ARtillery Briefs is a video series that outlines the top trends we’re tracking, including takeaways from recent reports and market forecasts. See the most recent episode below, including narrative takeaways and embedded video.

VR continues to show early-stage characteristics, including erratic interest and investment. But how big is it, and how big will it get? ARtillery Intelligence has quantified the revenue outlook, resulting in the fourth wave of its Global VR Forecast, and ARtillery Briefs episode (below).

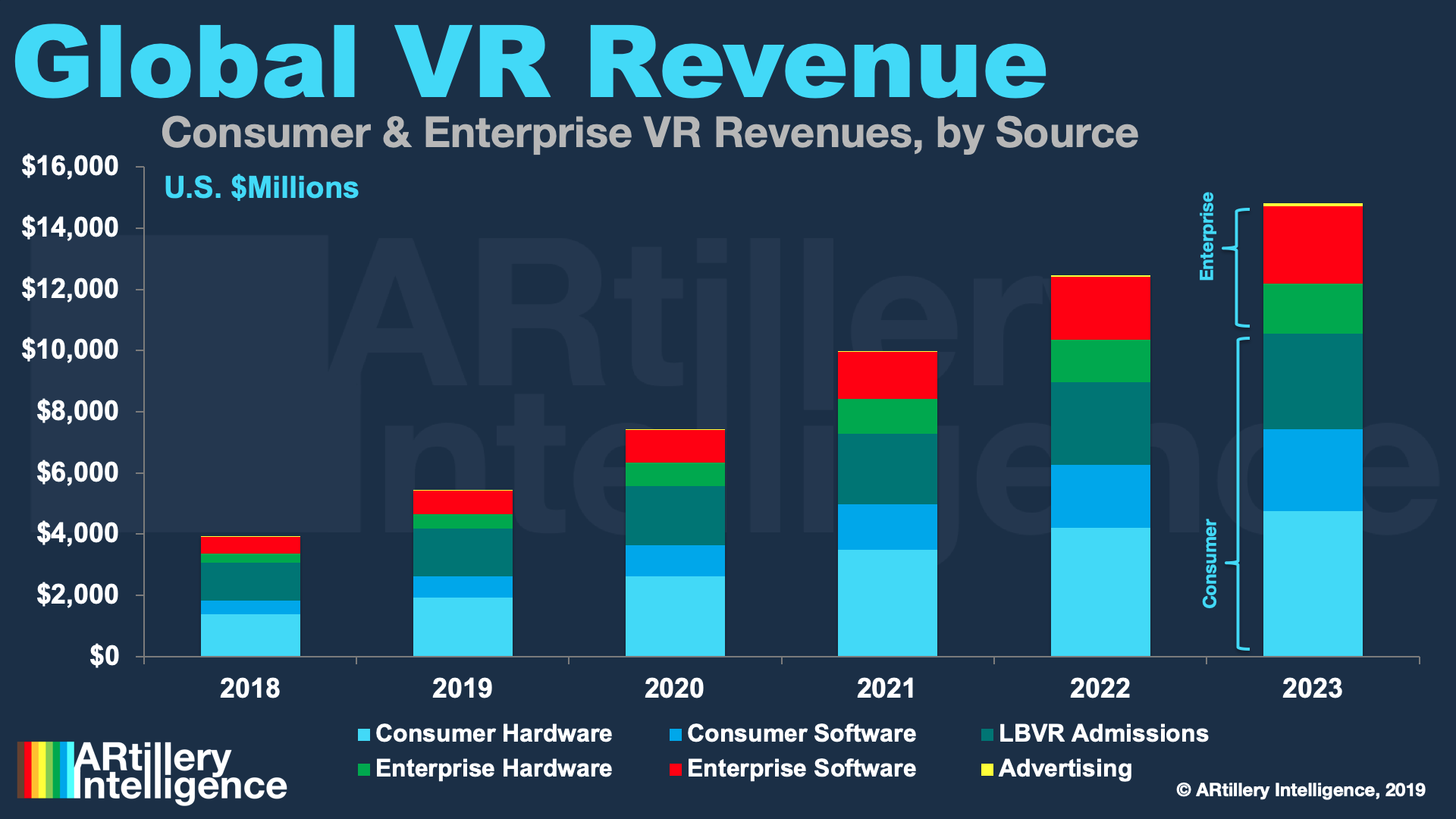

So what are the takeaways? At a high level, VR revenue is projected to grow from $3.9 billion last year to $14.8 billion in 2023. That includes lots of moving parts and sub-sectors like consumer and enterprise. Those are further subdivided by hardware, software and other revenue sources.

Virtuous Cycle

Consumer VR is projected to grow to $10.6 billion by 2023. That includes things that consumers pay for, currently dominated by hardware. It’s often the first step in emerging tech markets as an installed base is formed which then paves the way for software — in this case games and apps.

As that hardware base grows, it becomes a larger addressable market which attracts and incentivizes content creators. That influx can boost content libraries over time, which in turn fuels further user demand. Over time, revenue-per-user metrics can then improve, and around we go.

We’re certainly not there yet with this virtuous cycle in VR. But those wheels are slowly turning and are accelerated by things like Oculus Quest. This comes as Facebook prioritizes market share over margins with a competitively-priced and high-quality device that’s turning heads.

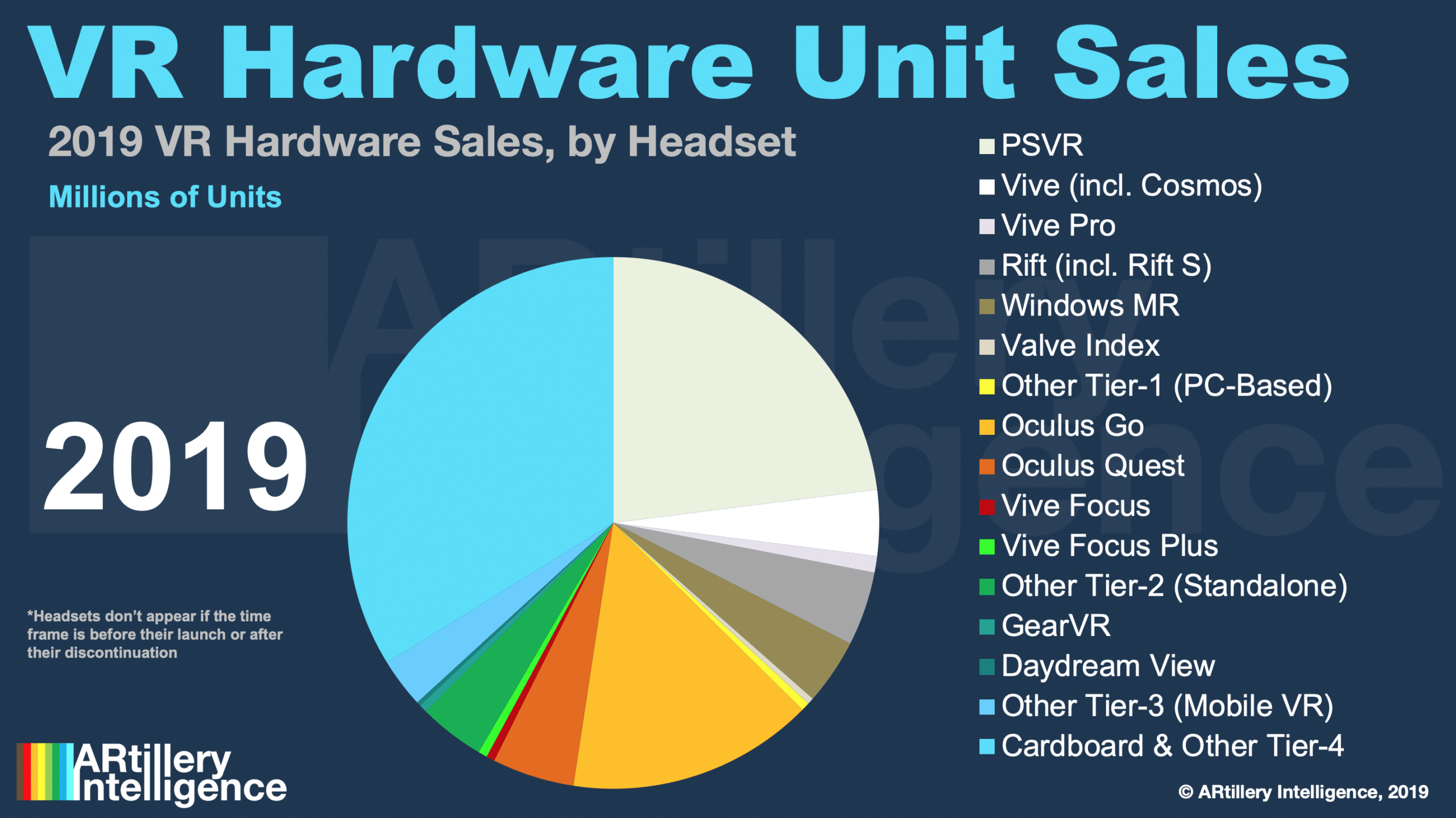

Quest’s unit sales are already looking strong according to several signals. Based on disclosures about Quest’s content sales, we’ve extrapolated its corresponding hardware sales. That stood at about 300,000 units in September, on pace to reach about 470,000 units by the end of the year.

VR at Work

Shifting to enterprise VR, ARtillery Intelligence sees that growing from $829 million in 2018 to $4.26 billion in 2023. These figures consist of anything that companies pay for. So like consumer markets, that includes hardware but also VR apps for productivity, training and visualization.

It also includes the creation tools for consumer-facing enterprises to develop VR experiences (e.g Unity). This will be a growing category among retailers, gaming and entertainment. Though end-users here are consumers, it’s an enterprise purchase which designates it as B2B2C.

For all of the above, enterprise VR spending still trails its consumer counterpart but will gain ground in revenue share throughout this five-year outlook. Factors driving that include ROI gains in corporate and industrial VR implementations, such as training and design prototyping.

Barriers to adoption are also notably lower in some cases than AR where more technically-complex hardware is purpose-built for enterprise (think: Hololens). Some enterprise VR buyers, such as training use cases, can conversely utilize off-the-shelf consumer hardware.

Hardware: Tip of the Spear

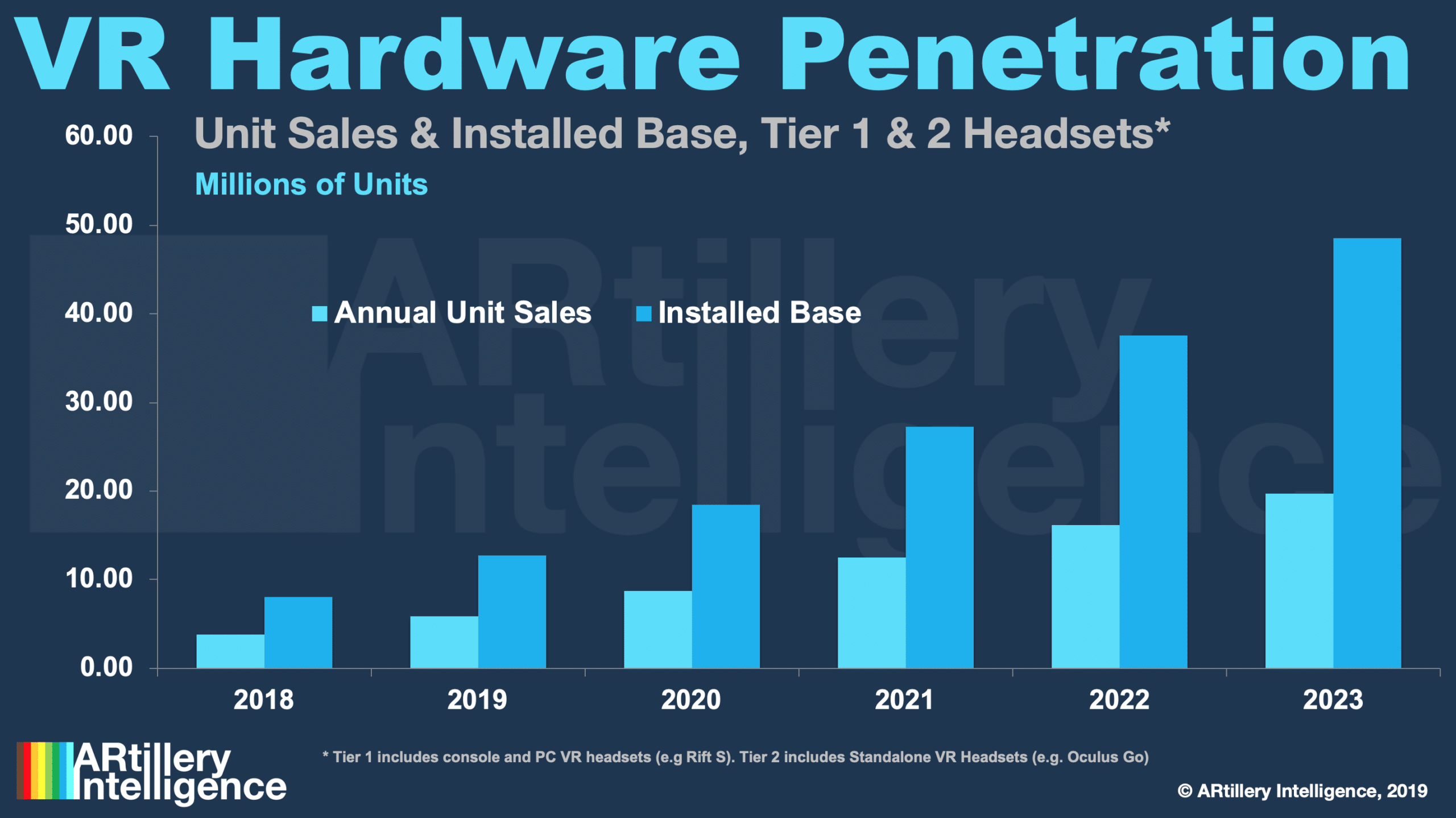

Speaking of hardware, it again comes first in emerging markets. There were an estimated 5.8 million units sold in 2019 for tier-1 and 2 headsets, growing to over 19 million in 2023. That correlates to a cumulative installed base of 12.7 million units this year and 48.5 million by 2023.

Playstation VR is the market share leader today and will continue to be strong, but the biggest movers will be Oculus Quest and Go, which address separate use cases but both hit the sweet spot of aggressive pricing, best-in-class quality levels, and quickly-growing content libraries.

That just scratches the surface, and there’s of course a lot more to the market sizing. At a high level, the above figures are best characterized as cautiously optimistic. Growth and scale will come but likely slower than many industry proponents, including us in the past, have believed.

That represents an ongoing process of attention to market signals and constant course correction. Expect more of that to come from our research arm ARtillery Intelligence, and some of the breakdowns we’ll provide here. Meanwhile, see more color in the video below or full report.

For deeper XR data and intelligence, join ARtillery PRO and subscribe to the free AR Insider Weekly newsletter.

Disclosure: AR Insider has no financial stake in the companies mentioned in this post, nor received payment for its production. Disclosure and ethics policy can be seen here.