This post is adapted from ARtillery Intelligence’s report, Mobile AR Strategies & Business Models. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

In AR’s early stages, a common question continues to be asked: where’s the money? There have been oscillations in excitement and doubt over AR, but the ultimate proof point will be revenue. Though aggregate revenues have disappointed, there are segments bearing fruit.

So we’ve examined the three biggest revenue categories for consumer-based mobile AR. We’ll examine them on qualitative and quantitative levels. The former entails product models, leading companies and best practices. The latter entails market sizing and revenue projections.

But before we dive into these models, what are they at a high level? We categorize them as follows:

1. Advertising (brands pay)

2. In-app purchases (consumers pay)

3. AR-as-a-service (enterprises pay)

Of course, there are more AR business models such as hardware sales (AR glasses). But since smartphone-based AR provides greater scale today, we’re focusing this analysis on software-based models in consumer mobile AR. We’ll separately tackle other subsectors like industrial.

Panning back, you may notice each of the above models has a different revenue source. In AR advertising, brands pay to create and distribute ads. With in-app purchases, consumers pay for enhanced experiences. And with AR-as-a-service, enterprises pay for tools to develop AR.

Starting with advertising, brands are increasingly learning that AR has inherent capabilities to demonstrate products in immersive ways. And it can span the consumer purchase funnel including reach-driven product/brand exposure as well as direct-response product conversions.

Ad campaign examples continue to build, and there’s momentum in the brand advertising world to adopt AR. Seeing revenue and doubling down on it, Facebook and Snap are increasingly catering to these brands with tools to lower barriers for AR lens creation and capability.

Moving on to the second business model, in-app purchases (IAP) are fitting for lots of AR experiences, especially gaming. This stems from the model’s success in mobile gaming, and its ability to maximize ARPU through the behavioral economics of micro-transactions.

But moreover, it’s fitting because AR is too early and unproven for consumers to pay upfront for premium apps. Our survey data with Thrive Analytics supports this. And if you need any more evidence, just look at the nearly $3 billion in IAP that Niantic has generated to date.

Lastly, there’s AR-as-a-service (ARaaS). This involves enabling tech that lowers friction or boosts capabilities. This democratizes advanced AR capabilities like graphics creation and includes tools like Unity, Amazon Sumerian and 8th Wall. Our recent analysis of Adobe Aero is another example.

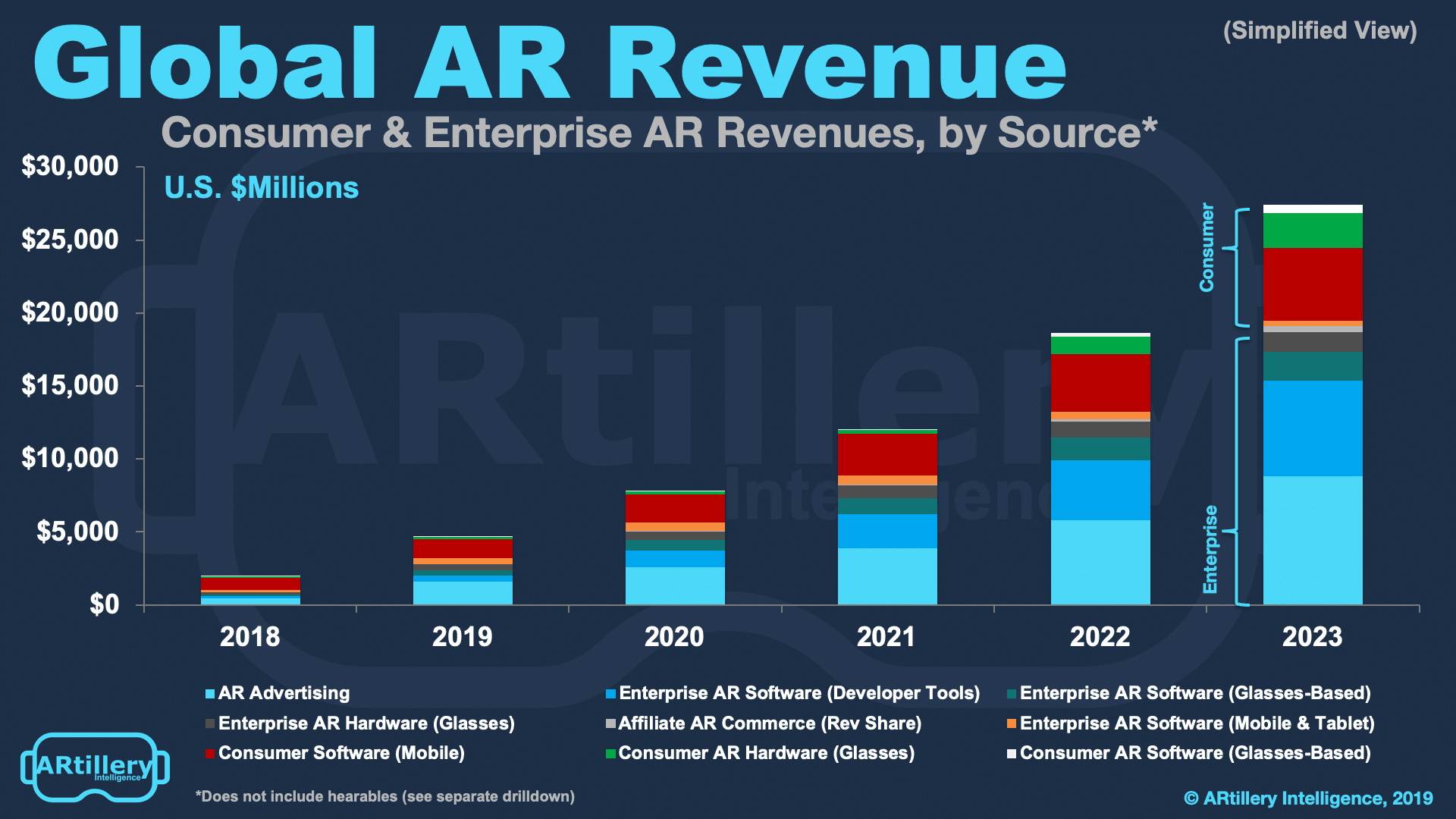

Adding up all three categories, it’s a $1.44 billion market, growing to $20.3 billion by 2023. The common thread with these models is AR technologies where the end-users are consumers on mobile devices as opposed to industrial enterprises and/or headworn AR experiences.

As an additional caveat, some of the above revenue categories are technically “enterprise AR” as enterprises are the source of spending. That applies here but the AR experiences listed above ultimately end up in consumers’ hands, as opposed to those built for industrial productivity.

That makes a few of the spending categories outlined above fall into a new category we call B2B2C. This is the case for AR advertising, as well as AR-as-a-service. In both cases, enterprises are the AR buyer but consumers are the target or end-user. This will be a major AR category.

We’ll be back in the coming weeks to dive deeper into each of these revenue categories and how things are playing out today. Meanwhile, you can see the full report from our research arm ARtillery Intelligence, or preview it here. The report’s video companion can also be seen below.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.