“Behind the Numbers” is AR Insider’s series that examines strategic takeaways from ARtillry Intelligence data. Each post drills down on one topic or chart. Subscribe for access to the full library and other knowledge-building resources.

One of the biggest precursors for AR’s opportunity is hardware installed base. Today much of that comes from smartphones, as mobile AR is the near-term play. That will be the case for several more years as AR glasses inch towards tenable pricing and specs for mainstream adoption.

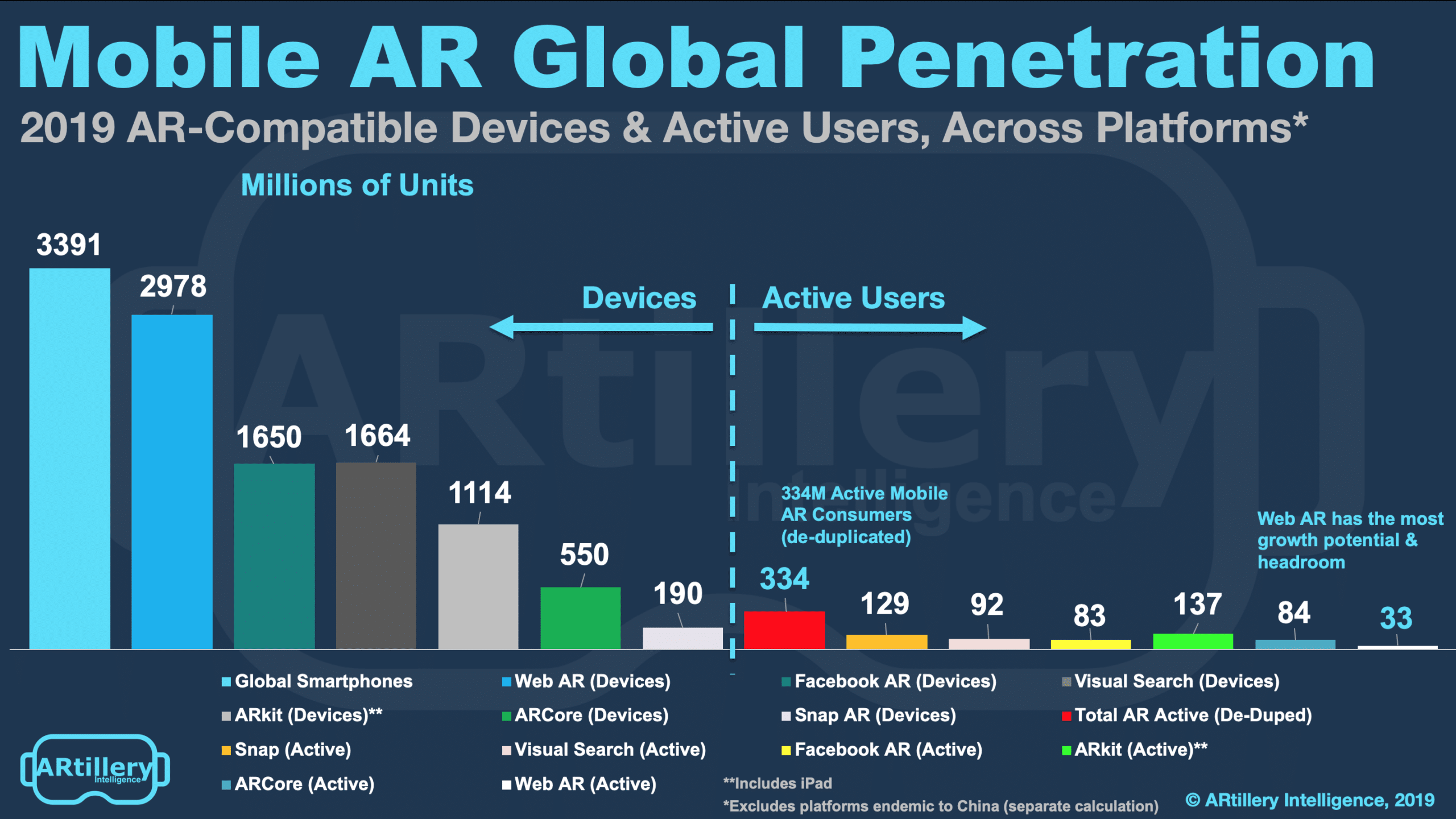

That mobile AR installed base is often cited as “1 billion units.” This is true if counting Apple (ARkit) and Google (ARcore) compatibility. However, an increasingly-fragmented set of mobile AR platforms creates a more complex picture, and a larger installed base than often cited.

According to the latest AR revenue forecast from our research arm ARtillery Intelligence, there are 3.39 billion smartphones on the planet. Those that are AR-compatibile include web AR (2.97 billion), Facebook’s Spark AR (1.6 billion) Snap’s Lens Studio (190 million) and others.

Active & Addressable

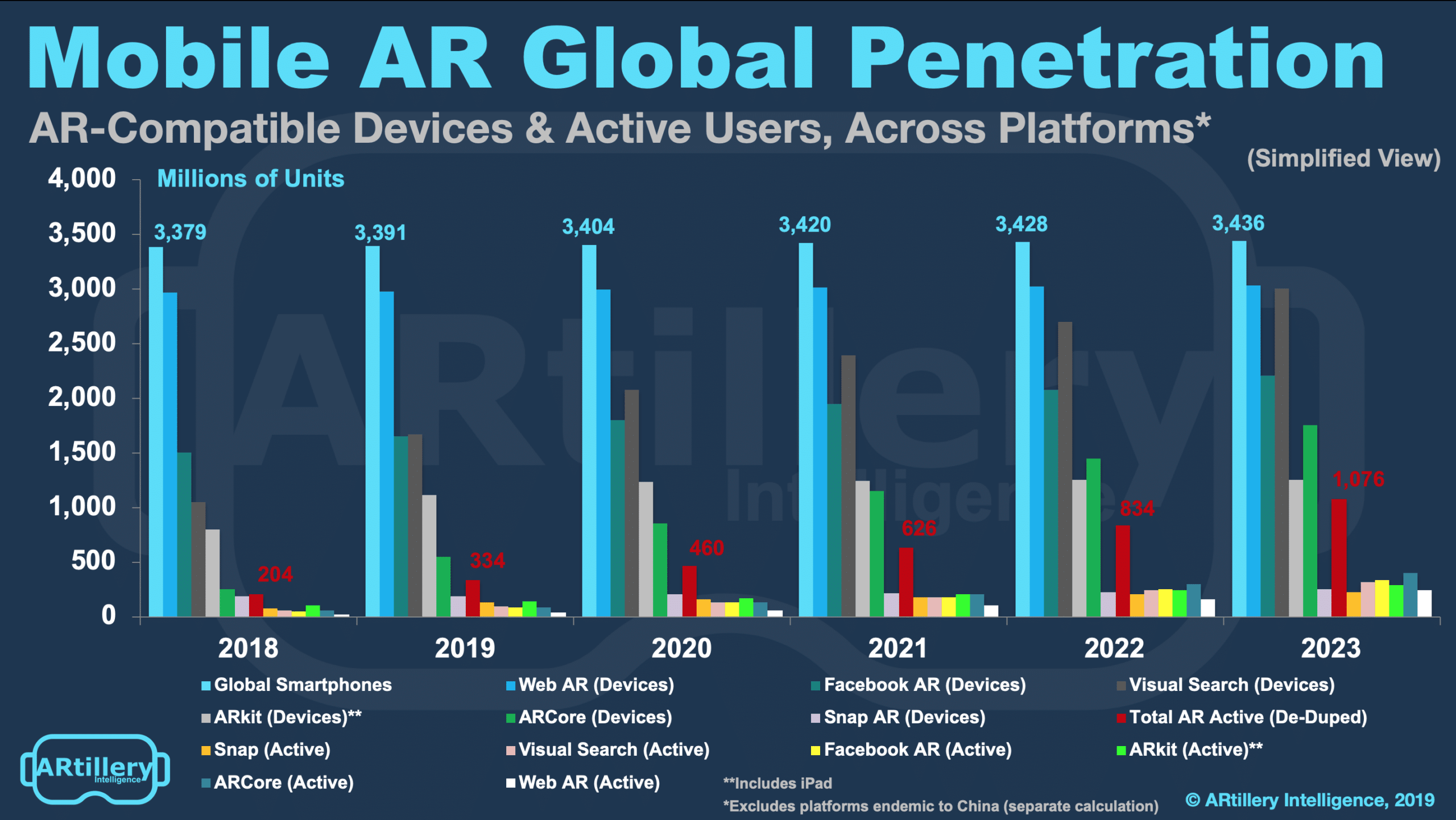

But the above figures measure total devices and AR compatibility. The number that matters more is active AR users. That total comes to 334 million, growing to 1.076 billion by 2023. This figure essentially tallies and de-duplicates active users across all of these platforms.

As an important qualifier, this doesn’t include platforms endemic to China. Such platforms are significant, but their sizing is done separately in terms of addressable market analysis. That’s because users of these platforms aren’t always addressable to companies outside of China.

As for insights that these data uncover, it’s notable how Web AR has both the highest compatibility and lowest active usage. That indicates growth potential, not just in ample headroom but also considering Web AR’s momentum and benefits. It’s easier to access than app downloads.

Web AR capability will also improve and catch up to native AR apps, while holding advantages like less AR “activation energy.” To devise Web AR compatibility required deep research into smartphone compatibility among companies building AR tools and experiences for the web.

Horse Race

As for other growth areas, ARCore has strong potential. Android’s global base gives ARCore a larger shell to grow into, though it currently trails ARkit. ARkit’s early lead has a lot to do with Apple’s vertical integration and ability to push firmware updates to a narrower range of hardware.

Visual search is likewise opportune. This is due to its utility-oriented, high-frequency use case we often cite. But more to the point of this analysis on distribution channels, Google’s ability to push Google Lens and infuse AR into search results will accelerate mainstream access and adoption.

Stay tuned for more forecast tidbits and insights over the coming weeks. Meanwhile, find out more about the report methodology or access the entire thing here. There will be lots to unpack as the AR market unfolds and becomes a virtual horse race of several competing platforms.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.

Header Image Credit: Apple