This post is adapted from ARtillery Intelligence’s latest report, Hearables: Broadening the Definition of AR. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

Picking up where we left off with Apple, Google and Bose’s hearables strategies, what’s the revenue outlook? And what are the business models that will materialize around ‘audio AR?’ As we’ve examined, tech giants are highly motivated to make it happen. So where’s the money?

This starts with a common thread in the Audio AR apps we’ve profiled so far: there’s a process of learning and growing with an inherently new form of user interactions. The playbook for these experiences is being written as we speak and it will be an ongoing process.

“We invented new AR audio-first game mechanics and audio interactions that open up exciting new areas of AR design,” said Xeo Design’s Nicole Lazzaro. “Imagine the player’s head as the joystick. We saw this as an opportunity to explore how audio increases immersion.”

Learning Curve

This learning curve could apply to monetization too. Beyond UX, what monetization models will integrate best? Given that it’s a form of mobile gaming, in-app purchases or sponsorship could develop. These are models supported by ARtillery Intelligence’s consumer AR survey (see below).

Quirkeley’s Siciliana Trevino believes her audio AR app for Bose frames could be monetized through in-game local business fare. That includes food, after working up a hunger from the game’s physical activity; or real-life lattes to go along with the virtual lattes in the gameplay.

As we examined recently, Quirkeley’s War of the Worlds: Invasion is a verbal instruction-based game which leads users through an escape from alien invasion. Audio signals prompt users for physical actions which are then tracked through the IMU sensor bundle in BoseAR devices.

As for how that use case translates to business models, it will be an acclimation process. Audio AR is a new modality within an already-new AR medium. So just as these developers are embarking on a creative process for audio AR, business models could likewise be experimental.

Business Case

Drilling down on some of those potential business models, how could they play out? Like any nascent area it will develop in lots of directions. Some of those directions will be expected, while some will be surprises. Local discovery and in-app purchases could be natural, per the above.

Like any other emerging technology – including graphical AR – a value chain will develop. That includes software for experience creation “building blocks,” as we like to call them. The ecosystem will include big players like Bose, smaller toolset providers and app developers like Xeo Design.

But the hardware always comes first. That process is underway as Apple, Google, Bose and others are seeding the audio AR opportunity by conditioning the user behavior. The poster child here is Apple which sold 25 million AirPods last year, and are conditioning an all-day use case.

So it’s no surprise that the majority of revenues in the near term hearables market will be the sale of that hardware. Over time, software and other revenue sources will build on that installed base. But the lion’s share in early years will go to players like Apple and Bose who sell hearables.

Planting Seeds

But one key distinction is that they aren’t “hearables” yet to consumers. The user intent behind these hardware purchases isn’t largely AR-driven. To plant the seeds for audio AR and establish a hardware base, devices must be marketed towards consumers’ current comfort levels.

According to Bose’s John Gordon at January’s ARiA conference, this starts with familiar territory — music — before evolving into audio AR. So Bose is essentially fighting two battles: conditioning consumers to the hardware while stimulating developers to build Audio AR apps.

“Start with something people want,” said Gordon. “People want to bring music into their lives. They want to bring sound in, and they’ll put something on their head to do it. But we wanted to go beyond that. We figured now that we’ve got something on people’s heads, what’s next?”

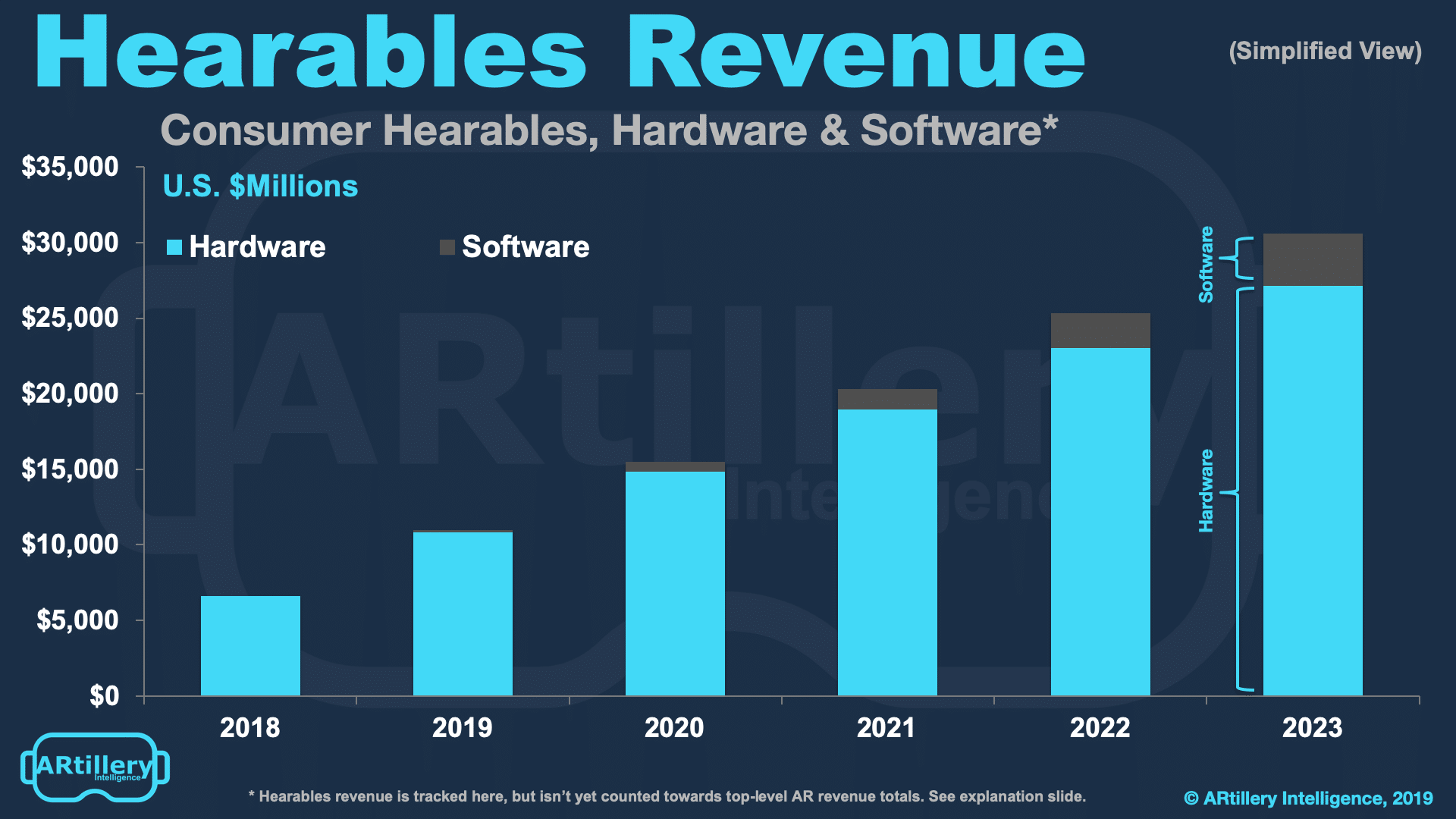

The reason this distinction is important is that hearables hardware revenue isn’t classified as “AR revenue” in ARtillery’s market sizing. It’s tracked for perspective, but doesn’t yet contribute to AR revenue totals. Revenue generated from audio AR apps are classified as AR revenue though.

By The Numbers

With those caveats and definitions, what does the hearables revenue picture look like? Artillery Intelligence projects hardware revenues to grow from $6.6 billion in 2018 to $27.1 billion in 2023. Software will meanwhile grow from $174 million this year to $3.46 billion by 2023.

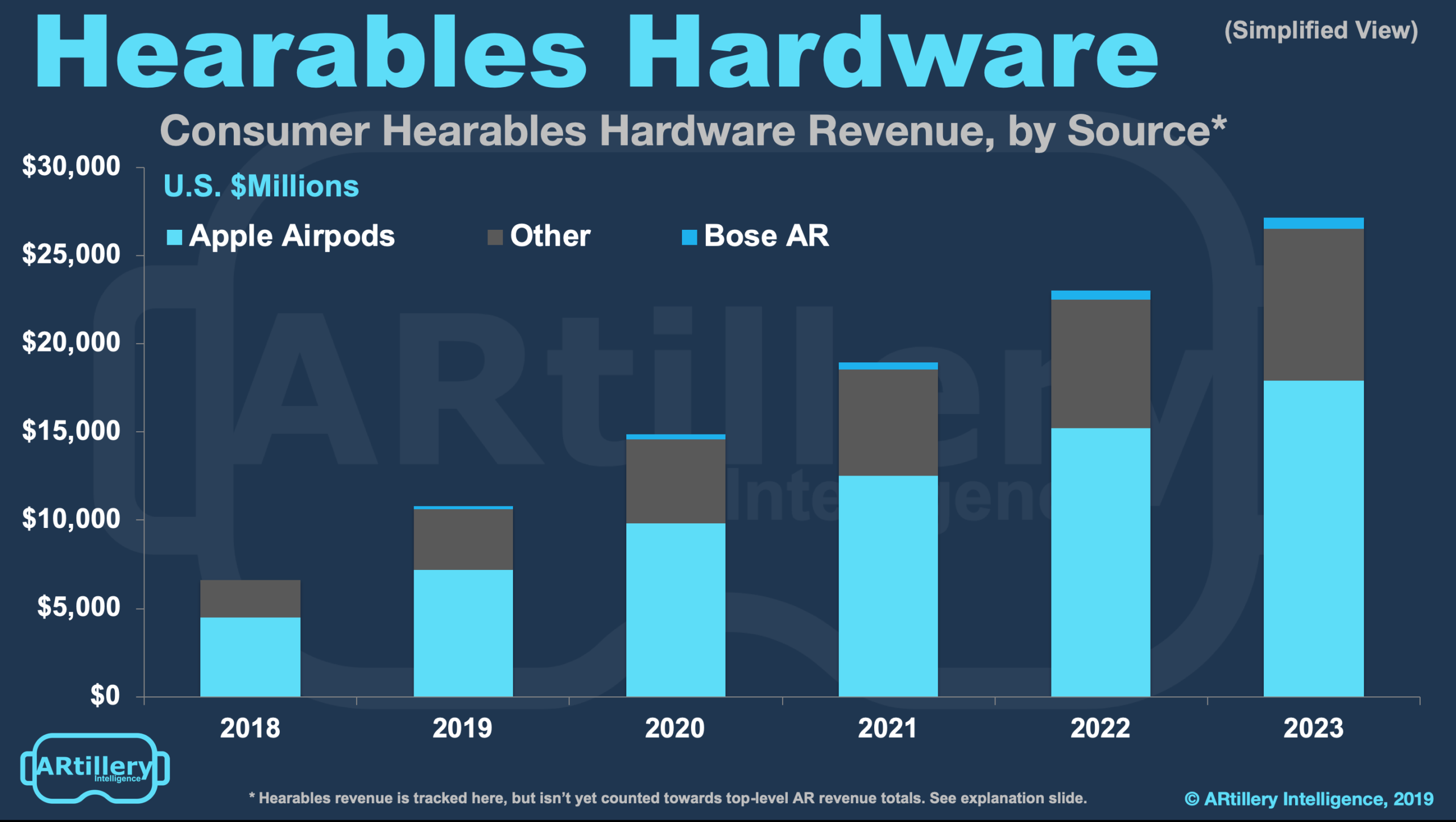

Further segmenting hardware revenue, Apple AirPods will maintain a commanding market share lead, growing from $4.5 billion last year to $17.9 billion in 2023. Bose will have a small but influential share of the hearables market, growing to $8.6 billion in 2023.

There will be others in this premium tier such as Google Pixel Buds, Samsung and others. Following these players, the remainder of the market will be a fragmented mix of commodity players that emerge globally, especially in China, to fulfill demand for lower-priced hearables.

These commodity players will make hearables accessible to a larger mainstream market and in developing markets. But innovation and market leadership will sit with Apple, Google and Bose, thus mirroring the typical dynamics of consumer electronics, most notably smartphones.

See more details about this report or continue reading here.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.