR Gets a Jolt

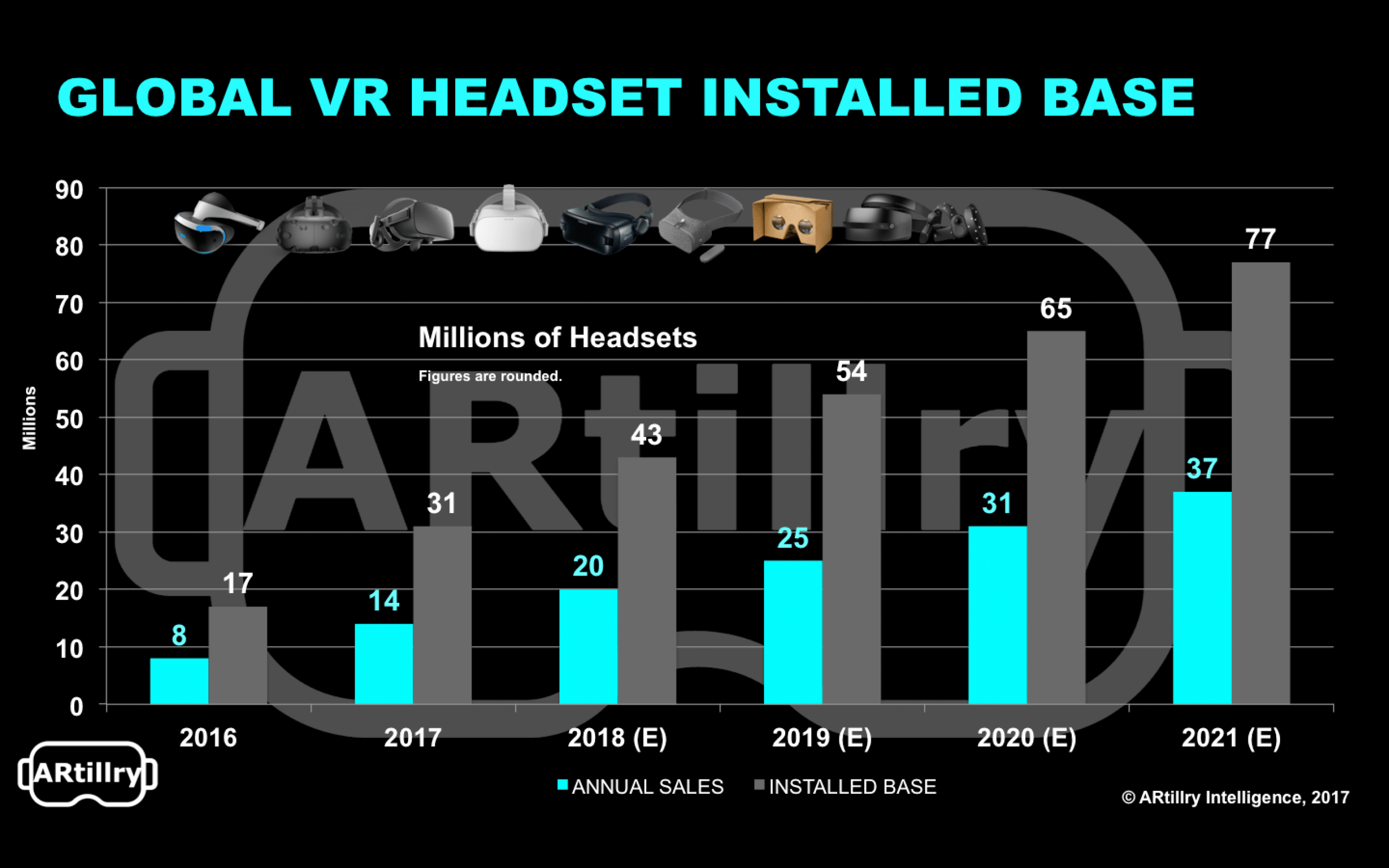

Oculus Go will launch in Q2 2018 and fuel consumer adoption more so than any other single headset to date. Its sales will exceed one million units in 2018, and begin to climb to a leading headset market share in later years.

With a $199 price tag, and more room for discounting, this will jumpstart VR’s sluggish sales and adoption rates. It will also create a greater installed base to motivate developers and content creators to build content, thus attracting more users to VR in a sort of virtuous cycle.

This process will take more than one year to play out, but will accelerate in 2018 to the tune of about 20 million total headsets sold (including cardboard and low-cost units throughout China); and a cumulative installed base of about 43 million headsets globally.

Unifying Technologies Emerge

Beyond slower-than-expected consumer VR adoption, the sector has further suffered from fragmentation. The already small user base is divided into smaller subsets when you consider the different platforms and walled gardens (HTC, Oculus, Daydream, etc.).

This makes it harder for developers to justify ROI in investing in content because an already-small addressable market gets smaller. Alleviating this challenge will be a major industry priority in 2018, including interoperability across platforms.

We’ll also see more low-barrier and cross-platform development tools like Google Blocks and Poly; and unifying technologies such as WebVR and WebAR. Google will take the lead on – and benefit most from – web-based delivery of AR and VR experiences.

Lastly, the AR cloud will develop and gain importance for geo-tagged data and content to enable and populate AR apps and games. It will be a critical component, given AR’s understated need to access mapping and positional data to overlay graphics properly.

Preview more 2017 lessons and 2018 predictions here.

For a deeper dive on AR & VR insights, see ARtillry’s new intelligence subscription, and sign up for the free ARtillry Weekly newsletter.

Disclosure: ARtillry has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.