Data Point of the Week is AR Insider’s weekly dive into data from around the XR universe. Spanning usage and market-sizing data, it’s meant to draw insights for XR players or would-be entrants. To see an indexed archive of data briefs and slide bank, subscribe to ARtillery Pro.

Last week, we got a data point that represents a rare nugget in the VR world: a unit sales disclosure from a major hardware player. Sony announced it has sold 4.2 million PSVRs to date. This makes PSVR the leading headset among tier-1 VR (Vive, Rift, Rift S & PSVR).

The leading position is mostly owed to an installed base of 92 million PS4 consoles in market. This gives it an addressable market that its tier-1 counterparts don’t enjoy. The all-in cost for a PSVR owner is around $299 if she already owns a PS4. Rift and Vive “all-in” price is greater than $1K.

This “all-in” dilemma is receding however, as the standalone category rises. Standalone capability is improving in as shown in Oculus Go and the forthcoming Quest. There will remain a Tier-1 market (enterprise, gaming) but it will lose share over time to mainstream-friendly standalones.

This is because price elasticity is a top gating factor to VR adoption at this early stage, as it often is for products that are new, non-essential and pricey. There are very few ubiquitous products that are greater than $400: Car, fridge, TV, smartphone, etc. VR isn’t on that list and may never be.

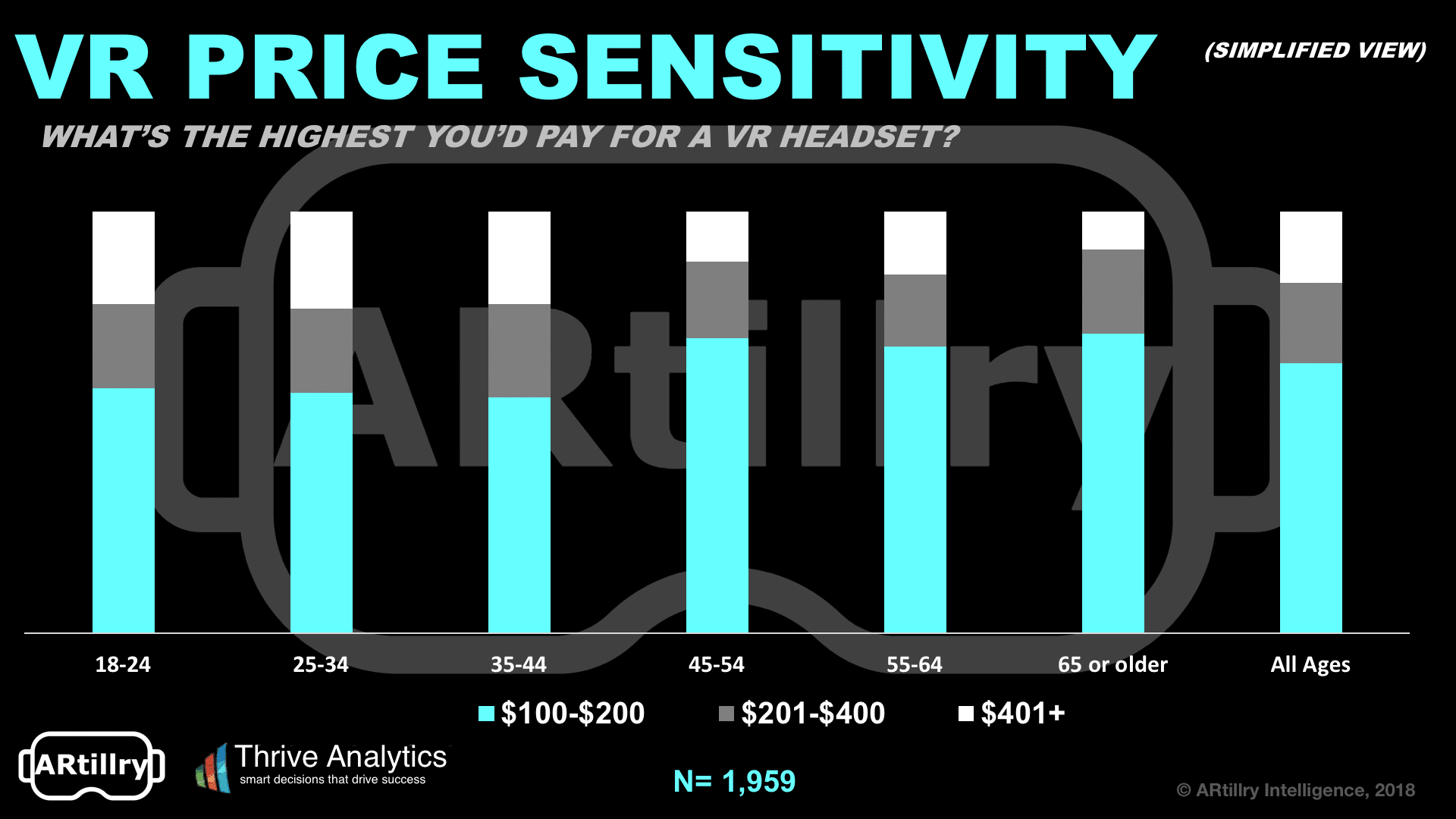

Instead, VR’s scale will come when the price dips below a certain threshold — or a price point that is “giftable,” as we like to say. And that magic price points where demand inflects are $200 and $400 according to our consumer survey research with Thrive Analytics (see above).

These two price points also happen to be where Oculus’ pricing strategy lies. The low-end (but still very capable) Oculus Go is $199, while the forthcoming standalone Quest is $399. The just-released Rift S is also $399, but that’s not an all-in price as it requires minimum-spec PC.

We expect big things of Oculus Go due to that loss-leader price point that Facebook has the luxury of offering as it trades “margins for market share” to seed a market. And it’s no slouch: with solid specs and a built-in content library (another key adoption factor), it tells a good story.

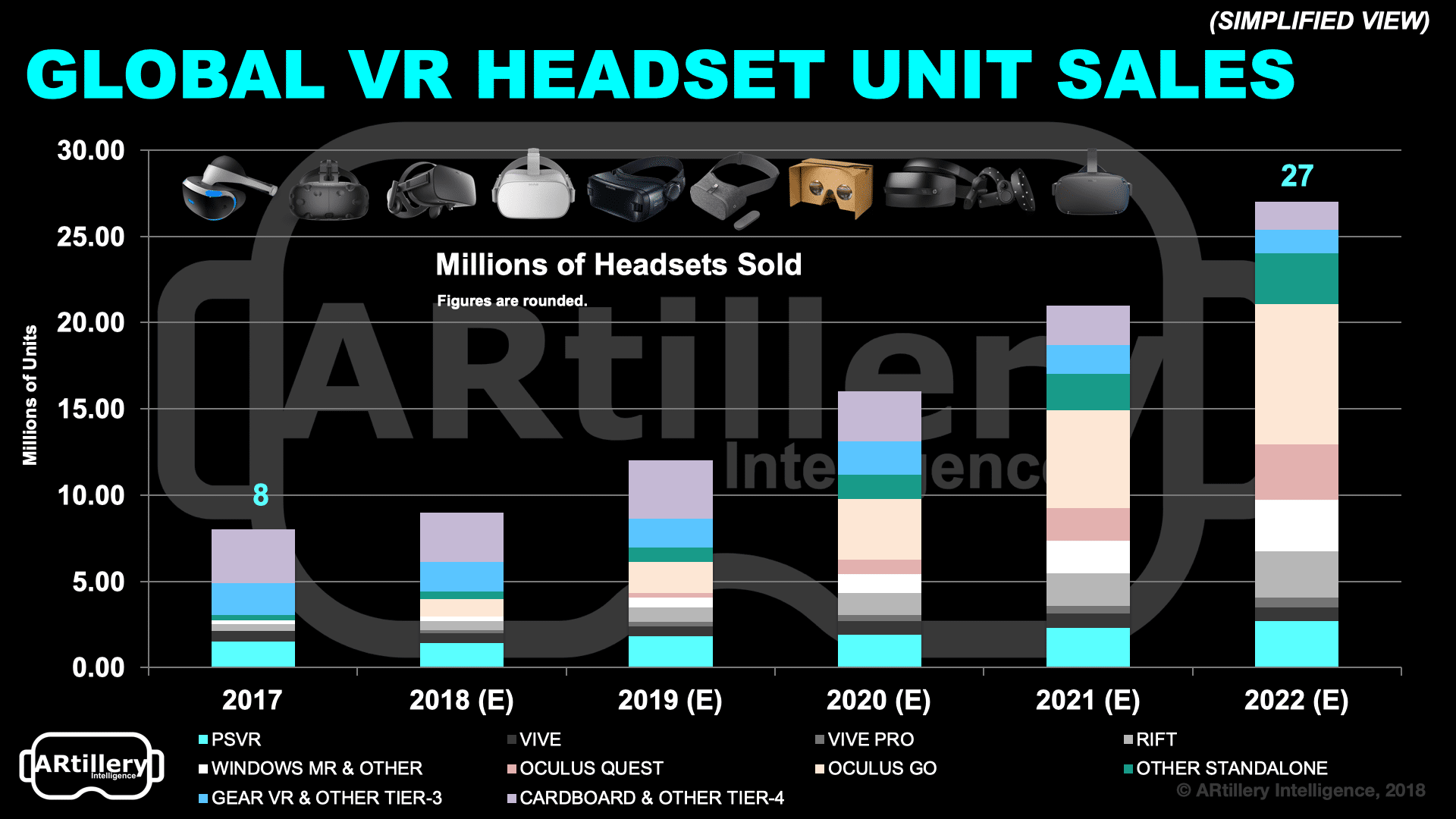

Back to the PSVR figure, it aligns with our projections, which pegged the headset’s installed base at 3.6 million units at the end of 2018 and full year sales of 1.79 million. We project it to lead tier-1 through 2022, but Rift S could gain share due to the aggressive pricing mentioned above.

Meanwhile, we’ll continue to aggregate market signals to pinpoint unit sales, market shares, pricing trends and all other ingredients of market-sizing and forecasting. Companies disclosing unit sales is a welcome gift, and will certainly be plugged into our next round of forecasting this spring.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.

Header image credit: Sony