This post is adapted from ARtillery Intelligence’s report, Mobile AR Strategies & Business Models. It includes some of its data and takeaways. More can be previewed here and subscribe for the full report.

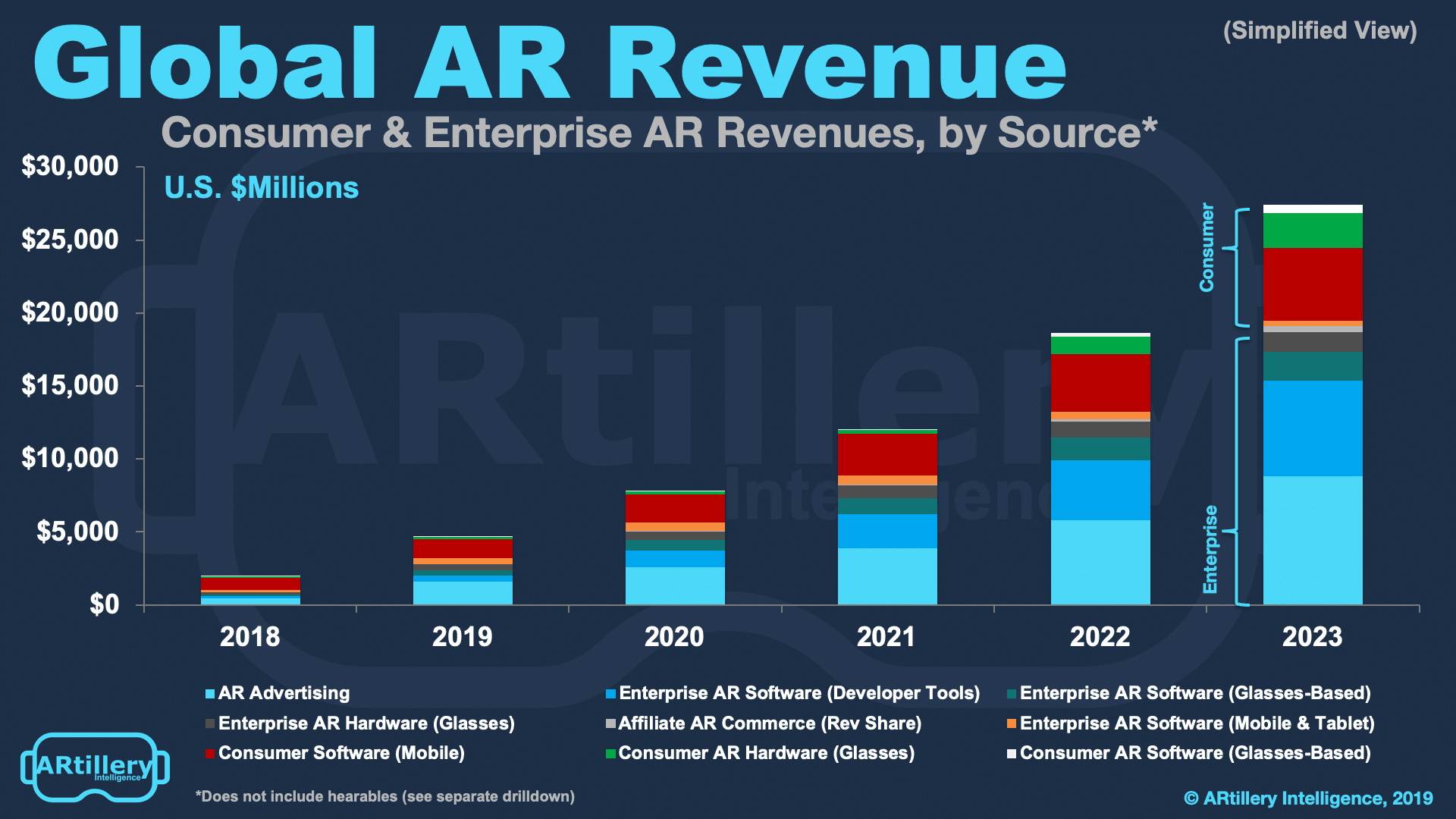

In AR’s early stages, a common question continues to be asked: where’s the money? There have been oscillations in excitement and doubt over AR, but the ultimate proof point will be revenue. Though aggregate revenues have disappointed, there are segments that are bearing fruit.

So we’ve determined the three biggest revenue categories for consumer-based mobile AR. We’ve examined them on qualitative and quantitative levels. The former entails product models, leading companies and best practices. The latter entails market sizing and revenue projections.

But before we dive into these models, starting today with advertising, what are they at a high level? We categorize them as follows:

1. Advertising (brands pay)

2. In-app purchases (consumers pay)

3. AR-as-a-service (enterprises pay)

Drilling Down on Ad Revenue

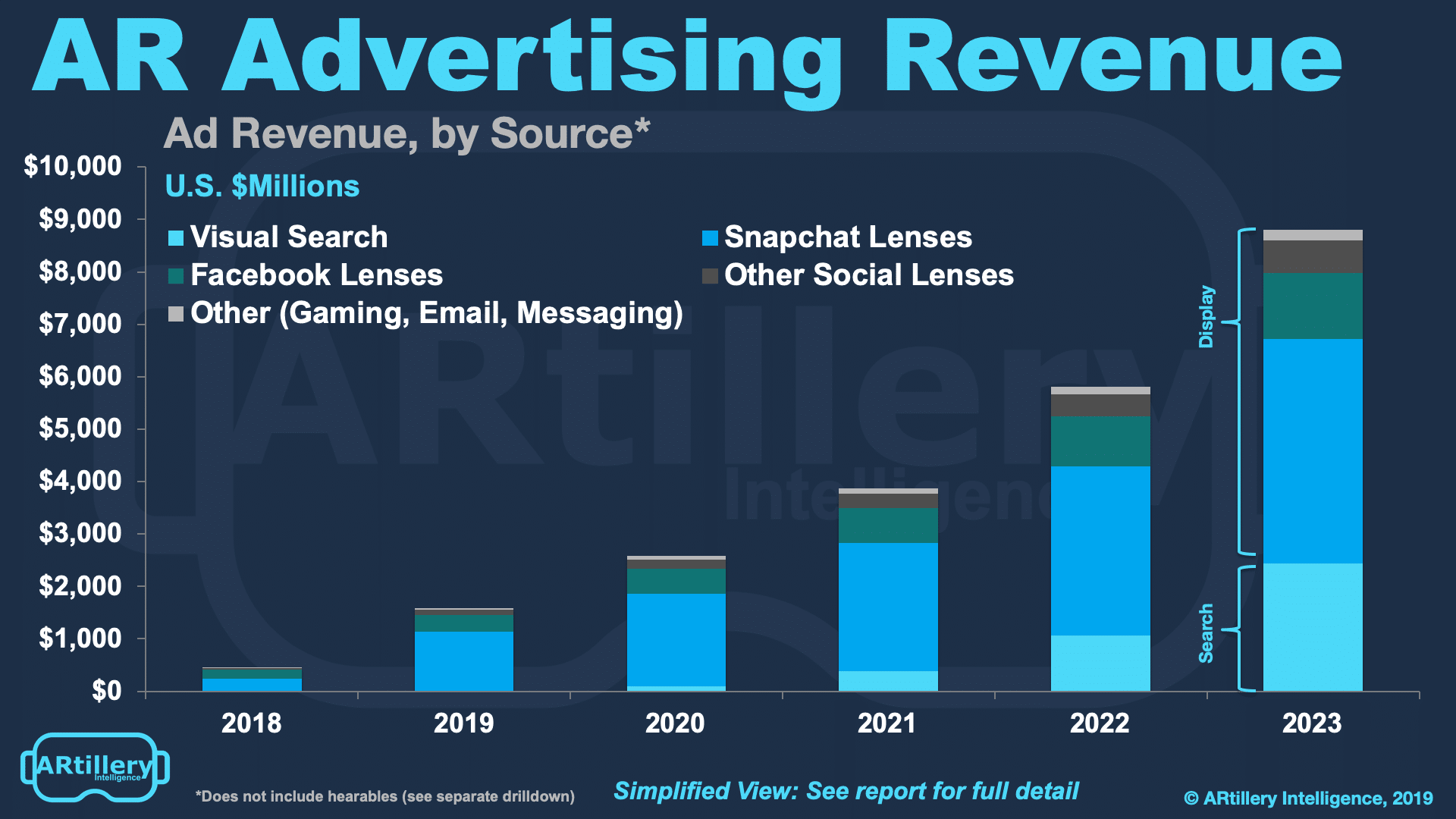

Starting with advertising, it’s currently the largest source of spending in AR. Specifically, it derived $453 million in 2018 according to ARtillery’s annual Global AR Forecast. That’s projected to grow to $8.8 billion by 2023. This revenue position is so far owed to the viral appeal of social AR lenses.

Led by Snapchat, usage has exploded around social AR Lenses. In fact, of all the mobile consumer AR formats and use cases today, social lenses dominate. Snapchat alone has reported that 142 million users engage with AR lenses daily. This is greater than Pokémon Go active users.

High levels of engagement are a starting point for media formats that attract advertisers. Bringing that to the next level, AR lenses demonstrate products in highly immersive ways. This has appealed to advertisers that appreciate the creative capacity that 3D content now affords them.

Moreover, that level of engagement is proving out through ad performance metrics. YouTube for example recently reported that 30 percent of viewers of its campaign with L’Oréal chose to activate the AR lens option to virtually try on shades of lipstick. This led users down the purchase funnel.

This makes AR lenses a rare “full-funnel” advertising format. In other words, they can accompany ads in high-reach “upper-funnel” distribution channels like YouTube ads or the Facebook News Feed. But once activated, they engender “lower-funnel” behavior like try-ons and conversions.

AR Lenses: Naming Names

As for market share, we estimate that Snap derived $246 million of the $453 million stated above. This makes it AR’s revenue leader. Pokémon Go’s $3 billion in in-app-purchases is greater, but that sum isn’t directly-attributable to AR, depending on your definition of AR.

Furthermore, Snapchat continues to double down on AR lenses. It recently extended lenses from selfie fodder to rear-facing camera AR that augments the world. That includes more utilitarian and intelligent AR based on scene awareness, able to do things like solve math problems on the fly.

Adding up its current position, Snapchat has seen 15 million cumulative lens views from 500,000 lenses. Its lens developer community continues to grow – fueled by the above tools – to the tune of 20 percent during Q3 2019. And as mentioned, it now reaches 142 million daily AR lens users.

But Facebook looms with one billion lens views in the past year. It got a later start with AR lenses, but could gain market share as it blitzes AR ad spend from existing advertisers. Its installed base is larger than Snapchat’s — 1.5 billion devices — and it likes to copy its closest competitors.

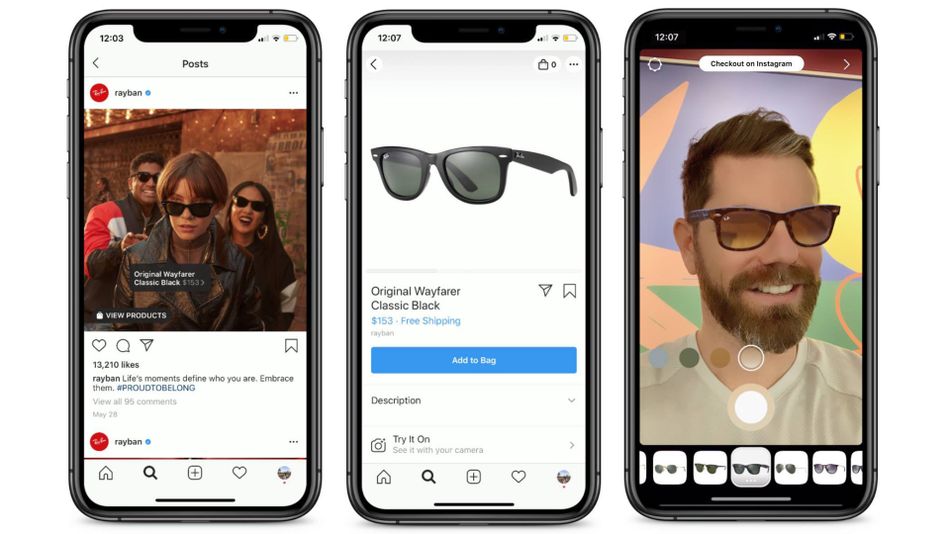

Facebook is also motivated to AR to diversify revenue, as diminishing News Feed ad inventory forces it to find other pastures. That includes Messenger (covered later in this report) and Instagram. The latter is the sleeping giant, with an aligned use case and recent AR integration.

The opportunity also extends beyond these social walled gardens. Broader cross-platform reach could come from Web AR, where capabilities are limited but catching up. That’s being led by innovators like 8th Wall, already working with advertisers like Miller Coors and Sony Pictures.

We’ll be back in the coming weeks to dive into other revenue models beyond advertising, and how things are playing out today. Meanwhile, you can see the full report from our research arm ARtillery Intelligence, or preview it here. The report’s video companion can also be seen below.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.