As we roll into 2021, AR and VR — collectively known as spatial computing — are each at different stages. Breaking them down further, they consist of several sub-segments that are likewise at different stages of their lifecycles and led by different market dynamics.

For these reasons, AR Insider’s research arm ARtillery Intelligence has begun to separate its major market-sizing endeavors into three main pillars: mobile AR, headworn AR, and VR. They’re each specific and nuanced enough to deserve their own focused drill-downs.

This follows the previous practice of releasing one monolithic “VR/AR” forecast. Though it contained subdivisions, lumping them together isn’t useful to anyone. Companies in spatial computing live in specific segments and want guidance on their addressable market.

So how do these individual markets stack up? ARtillery sought to answer these questions in a recent investing-focused event for VRARA, including breakdowns of the above three pillars. We’re featuring it in this week’s XR Talks (video and takeaways below).

The Here-and-Now Opportunity

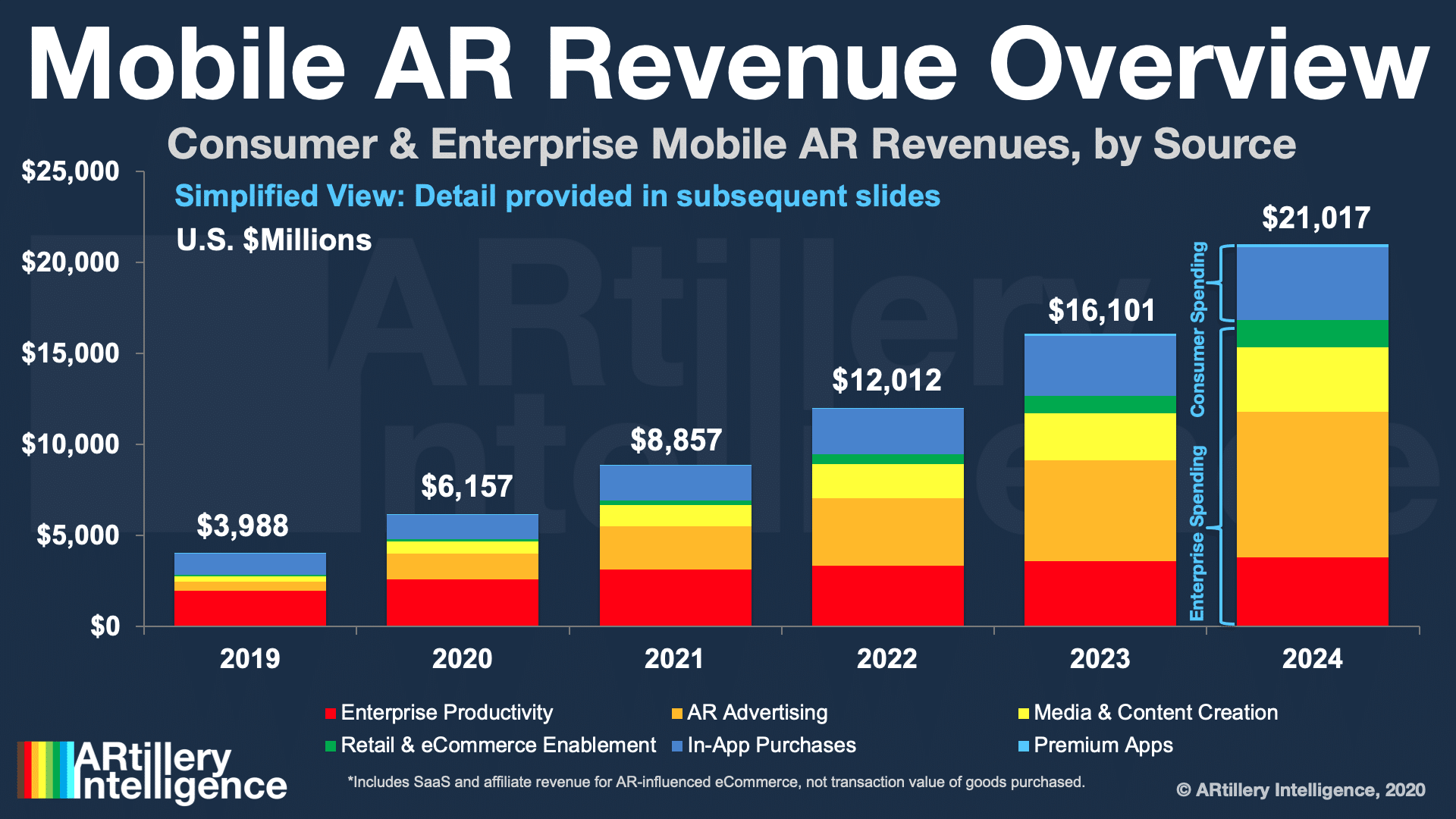

Starting with mobile AR, ARtillery projects it to grow from $3.98 billion last year to $21 billion by 2024. This consists of several subdivisions including enterprise productivity, consumer spending, and AR advertising. The latter alone is estimated to reach $1.4 billion in 2020.

Stepping back, one of the foundations for the mobile AR opportunity is smartphone scale, as it piggybacks on a ubiquitous device that we all carry. To quantify that, there are about 3 billion AR-compatible smartphones globally, thanks to the work of 8th Wall and others to enable web AR.

Beyond Web AR, we continue to see momentum from other AR platforms including everything from ARkit to Snap’s Lens Studio. When we look at all these platforms and de-duplicate usage overlaps, there’s an estimated 598 million active AR users globally today.

Building on that installed base are several revenue opportunities, such as the areas mentioned above. A less-sexy but promising revenue category is AR tool builders and enablers. These are platforms that accelerate AR by lowering friction and democratizing its creation.

We call this category “AR as a Service,” and it includes companies of all sizes — from Adobe to Unity to 8th Wall. It will grow into a broad ecosystem including everything from consumer-facing experience creation (B2B2C) to streamlining and scaling 3D asset creation.

Line-of-Sight

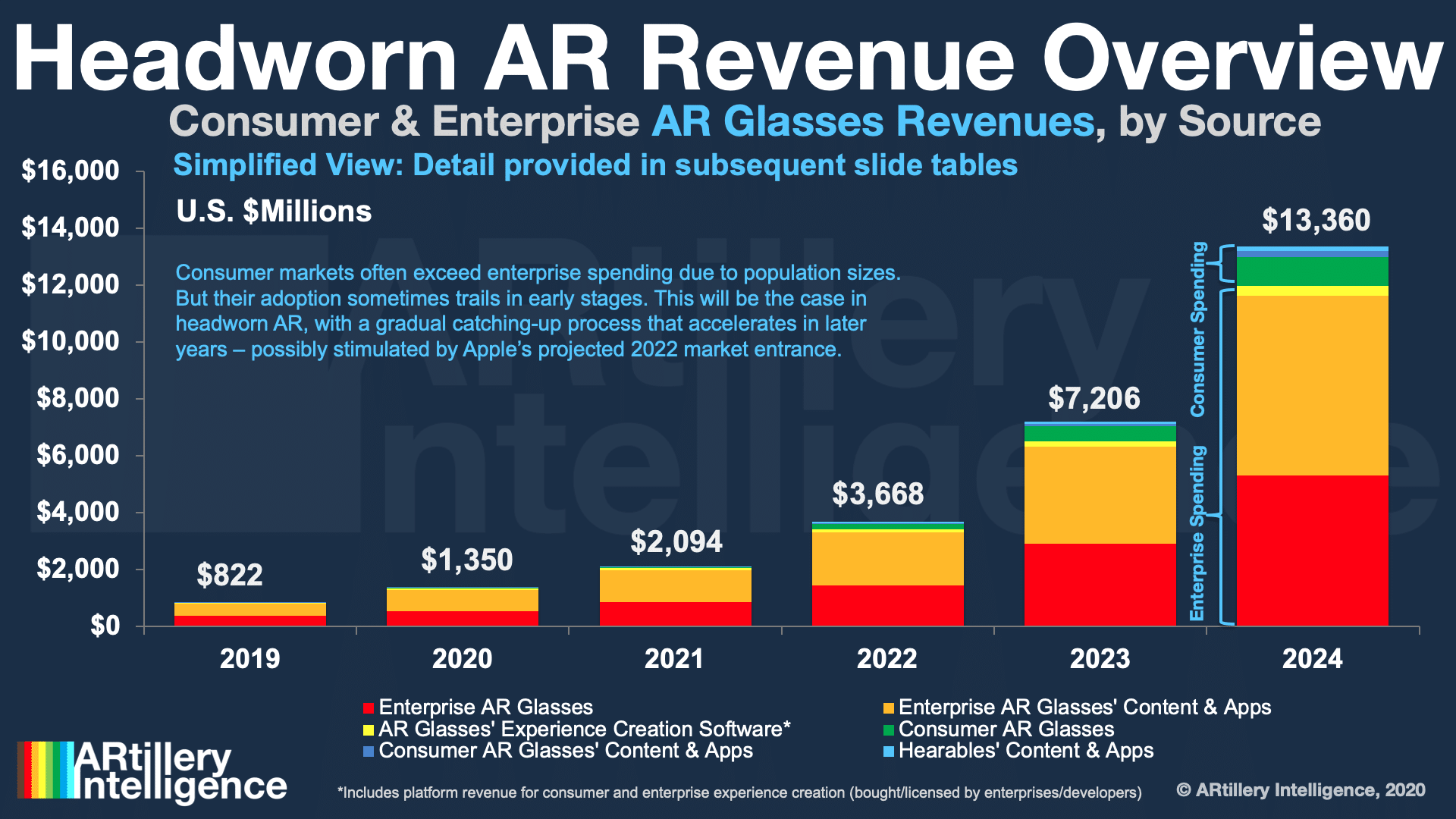

Moving on to headworn AR, it’s projected to grow from $822 million in 2019 to $13.4 billion by 2024. That’s steep growth as it sprouts from such a small base (as the properties of early-stage market growth often go). The headworn AR market today is small but substantially promising.

Those spending levels are dominated by enterprises. Specifically, the leading revenue segment today is enterprise hardware. This will be eclipsed over time by enterprise software, as it builds on a larger installed base and scales via typical SaaS economics and recurring cycles.

As for consumer-based AR glasses, they’re projected to grow from an almost non-existent base today to 1.59 million units in 2024. The wild card here is Apple’s rumored market entrance in 2022. If that happens, it could raise all boats to some degree, as Apple incites mainstream demand.

But don’t get too excited….we’re talking about a few million units in the first few years (similar to iPhone and Apple Watch growth curves). To compare that to a ubiquitous device to put things into perspective, 2024’s projected AR glasses sales will be dwarfed by smartphones 2000 to 1.

Also be ready for redefined AR from Apple. It won’t be a graphically intensive UX but rather a stylistically-viable form factor that prioritizes wearability. That will mean “liter” forms of AR such as enhancing human vision, wearables fusion, iOS notifications, and commerce-oriented alerts.

Fully Immersed

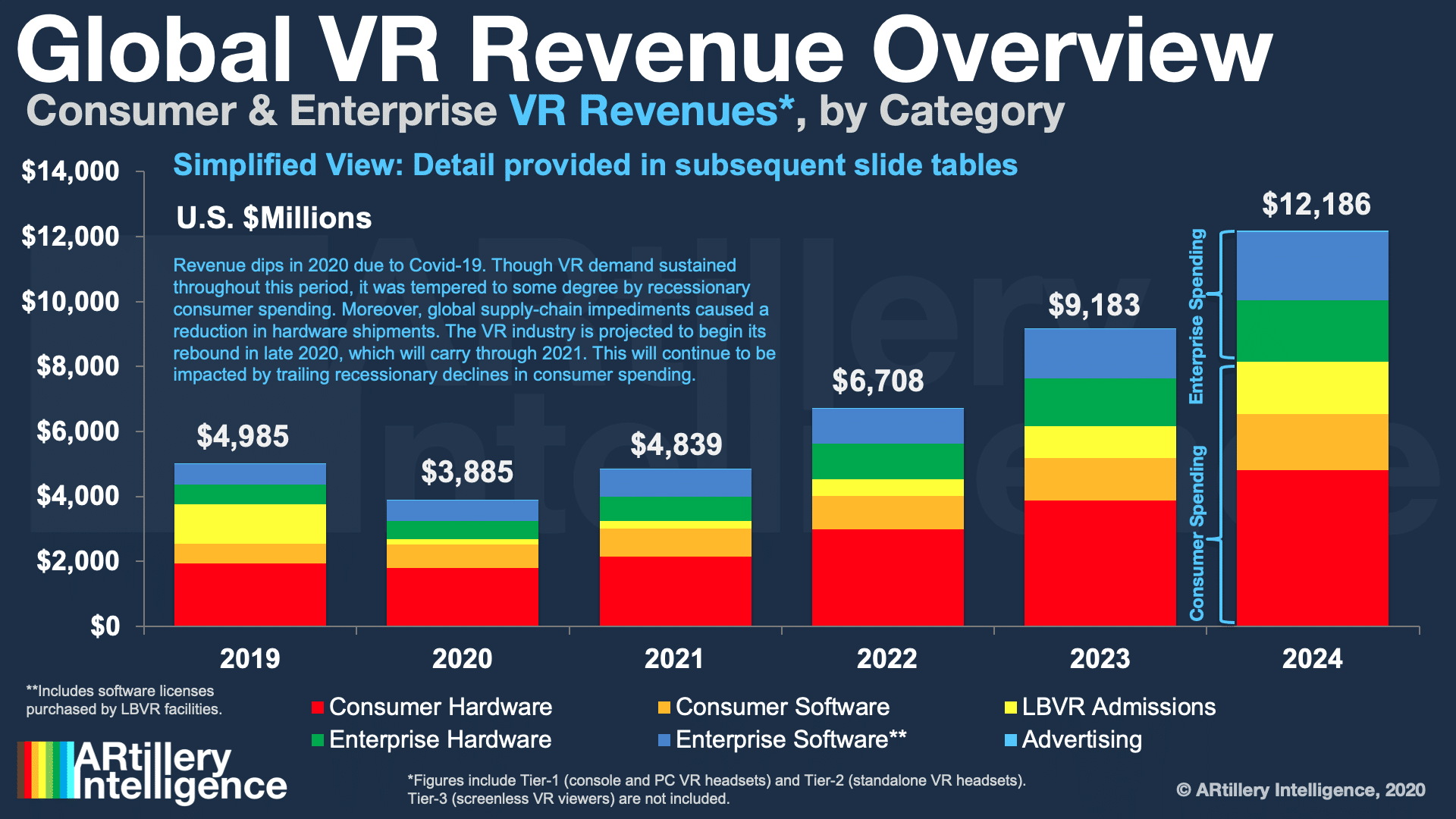

Moving on to the third and final spatial pillar, what’s happening in VR? Like the AR categories above, there are several sector-specific drivers and dynamics. Starting at a high level, VR will grow from $4.9 million in revenue last year to $12.2 million in 2024, with a pandemic dip in 2020.

Just like the above AR categories, VR’s foundation starts with its hardware base. There we project PC, console and standalone VR sales to grow from 5.41 million units last year to 14.31 million by 2024. The latter correlates to a cumulative installed base of 34 million in-market units.

To address the pandemic decline in 2020, it’s primarily driven by supply-chain impediments, which had an outsized impact on VR’s hardware-heavy revenue makeup. Those headwinds had less impact on AR, especially mobile AR which is deployed primarily through software.

Another way to look at VR in 2020 is that demand wasn’t lacking, as it aligns with Covid-advantaged sectors like gaming. So declines were all about supply. The net effect was a 10 percent year-over-year dip in units shipped….which could have been worse if not for a few factors.

To the Rescue

Those factors include Facebook’s beefed-up supply chain for Quest 2, which lessened the degree of 2020’s VR unit shipment decline. It has mostly met Quest 2’s substantial demand levels throughout Q4 and isn’t experiencing the same holiday shortages it had last year at this time.

Meanwhile, it’s not just about Quest 2. PSVR continues to be the market share leader, piggybacking on 100 million+ Playstation 4 units (and Playstation 5 potential). Other spec-advantaged hardware will ride a post-Covid rebound, including Valve Index and HP Reverb g2.

That rebound will be fueled by pent-up demand as well as VR’s alignment with Covid-accelerated sectors like gaming, remote work, and virtual events. But beyond the current period, these factors could have long-term effects that sustain in a post-Covid hybrid-world of remote work and events.

See the full presentation embedded below, and stay tuned for coverage of other segments at the same event, including the investor panel shown above.