One health indicator in any tech sector is the venture funding that flows into it. XR is no exception as its venture-funding fluctuations – both up and down – map to its general health. A historical sequence of XR industry ups and downs has tracked closely with its funding inflows.

These events over the past decade include the XR industry’s circa-2017 hype cycle, subsequent correction, quick rebound, metaverse boom/bust, Covid software boom/bust, and the more recent rise of AI. XR funding throughout this period maps closely to the macro-environment.

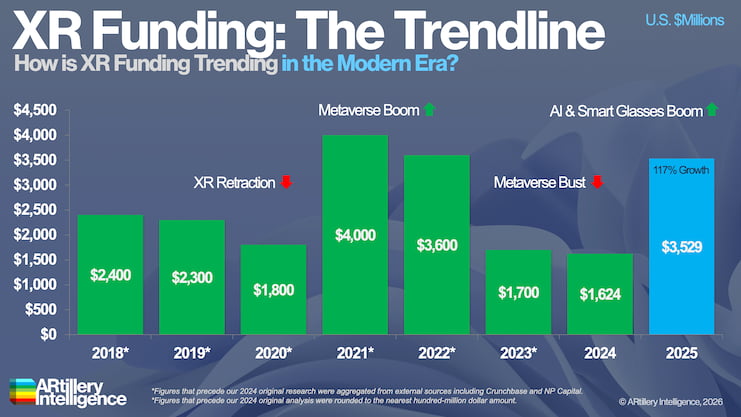

So where are we now? After a few years of declines – mostly due to the hangover from circa-2021 “metaverse mania,” XR venture funding reached $3.53 billion in 2025 – a 117 percent year-over-year jump. Meanwhile, 2026 year-to-date funding has mostly sustained this momentum.

What’s driving this growth? This is the topic of a recent report from our research arm, ARtillery Intelligence. It joins our excerpt series, continuing in this installment with a look at XR funding’s recent history, correlation to broader macro factors, and what defines the current environment.

Disciplined & Discerning

Starting with XR’s recent history, investor activity has been more disciplined and discerning following the metaverse boom/bust cycle. A return-to-fundamentals dynamic has also defined the broader funding environment – due largely to the hangover from the Covid software boom.

But if we go back further for historical context, we can look at XR’s current era – starting with Meta’s 2014 acquisition of Oculus. Since then, we’ve seen a few boom & bust cycles. And fluctuations in venture funding mapped closely to these ups and downs (see graphic below).

The first XR boom in this timeframe was the circa-2017 period of elevated excitement, which led to overvaluation and oversupply that wasn’t met with equivalent demand. This caused a shakeout and market correction from 2018 to 2020 – a relatively short bust period.

The reason for XR’s shortened time in the penalty box was that investor appetites were revived by the excitement and investment that picked back up in late 2020. This was driven by a combination of the Covid software boom and the phenomenon we call “metaverse mania.”

But as the metaverse failed to prove its tangibility, a correction followed. This was amplified by two things. The first was the hangover from the Covid software boom, as noted. The second was the rapid rise of AI, which siphoned investment dollars away from other sectors, including XR.

The Intersection of AI and XR

That brings us closer to the present, where XR funding surprisingly rebounded by growing 117 percent last year to $3.53 billion. That’s not only a healthy growth rate, but was the first year of growth after three consecutive years of declines. Why the resurgence? One answer is AI.

Though AI started as an XR-funding headwind for the reasons noted above, it has since shifted into more of a tailwind. This is because AI can often amplify XR’s capabilities, such as automating developer workflows and driving the industry’s most momentous segment: smart glasses.

One strategic takeaway is that XR startups that can demonstrate that their products live at this intersection of XR and AI can attract investors. But the key term is “demonstrate.” XR/AI integrations must be real and robust if they’re to pass the diligence test from any decent investor.

Put another way, repeating the term ‘AI’ in pitch decks – an all-too-common practice these days – won’t work. This is behavior we saw in the aforementioned metaverse boom years. In either era, investors see right through the buzzword bingo if there isn’t substantive technical backing.

We’ll pause there and pick things up in the next installment with more analysis around the XR funding environment, as well as segmentations like category, stage, and deal size. Meanwhile, check out the full report for more color.