ARtillery Briefs is a video series that outlines the top trends we’re tracking, including takeaways from recent reports and market forecasts. See the most recent episode below, including narrative takeaways and embedded video.

In consumer-based AR’s early stages, a common question is ‘Where’s the money?’ There have been oscillations in excitement and doubt over AR, but the ultimate proof point will be revenue. Though aggregate revenues have disappointed so far, there are glimmers of hope.

This plays out today in a few revenue models bearing fruit. These are mostly tied to mobile AR, as headsests don’t yet scale in consumer markets (industrial enterprise AR is different). ARtillery Intelligence breaks this down in its latest report and AR Briefs episode (video below).

Full Funnel

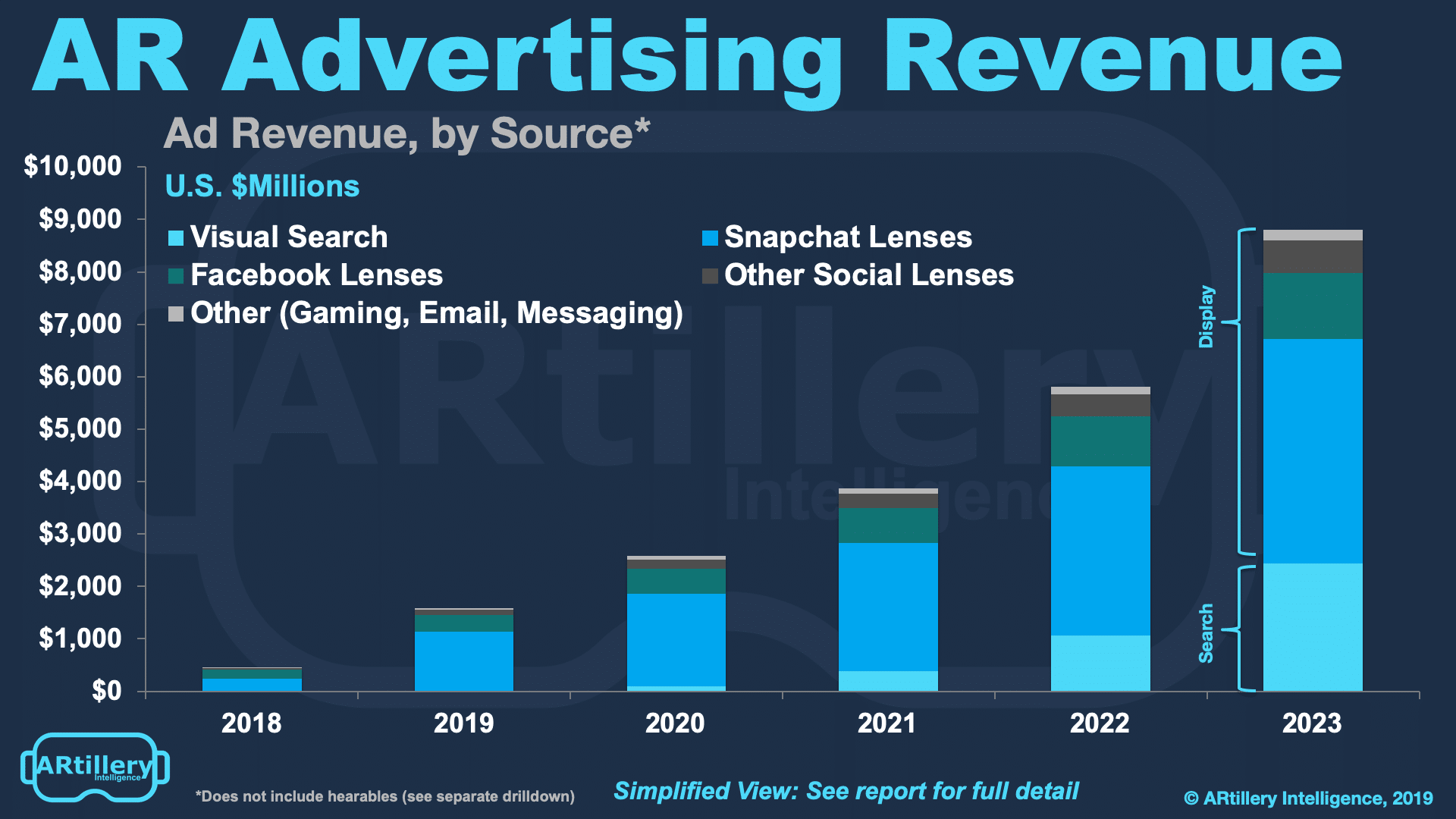

The first business model bearing fruit is AR advertising. This is growing as brands learn that AR can span the consumer purchase funnel. That includes upper-funnel reach-driven product/brand exposure as well as lower-funnel direct-response conversions from things like cosmetics try-ons.

AR also has inherent capabilities to demonstrate products in immersive ways; and brands like how it boosts their creative capacity. That’s proving out through user engagement rates and advertiser ROI, as well as brand spending: $453 million last year, growing to $8.8 billion by 2023.

Seeing that revenue and doubling down on it, Facebook, Snapchat and a few others are increasingly providing brands with tools to lower barriers for AR lens creation and capability. We’ll see that trend continue, such as Intagram’s potential “sleeping giant” status for AR ads.

Early & Unproven

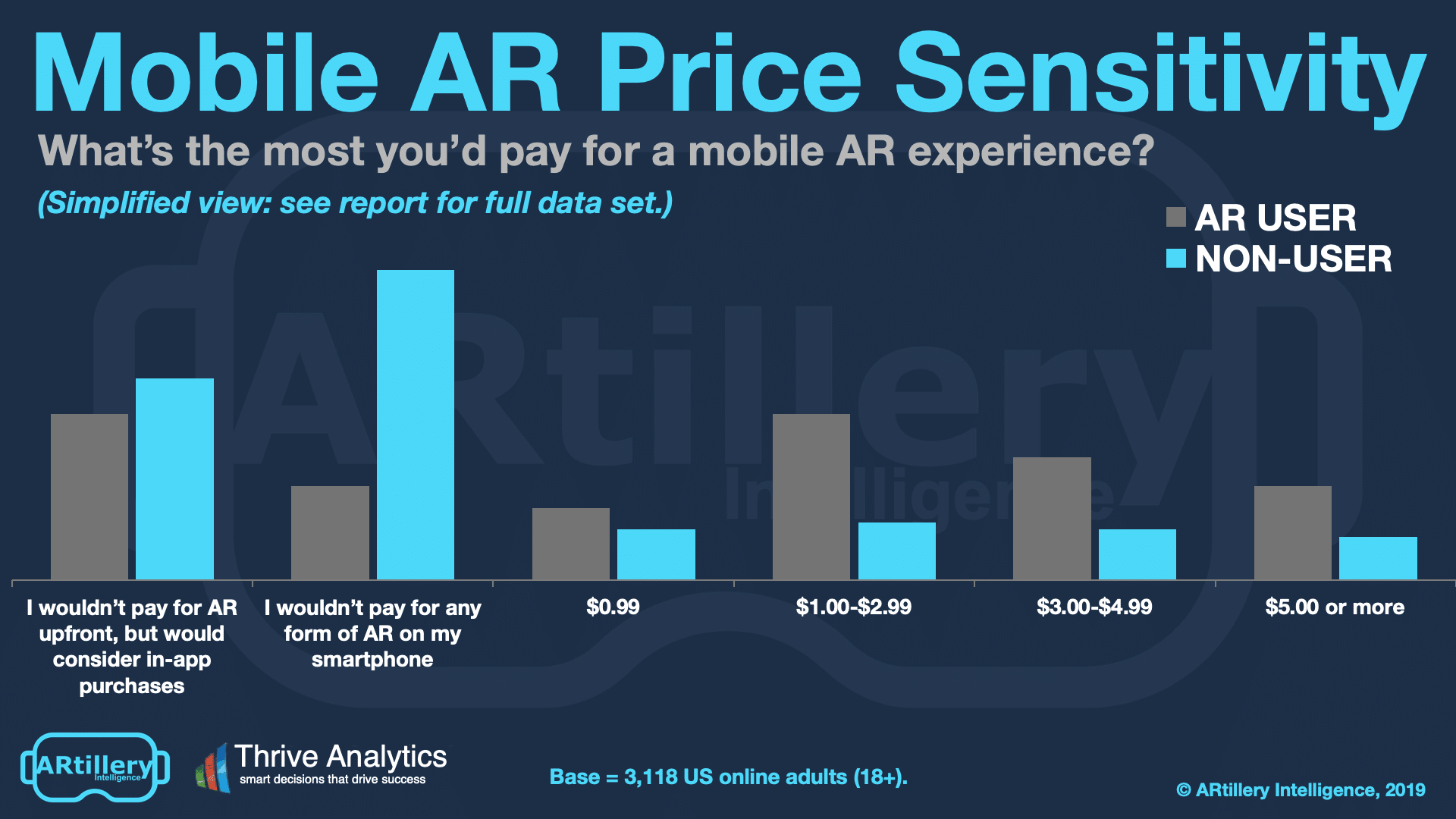

Moving on to the second model, in-app purchases (IAP) are fitting for lots of AR experiences, especially gaming. This stems from the model’s success in mobile gaming, and its ability to maximize revenue per user (ARPU) through the behavioral economics of micro-transactions.

More importantly, it’s fitting because AR is too early and unproven for consumers to pay upfront for premium apps. ARtillery consumer survey data support that. And if you need more evidence, just look at the roughly $2.65 billion in IAP that Niantic has generated to date for Pokemon Go.

Next, we believe IAP will extend from gaming into other areas like social lenses, where companies like Snap could tap into a long tail of consumer-purchased lenses, similar to what they did with geofilters. The business case is validated elsewhere, such as Fortnite’s avatar personalization.

Picks & Shovels

Lastly, there’s AR-as-a-service (ARaaS). This is a broad category that involves enabling tech that lowers friction or boosts capabilities for AR creation. So it includes game engines like Unity, AR experience creation like Amazon Sumerian, or Web AR enablement like 8th Wall.

The defining factor is that it’s all about lowering barriers for consumer-facing enterprises to build AR experiences for their customers. What will really drive this category is democratizing advanced AR for these entities as demand grows. It’s the proverbial picks and shovels in the gold rush.

For example, Adobe Aero is in a strong position by enabling AR for an installed base of creative professionals by integrating right into the Creative Suite. This should accelerate AR creation among consumer-facing brands by infusing AR capability in their existing workflows.

B2B2C

One thing you may notice from these models is that they have different spending sources. With advertising, brands pay for AR development and media activation. With IAP, consumers pay. And with ARaaS, consumer-facing enterprises pay for tools to build AR for their customers.

The last one is notable because it’s technically “enterprise AR” due to the spending source, but end users are consumers. Compared to industrial enterprise AR, these AR activations are meant to boost consumer engagement or purchases. That puts it in a category we call B2B2C.

Lastly, it’s worth noting that there are several more business models in AR such as headset sales. But it’s the above three models that are bearing the most fruit in early days as they tap into consumer-based mobile AR use cases. Check out more color in the video below or full report.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.